11min Read

11min Read

Mutual Fund Advisory Services: Do You Really Need a Mutual Fund Advisor in 2026?

Mutual Fund Advisory Services: Do You Really Need a Mutual Fund Advisor in 2026?

Mutual Fund Advisory Services: Do You Really Need a Mutual Fund Advisor in 2026?

Understand mutual fund advisory services, compare RIAs, distributors and digital platforms, and choose an adviser based on your financial goals.

Understand mutual fund advisory services, compare RIAs, distributors and digital platforms, and choose an adviser based on your financial goals.

Understand mutual fund advisory services, compare RIAs, distributors and digital platforms, and choose an adviser based on your financial goals.

Ckredence Wealth

Ckredence Wealth

|

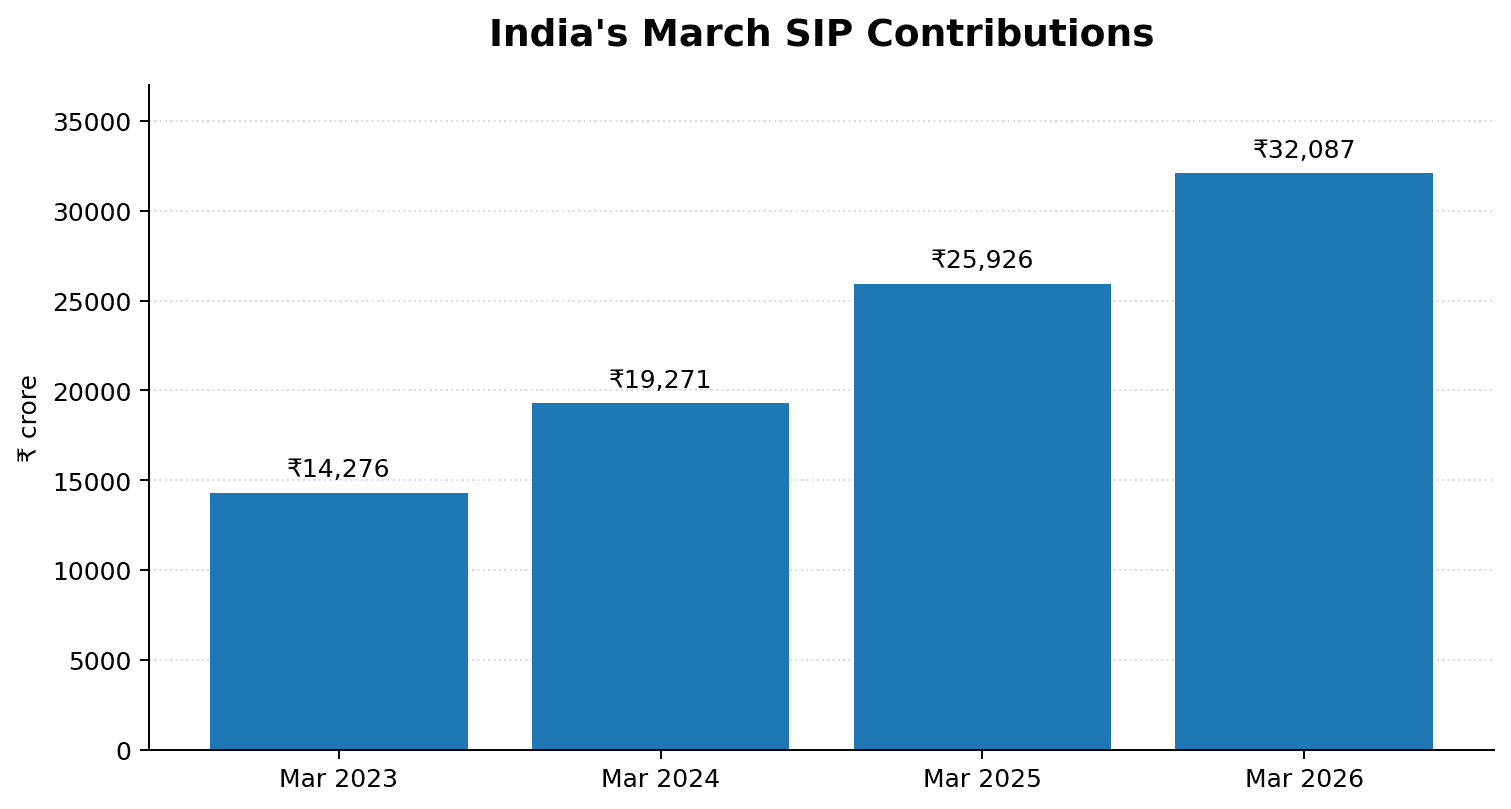

India’s mutual fund participation is rising, but investment decisions still need context. AMFI’s March SIP series moved from ₹14,276 crore in March 2023 to ₹19,271 crore in March 2024, ₹25,926 crore in March 2025, and ₹32,087 crore in March 2026. More people are investing through SIPs, yet many still choose funds before checking their financial goals, risk capacity, or existing allocation.

