13min Read

13min Read

Financial Advisory Services India: Do You Really Need a Financial Advisor in 2026?

Financial Advisory Services India: Do You Really Need a Financial Advisor in 2026?

Financial Advisory Services India: Do You Really Need a Financial Advisor in 2026?

Most financial advice in India still runs on product commissions, not fiduciary duty. Learn the signs you need a SEBI-registered advisor in 2026.

Most financial advice in India still runs on product commissions, not fiduciary duty. Learn the signs you need a SEBI-registered advisor in 2026.

Most financial advice in India still runs on product commissions, not fiduciary duty. Learn the signs you need a SEBI-registered advisor in 2026.

Ckredence Wealth

Ckredence Wealth

|

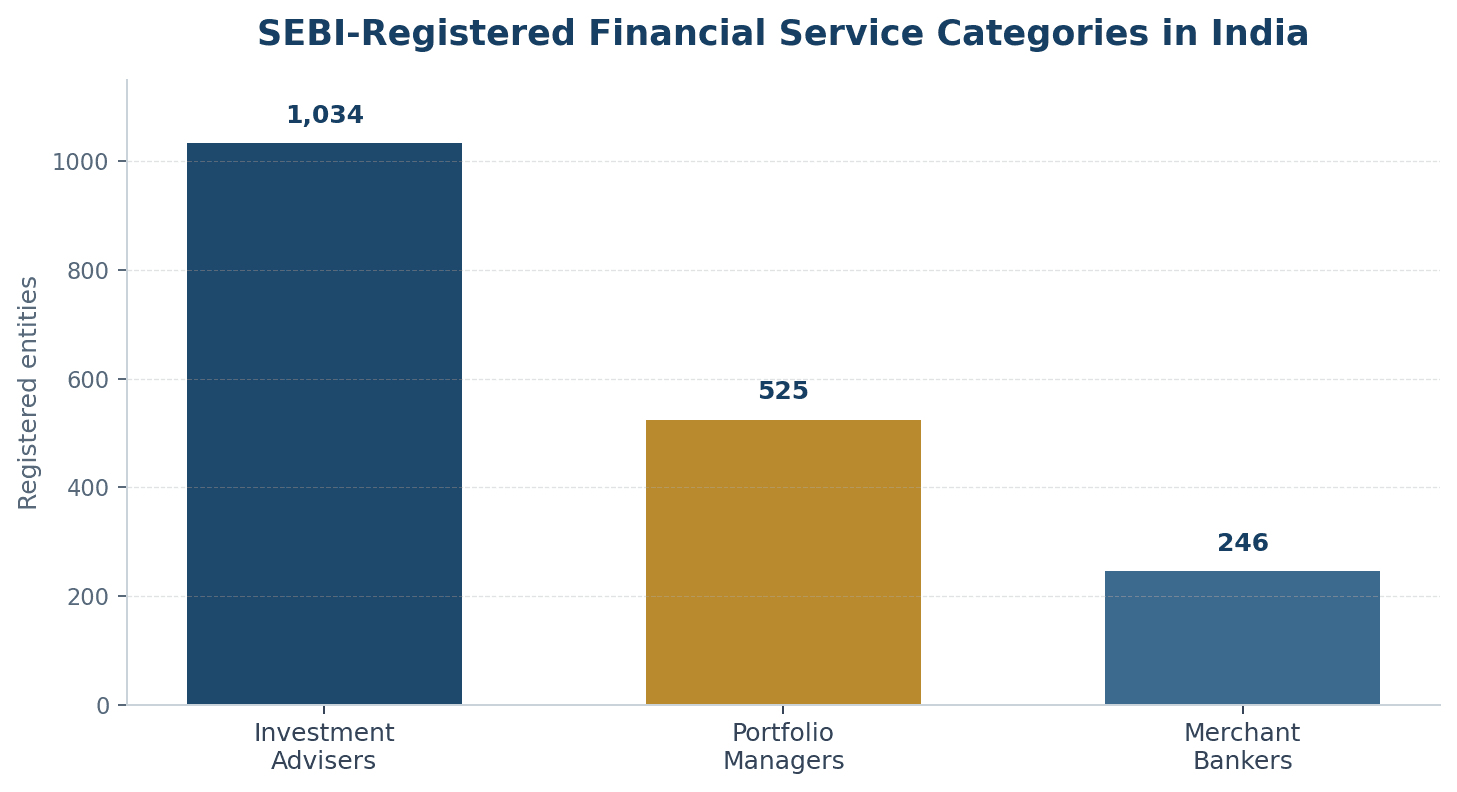

As of June 2026, SEBI listed 1,034 Investment Advisers, 525 Portfolio Managers, and 246 Merchant Bankers. These categories serve very different needs, from personal wealth planning and portfolio advice to business funding, mergers, valuations, and transaction support.