Does your current mutual fund portfolio match your retirement, business, family, and liquidity needs?

Do you know whether a recommendation comes from paid advice or product distribution?

Are you reviewing fund overlap, risk changes, and your changing financial priorities?

Mutual fund advisory services can bring structure to these questions. They help investors move from isolated fund purchases to a plan that connects money with purpose, time horizon, risk, and review discipline.

Figure: India’s March SIP Contributions | Source: AMFI monthly publications and annual reports

TL;DR

Mutual fund advisory services should begin with your goals, risk profile, and investment horizon.

Fund selection should follow asset allocation, not recent returns or online recommendations.

RIAs, distributors, and digital platforms work under different fee and service models.

Direct and regular plans should be discussed before you invest.

A portfolio review should check overlap, fund role, allocation drift, and changing financial needs.

Written recommendations and consent records reduce confusion around portfolio changes.

Advisory may suit investors who need planning support, but it is not necessary for every portfolio.

What Are Mutual Fund Advisory Services?

Mutual fund advisory services help investors decide how mutual funds should fit into their larger financial plan. The work starts with your goals, current investments, liabilities, cash needs, and comfort with market movement.

A fund recommendation alone is not enough. Good advisory explains why a fund category belongs in your portfolio, how long you may hold it, and when the allocation needs review.

What Mutual Fund Advisory Services Cover

Mutual fund advisory can include:

Goal mapping for retirement, education, wealth creation, business liquidity, or legacy planning.

Risk profiling to understand how much volatility you can handle.

Asset allocation across equity, debt, hybrid, and other investment categories.

Fund-category selection based on the role each investment must play.

Portfolio review and rebalancing discussions.

Guidance on plan type, charges, documentation, and investor approval.

A mutual fund advisor should help you see the portfolio as one connected structure. This reduces the habit of adding multiple funds that hold similar securities or serve no clear goal.

What Mutual Fund Advisory Services Should Not Mean

Mutual fund advisory services should not mean guaranteed returns or frequent fund switching. They should also not become a sales conversation where the investor does not understand cost, risk, or the reason behind a recommendation.

A healthy advisory relationship leaves you with written clarity. You should know what you own, why you own it, and what may trigger a future change.

Why Use Mutual Fund Advisory Services?

Mutual fund advisory services are useful when an investor needs more than access to schemes. They can help connect financial goals, risk tolerance, investment horizon, and existing holdings before any new mutual fund is selected.

The value comes from having a clear order of decisions. The adviser should understand your situation first and then explain how each investment fits into your portfolio.

The main reasons investors use mutual fund advisory services include:

Goal-Based Planning: Retirement, children’s education, business expansion, emergency liquidity, and wealth transfer need different investment timelines. A short-term cash need should not be placed in the same category as a long-term retirement goal.

Fund Selection After Asset Allocation: Many investors start by asking for the best mutual fund. The better question is whether the portfolio needs equity exposure, debt stability, hybrid allocation, or liquidity support.

Portfolio Review and Rebalancing: Portfolio review checks whether your investments still match your original plan. It may identify duplicate funds, changes in category exposure, or an allocation that has moved away from your intended risk level.

Behavioural Support During Market Movement: Market falls can create panic, while market rallies can create overconfidence. A written investment plan gives investors a reference point before they redeem, add a risky category, or switch funds based on short-term performance.

For investors building post-work income, our guide to a retirement investment plan in India explains why the investment mix must reflect both future expenses and withdrawal needs. Similarly, our guide on asset allocation in India explains why fund selection should follow the investor’s actual financial needs.

Mutual fund advisory services cannot remove market risk. They can help investors make decisions with more discipline and less reaction, especially when different funds in the portfolio have different roles and time horizons.

“Mutual Fund investments are subject to market risks.” Source: AMFI Scheme Information Document A written investment plan does not remove market risk. It helps investors understand whether the risk taken matches the goal they are investing for. |

Types of Mutual Fund Advisory Services and Advisors in India

Not every person who helps you buy a mutual fund works under the same structure. The distinction matters because the service model, payment method, and recommendation process may differ.

Before you accept any recommendation, ask the professional how they are registered and how they earn from your investment.

SEBI Registered Investment Advisors

A SEBI Registered Investment Advisor generally provides investment advice for a fee paid by the client. The discussion may include financial goals, risk profile, asset allocation, and the suitability of different investment products.

An RIA relationship can suit investors who need planning depth and a written advisory process. Read our SEBI Registered Investment Advisor guide before deciding whether this model fits your needs.

Mutual Fund Distributors

Mutual fund distributors assist investors with mutual fund transactions and servicing. They may help with documentation, SIP setup, redemption requests, and regular portfolio communication.

Their route generally involves regular plans, where commissions may be paid by asset management companies. Investors should ask about plan type, commission disclosure, and the scope of ongoing support before proceeding.

Digital and Robo-Advisory Platforms

Digital platforms may offer online fund access, goal tracking, model portfolios, or portfolio reports. They can work for investors who are comfortable using technology and do not require frequent in-person discussions.

However, a digital platform may not understand business cash flows, family obligations, tax position, or succession needs in the same way as a detailed advisory meeting. The right choice depends on how much planning support you need.

The right mutual fund advisory service depends on the investor’s need for planning depth, servicing support, and personal involvement. A complex financial situation may require more than a transaction platform, while a simple portfolio may not need ongoing high-touch advice.

📊 SEBI’s intermediary register listed 1,037 investment advisers as of June 2026. Registration is an important first check, but it does not replace a discussion about fees, plan type, service scope, or transaction authority. Not sure whether you need an RIA, a distributor, or a digital platform? Talk to Our Advisor before choosing a service model. |

Finding Local Mutual Fund Advisory Services in Pune

A local mutual fund advisor in Pune can be useful when you prefer face-to-face conversations about family goals, business income, or a changing portfolio. But proximity should not be the only reason for selection.

Start with verification. Check the adviser’s registration, service model, fee structure, and written process before sharing financial details.

Check the Adviser’s Regulatory Identity

Ask whether the person acts as an investment adviser, mutual fund distributor, or both through separate entities. The answer tells you how advice, execution, and payment may work.

Do not rely only on visiting cards, social media profiles, or referrals. Check registration details through the relevant regulatory or industry records.

Ask How the Adviser Is Paid

The payment model should be explained in writing. You should understand advisory fees, distributor commissions, platform costs, and any other charges connected with your investments.

Cost is not the only factor. The larger concern is whether the professional clearly explains what service you receive for the money paid.

Ask About Direct and Regular Plans

Direct and regular plans differ in how the mutual fund is purchased and serviced. The right choice depends on whether you need ongoing support and how you evaluate the total cost of that support.

Our direct mutual fund versus regular mutual fund guide explains the difference in plain language. This question should be settled before the first investment is made.

Confirm the Review Process

Ask how often the portfolio is reviewed, what reports you receive, and how recommendations are documented. A review meeting should not only discuss recent returns.

It should also examine goal progress, asset allocation, fund role, liquidity needs, and changes in your financial life.

How Mutual Fund Advisory Services Work Before You Invest

Mutual fund advisory services should follow a clear process. The process protects both the investor and the adviser from decisions made without enough context.

A sound discussion should move from facts to goals, and then from goals to investment choices.

Financial facts and goals → Risk profile → Asset allocation → Fund category selection → Execution choice → Review and rebalancing

Step One: Financial Facts and Goal Mapping

The adviser reviews income, expenses, existing investments, liabilities, insurance, and near-term cash needs. This creates a clearer picture of what your money must do.

A business owner may need working-capital flexibility. A senior executive may need a retirement plan that accounts for future income needs and family commitments.

Step Two: Risk Profile and Time Horizon

Risk capacity and risk comfort are different. An investor may have a high income but still need low volatility because the money is required soon.

Time horizon also affects fund selection. Long-term goals may carry higher equity exposure, while near-term needs may require lower market risk.

Step Three: Fund Role and Category Selection

Each fund category should have a role. Equity funds may support long-term growth, while debt funds may serve stability and liquidity needs.

Before choosing schemes, understand the difference between equity and debt mutual funds. This reduces the risk of holding investments that do not match your expected holding period.

Step Four: Implementation and Documentation

The investor should receive clear information about the fund category, scheme, plan type, cost structure, and reason for selection. Consent should be recorded before transactions are made.

This is also the stage to check who can place transactions and what authority, if any, has been provided. Never assume that a verbal discussion is enough.

Step Five: Periodic Review

Portfolio review should focus on whether the plan still fits. It should not become a reason for unnecessary switching.

A review may lead to no change at all. Staying invested can be the right decision when the portfolio remains aligned with goals and risk profile.

Comparing Mutual Fund Advisory Services: RIA, Distributor, or Digital Platform?

The right mutual fund advisory service depends on how much planning support you need. It also depends on whether you want advice, transaction support, digital access, or a mix of these.

Use this comparison as a starting point. The final decision should follow a clear discussion about scope, cost, and responsibility.

Decision Factor | SEBI Registered Investment Advisor | Mutual Fund Distributor | Digital or Robo Platform |

How the service is paid | Client-paid advisory fee | Commission linked to distributed products | Platform or advisory charge |

Main purpose | Personal advice and financial planning | Fund access and transaction support | Digital investing and portfolio tracking |

Plan type discussion | Often includes direct-plan suitability | Generally involves regular plans | Depends on platform model |

Human involvement | Higher | Varies by distributor | Lower to moderate |

Suitable for | Investors needing planning depth | Investors needing servicing support | Investors comfortable with self-service |

The service type should match your needs. A complex financial situation may need more than a transaction platform, while a simple portfolio may not need ongoing high-touch advice.

How to Check Mutual Fund Advisory Services Before You Sign

Before you begin, ask questions that make the working relationship clear. The adviser should answer them without avoiding cost, authority, or plan-type discussions.

These questions also protect you from assumptions later.

“Will You Build a Plan or Only Suggest Funds?”

Ask whether the service includes goal planning, risk profiling, asset allocation, and portfolio review. A list of schemes without a broader plan may not address your actual needs.

The adviser should explain the role of each investment. You should not be left to guess why a fund was added.

“What Will I Pay and How Will It Be Disclosed?”

Ask for a written explanation of advisory fees, distributor commissions, fund costs, and platform charges. Read the document before you invest.

The cheapest option is not always the right one. But every cost should be clear and connected to a service you understand.

“Who Has Authority to Act on My Portfolio?”

Ask who can execute transactions and whether any mandate or consent is needed. Keep copies of forms, emails, statements, and written recommendations.

This matters when there is a disagreement later. Clear records help both the investor and the adviser understand what was agreed.

“What Will Be Reviewed After I Invest?”

A proper review should cover allocation, goal progress, fund overlap, portfolio risk, and financial changes. It should not only compare recent returns.

Ask how the adviser will communicate a recommended change. Written reasons are useful when you revisit the decision later.

“What Happens When My Goals Change?”

A change in business income, a planned home purchase, retirement timing, or family needs may require a portfolio review. The adviser should explain how these events affect the investment plan.

For broader planning needs, read our guide on when you may need a financial advisor in India. Mutual fund decisions become more useful when they are connected to the rest of your financial life.

📝 A fee, mandate, or plan type you do not understand today can create confusion later. Spreading wealth across mutual funds, PMS, and other assets without a coordinated view can also create blind spots. Schedule a consultation with Ckredence Wealth to review how your investments fit together. |

When Mutual Fund Advisory Services May Be Worth Paying For

Mutual fund advisory services can suit investors who need structure, regular review, or help connecting investments with life goals. They may be particularly relevant for business owners, senior executives, doctors, CAs, lawyers, and families with several financial priorities.

They are not automatically necessary for everyone. The value depends on your situation and the quality of the service.

Advisory May Help When

You have several financial goals but no clear investment map.

Your portfolio has overlapping schemes or unclear fund roles.

You do not have the time to review investments with discipline.

You react strongly to market movement.

You need a view across mutual funds, liquidity, taxes, retirement, and family goals.

DIY May Be Enough When

Your goals are simple and clearly documented.

You understand asset allocation and fund categories.

You can review your portfolio without chasing recent returns.

You do not need regular planning discussions.

Your investments have a clear role and are easy to monitor.

The decision does not need to be permanent. Your need for advice can change as your wealth, responsibilities, and financial goals change.

Why Choose Ckredence Wealth for Mutual Fund Advisory Services?

At Ckredence Wealth, mutual fund advisory starts with the investor’s financial situation rather than a scheme list. We discuss goals, risk profile, investment horizon, liquidity needs, and the role mutual funds should play in the larger portfolio.

Our discussions focus on:

Goal-based mutual fund planning for wealth creation, retirement, family needs, and liquidity.

Asset allocation before individual fund selection.

SIP planning, portfolio review, and documented recommendations.

Regular conversations when personal or financial circumstances change.

For investors whose needs extend beyond mutual funds, we also connect the discussion with broader financial planning. Bring your current mutual fund list to us, and we will help you identify the questions each holding should be able to answer.

✦ Portfolio Clarity Starts With Your Current List Do not begin with another scheme name. Start by reviewing whether each existing fund has a clear role in your financial plan. Start Your Portfolio Clarity Conversation with Ckredence Wealth. |

Conclusion

Mutual fund advisory services can help bring order to investments that have been added over time without a clear plan. The right relationship should explain the adviser’s role, payment method, plan type, recommendation process, and review approach before you invest. It should also give you a clearer view of how each fund supports a goal, time horizon, and level of risk.

A useful portfolio is not simply a collection of schemes. It should help you track retirement needs, family priorities, liquidity requirements, and long-term wealth plans with more clarity. Review your investments before adding another fund, especially when your income, responsibilities, or financial goals have changed.

FAQs

01.

What are mutual fund advisory services?

Mutual fund advisory services help investors set goals, choose fund categories, and review portfolios. They should explain costs, risks, plan type, and the reason behind recommendations.

02.

How does a SEBI Registered Investment Advisor differ from a mutual fund distributor?

A SEBI Registered Investment Advisor generally charges clients for investment advice. A mutual fund distributor supports transactions and may receive product-linked commission.

03.

Are direct mutual fund plans better than regular plans when using advisory services?

Direct plans may have lower fund expenses because they do not include distributor commission. Regular plans may suit investors who value distributor support and servicing.

04.

What should I check before giving a mutual fund advisor authority to act on my portfolio?

Check the written mandate, transaction authority, service scope, fee structure, and consent process. Keep copies of all forms, recommendations, and portfolio statements.

India’s mutual fund participation is rising, but investment decisions still need context. AMFI’s March SIP series moved from ₹14,276 crore in March 2023 to ₹19,271 crore in March 2024, ₹25,926 crore in March 2025, and ₹32,087 crore in March 2026. More people are investing through SIPs, yet many still choose funds before checking their financial goals, risk capacity, or existing allocation.

Does your current mutual fund portfolio match your retirement, business, family, and liquidity needs?

Do you know whether a recommendation comes from paid advice or product distribution?

Are you reviewing fund overlap, risk changes, and your changing financial priorities?

Mutual fund advisory services can bring structure to these questions. They help investors move from isolated fund purchases to a plan that connects money with purpose, time horizon, risk, and review discipline.

Figure: India’s March SIP Contributions | Source: AMFI monthly publications and annual reports

TL;DR

Mutual fund advisory services should begin with your goals, risk profile, and investment horizon.

Fund selection should follow asset allocation, not recent returns or online recommendations.

RIAs, distributors, and digital platforms work under different fee and service models.

Direct and regular plans should be discussed before you invest.

A portfolio review should check overlap, fund role, allocation drift, and changing financial needs.

Written recommendations and consent records reduce confusion around portfolio changes.

Advisory may suit investors who need planning support, but it is not necessary for every portfolio.

What Are Mutual Fund Advisory Services?

Mutual fund advisory services help investors decide how mutual funds should fit into their larger financial plan. The work starts with your goals, current investments, liabilities, cash needs, and comfort with market movement.

A fund recommendation alone is not enough. Good advisory explains why a fund category belongs in your portfolio, how long you may hold it, and when the allocation needs review.

What Mutual Fund Advisory Services Cover

Mutual fund advisory can include:

Goal mapping for retirement, education, wealth creation, business liquidity, or legacy planning.

Risk profiling to understand how much volatility you can handle.

Asset allocation across equity, debt, hybrid, and other investment categories.

Fund-category selection based on the role each investment must play.

Portfolio review and rebalancing discussions.

Guidance on plan type, charges, documentation, and investor approval.

A mutual fund advisor should help you see the portfolio as one connected structure. This reduces the habit of adding multiple funds that hold similar securities or serve no clear goal.

What Mutual Fund Advisory Services Should Not Mean

Mutual fund advisory services should not mean guaranteed returns or frequent fund switching. They should also not become a sales conversation where the investor does not understand cost, risk, or the reason behind a recommendation.

A healthy advisory relationship leaves you with written clarity. You should know what you own, why you own it, and what may trigger a future change.

Why Use Mutual Fund Advisory Services?

Mutual fund advisory services are useful when an investor needs more than access to schemes. They can help connect financial goals, risk tolerance, investment horizon, and existing holdings before any new mutual fund is selected.

The value comes from having a clear order of decisions. The adviser should understand your situation first and then explain how each investment fits into your portfolio.

The main reasons investors use mutual fund advisory services include:

Goal-Based Planning: Retirement, children’s education, business expansion, emergency liquidity, and wealth transfer need different investment timelines. A short-term cash need should not be placed in the same category as a long-term retirement goal.

Fund Selection After Asset Allocation: Many investors start by asking for the best mutual fund. The better question is whether the portfolio needs equity exposure, debt stability, hybrid allocation, or liquidity support.

Portfolio Review and Rebalancing: Portfolio review checks whether your investments still match your original plan. It may identify duplicate funds, changes in category exposure, or an allocation that has moved away from your intended risk level.

Behavioural Support During Market Movement: Market falls can create panic, while market rallies can create overconfidence. A written investment plan gives investors a reference point before they redeem, add a risky category, or switch funds based on short-term performance.

For investors building post-work income, our guide to a retirement investment plan in India explains why the investment mix must reflect both future expenses and withdrawal needs. Similarly, our guide on asset allocation in India explains why fund selection should follow the investor’s actual financial needs.

Mutual fund advisory services cannot remove market risk. They can help investors make decisions with more discipline and less reaction, especially when different funds in the portfolio have different roles and time horizons.

“Mutual Fund investments are subject to market risks.” Source: AMFI Scheme Information Document A written investment plan does not remove market risk. It helps investors understand whether the risk taken matches the goal they are investing for. |

Types of Mutual Fund Advisory Services and Advisors in India

Not every person who helps you buy a mutual fund works under the same structure. The distinction matters because the service model, payment method, and recommendation process may differ.

Before you accept any recommendation, ask the professional how they are registered and how they earn from your investment.

SEBI Registered Investment Advisors

A SEBI Registered Investment Advisor generally provides investment advice for a fee paid by the client. The discussion may include financial goals, risk profile, asset allocation, and the suitability of different investment products.

An RIA relationship can suit investors who need planning depth and a written advisory process. Read our SEBI Registered Investment Advisor guide before deciding whether this model fits your needs.

Mutual Fund Distributors

Mutual fund distributors assist investors with mutual fund transactions and servicing. They may help with documentation, SIP setup, redemption requests, and regular portfolio communication.

Their route generally involves regular plans, where commissions may be paid by asset management companies. Investors should ask about plan type, commission disclosure, and the scope of ongoing support before proceeding.

Digital and Robo-Advisory Platforms

Digital platforms may offer online fund access, goal tracking, model portfolios, or portfolio reports. They can work for investors who are comfortable using technology and do not require frequent in-person discussions.

However, a digital platform may not understand business cash flows, family obligations, tax position, or succession needs in the same way as a detailed advisory meeting. The right choice depends on how much planning support you need.

The right mutual fund advisory service depends on the investor’s need for planning depth, servicing support, and personal involvement. A complex financial situation may require more than a transaction platform, while a simple portfolio may not need ongoing high-touch advice.

📊 SEBI’s intermediary register listed 1,037 investment advisers as of June 2026. Registration is an important first check, but it does not replace a discussion about fees, plan type, service scope, or transaction authority. Not sure whether you need an RIA, a distributor, or a digital platform? Talk to Our Advisor before choosing a service model. |

Finding Local Mutual Fund Advisory Services in Pune

A local mutual fund advisor in Pune can be useful when you prefer face-to-face conversations about family goals, business income, or a changing portfolio. But proximity should not be the only reason for selection.

Start with verification. Check the adviser’s registration, service model, fee structure, and written process before sharing financial details.

Check the Adviser’s Regulatory Identity

Ask whether the person acts as an investment adviser, mutual fund distributor, or both through separate entities. The answer tells you how advice, execution, and payment may work.

Do not rely only on visiting cards, social media profiles, or referrals. Check registration details through the relevant regulatory or industry records.

Ask How the Adviser Is Paid

The payment model should be explained in writing. You should understand advisory fees, distributor commissions, platform costs, and any other charges connected with your investments.

Cost is not the only factor. The larger concern is whether the professional clearly explains what service you receive for the money paid.

Ask About Direct and Regular Plans

Direct and regular plans differ in how the mutual fund is purchased and serviced. The right choice depends on whether you need ongoing support and how you evaluate the total cost of that support.

Our direct mutual fund versus regular mutual fund guide explains the difference in plain language. This question should be settled before the first investment is made.

Confirm the Review Process

Ask how often the portfolio is reviewed, what reports you receive, and how recommendations are documented. A review meeting should not only discuss recent returns.

It should also examine goal progress, asset allocation, fund role, liquidity needs, and changes in your financial life.

How Mutual Fund Advisory Services Work Before You Invest

Mutual fund advisory services should follow a clear process. The process protects both the investor and the adviser from decisions made without enough context.

A sound discussion should move from facts to goals, and then from goals to investment choices.

Financial facts and goals → Risk profile → Asset allocation → Fund category selection → Execution choice → Review and rebalancing

Step One: Financial Facts and Goal Mapping

The adviser reviews income, expenses, existing investments, liabilities, insurance, and near-term cash needs. This creates a clearer picture of what your money must do.

A business owner may need working-capital flexibility. A senior executive may need a retirement plan that accounts for future income needs and family commitments.

Step Two: Risk Profile and Time Horizon

Risk capacity and risk comfort are different. An investor may have a high income but still need low volatility because the money is required soon.

Time horizon also affects fund selection. Long-term goals may carry higher equity exposure, while near-term needs may require lower market risk.

Step Three: Fund Role and Category Selection

Each fund category should have a role. Equity funds may support long-term growth, while debt funds may serve stability and liquidity needs.

Before choosing schemes, understand the difference between equity and debt mutual funds. This reduces the risk of holding investments that do not match your expected holding period.

Step Four: Implementation and Documentation

The investor should receive clear information about the fund category, scheme, plan type, cost structure, and reason for selection. Consent should be recorded before transactions are made.

This is also the stage to check who can place transactions and what authority, if any, has been provided. Never assume that a verbal discussion is enough.

Step Five: Periodic Review

Portfolio review should focus on whether the plan still fits. It should not become a reason for unnecessary switching.

A review may lead to no change at all. Staying invested can be the right decision when the portfolio remains aligned with goals and risk profile.

Comparing Mutual Fund Advisory Services: RIA, Distributor, or Digital Platform?

The right mutual fund advisory service depends on how much planning support you need. It also depends on whether you want advice, transaction support, digital access, or a mix of these.

Use this comparison as a starting point. The final decision should follow a clear discussion about scope, cost, and responsibility.

Decision Factor | SEBI Registered Investment Advisor | Mutual Fund Distributor | Digital or Robo Platform |

How the service is paid | Client-paid advisory fee | Commission linked to distributed products | Platform or advisory charge |

Main purpose | Personal advice and financial planning | Fund access and transaction support | Digital investing and portfolio tracking |

Plan type discussion | Often includes direct-plan suitability | Generally involves regular plans | Depends on platform model |

Human involvement | Higher | Varies by distributor | Lower to moderate |

Suitable for | Investors needing planning depth | Investors needing servicing support | Investors comfortable with self-service |

The service type should match your needs. A complex financial situation may need more than a transaction platform, while a simple portfolio may not need ongoing high-touch advice.

How to Check Mutual Fund Advisory Services Before You Sign

Before you begin, ask questions that make the working relationship clear. The adviser should answer them without avoiding cost, authority, or plan-type discussions.

These questions also protect you from assumptions later.

“Will You Build a Plan or Only Suggest Funds?”

Ask whether the service includes goal planning, risk profiling, asset allocation, and portfolio review. A list of schemes without a broader plan may not address your actual needs.

The adviser should explain the role of each investment. You should not be left to guess why a fund was added.

“What Will I Pay and How Will It Be Disclosed?”

Ask for a written explanation of advisory fees, distributor commissions, fund costs, and platform charges. Read the document before you invest.

The cheapest option is not always the right one. But every cost should be clear and connected to a service you understand.

“Who Has Authority to Act on My Portfolio?”

Ask who can execute transactions and whether any mandate or consent is needed. Keep copies of forms, emails, statements, and written recommendations.

This matters when there is a disagreement later. Clear records help both the investor and the adviser understand what was agreed.

“What Will Be Reviewed After I Invest?”

A proper review should cover allocation, goal progress, fund overlap, portfolio risk, and financial changes. It should not only compare recent returns.

Ask how the adviser will communicate a recommended change. Written reasons are useful when you revisit the decision later.

“What Happens When My Goals Change?”

A change in business income, a planned home purchase, retirement timing, or family needs may require a portfolio review. The adviser should explain how these events affect the investment plan.

For broader planning needs, read our guide on when you may need a financial advisor in India. Mutual fund decisions become more useful when they are connected to the rest of your financial life.

📝 A fee, mandate, or plan type you do not understand today can create confusion later. Spreading wealth across mutual funds, PMS, and other assets without a coordinated view can also create blind spots. Schedule a consultation with Ckredence Wealth to review how your investments fit together. |

When Mutual Fund Advisory Services May Be Worth Paying For

Mutual fund advisory services can suit investors who need structure, regular review, or help connecting investments with life goals. They may be particularly relevant for business owners, senior executives, doctors, CAs, lawyers, and families with several financial priorities.

They are not automatically necessary for everyone. The value depends on your situation and the quality of the service.

Advisory May Help When

You have several financial goals but no clear investment map.

Your portfolio has overlapping schemes or unclear fund roles.

You do not have the time to review investments with discipline.

You react strongly to market movement.

You need a view across mutual funds, liquidity, taxes, retirement, and family goals.

DIY May Be Enough When

Your goals are simple and clearly documented.

You understand asset allocation and fund categories.

You can review your portfolio without chasing recent returns.

You do not need regular planning discussions.

Your investments have a clear role and are easy to monitor.

The decision does not need to be permanent. Your need for advice can change as your wealth, responsibilities, and financial goals change.

Why Choose Ckredence Wealth for Mutual Fund Advisory Services?

At Ckredence Wealth, mutual fund advisory starts with the investor’s financial situation rather than a scheme list. We discuss goals, risk profile, investment horizon, liquidity needs, and the role mutual funds should play in the larger portfolio.

Our discussions focus on:

Goal-based mutual fund planning for wealth creation, retirement, family needs, and liquidity.

Asset allocation before individual fund selection.

SIP planning, portfolio review, and documented recommendations.

Regular conversations when personal or financial circumstances change.

For investors whose needs extend beyond mutual funds, we also connect the discussion with broader financial planning. Bring your current mutual fund list to us, and we will help you identify the questions each holding should be able to answer.

✦ Portfolio Clarity Starts With Your Current List Do not begin with another scheme name. Start by reviewing whether each existing fund has a clear role in your financial plan. Start Your Portfolio Clarity Conversation with Ckredence Wealth. |

Conclusion

Mutual fund advisory services can help bring order to investments that have been added over time without a clear plan. The right relationship should explain the adviser’s role, payment method, plan type, recommendation process, and review approach before you invest. It should also give you a clearer view of how each fund supports a goal, time horizon, and level of risk.

A useful portfolio is not simply a collection of schemes. It should help you track retirement needs, family priorities, liquidity requirements, and long-term wealth plans with more clarity. Review your investments before adding another fund, especially when your income, responsibilities, or financial goals have changed.

FAQs

01.

What are mutual fund advisory services?

Mutual fund advisory services help investors set goals, choose fund categories, and review portfolios. They should explain costs, risks, plan type, and the reason behind recommendations.

02.

How does a SEBI Registered Investment Advisor differ from a mutual fund distributor?

A SEBI Registered Investment Advisor generally charges clients for investment advice. A mutual fund distributor supports transactions and may receive product-linked commission.

03.

Are direct mutual fund plans better than regular plans when using advisory services?

Direct plans may have lower fund expenses because they do not include distributor commission. Regular plans may suit investors who value distributor support and servicing.

04.

What should I check before giving a mutual fund advisor authority to act on my portfolio?

Check the written mandate, transaction authority, service scope, fee structure, and consent process. Keep copies of all forms, recommendations, and portfolio statements.