Are you looking for help with your investments or a business financial decision?

Do you know whether your adviser earns through fees, commissions, or transactions?

Does your current portfolio reflect your goals, liquidity needs, and comfort with risk?

Financial advisory services in India can refer to personal wealth advice or corporate finance support. The right choice depends on the decision you need to make, not simply on the amount you plan to invest.

Figure: SEBI-registered financial service categories in India. Source: SEBI Recognised Intermediaries, June 2026.

TL;DR

Financial advisory services in India can cover personal wealth decisions or corporate finance needs.

SEBI Registered Investment Advisers, distributors, wealth managers, and corporate advisers have different roles.

Personal advice should begin with goals, risk profile, liquidity needs, and asset allocation.

Mutual fund distribution and investment advice follow different payment models.

Corporate advisory may include capital raising, business valuation, restructuring, or transaction support.

Ask for fee disclosures, service scope, product rationale, and review frequency before signing up.

The right adviser depends on your financial complexity, not only your portfolio value.

What Are Financial Advisory Services in India?

Financial advisory services in India help individuals, families, companies, and institutions make informed financial decisions. The work can involve investments, tax coordination, retirement planning, business valuation, capital raising, restructuring, or transaction support.

The term is broad. That is why many readers compare services that are not meant for the same purpose.

Personal Financial Advisory Services

Personal financial advisory focuses on an individual or family’s money decisions. It may cover financial goals, risk profile, asset allocation, mutual funds, PMS, debt, liquidity, retirement, and wealth transfer planning.

The starting point should be the investor’s full financial position. A list of funds or stocks without that context may not solve the actual problem.

Corporate Financial Advisory Services

Corporate financial advisory focuses on business-level decisions. It may involve funding, debt structuring, valuation, business sale, mergers, acquisition support, restructuring, or public-market preparation.

This work is generally relevant for business owners, promoters, CFOs, institutions, and government entities. It is different from personal investment planning.

Personal financial advice helps you decide what your money should do. Corporate financial advice helps a business decide how capital, ownership, and transactions should be handled. |

Personal Financial Advisory Services in India

Personal financial advisory services help investors connect money decisions with future goals. The work should move from financial facts to asset allocation and then to investment selection.

A strong process does not begin with a product recommendation. It begins with questions about income, liabilities, dependants, existing investments, emergency needs, and future responsibilities.

SEBI Registered Investment Advisers

A SEBI Registered Investment Adviser provides personalised investment guidance based on a client’s goals, risk appetite, and financial position. Advisers charge clients directly and are expected to follow fiduciary standards.

This model may suit investors who want a written investment view, allocation guidance, and periodic review. Before working with an adviser, verify the registration and understand the scope of advice.

Fee-Only Financial Planners

A fee-only planner is paid directly by the client rather than through product commissions. The work may include goal planning, cash-flow review, retirement planning, insurance review, and portfolio guidance.

Ask what the fee includes. Some planners may provide a financial plan only, while others may also support implementation and review discussions.

Wealth Management Services

Wealth management is generally useful when the financial picture includes several asset classes, family wealth, business proceeds, estate planning, or succession needs. The service may cover investments, liquidity planning, tax coordination, and family-level decisions.

The exact scope varies by firm. Investors should ask which activities are advisory, which are execution-related, and which are handled by external professionals.

Mutual Fund Distribution and Execution Support

Mutual fund distributors can help investors with transactions, SIP setup, paperwork, servicing, and portfolio communication. Under AMFI guidance, distributors may receive trail commission on regular-plan investments.

This model may help investors who need transaction support. However, investors should understand the difference between mutual fund advisory services, direct plans, regular plans, and distributor compensation before investing.

“The right adviser should explain the role of every investment before asking you to buy it.” |

Corporate Financial Advisory Services in India

Corporate financial advisory services focus on business value, capital, ownership, and transactions. This includes areas such as funding, debt structuring, valuation, due diligence, mergers, business sale, restructuring, and public-market preparation.

Corporate advisory is not meant for an individual deciding between mutual funds and direct equity. It is generally used when a company needs support for a financial event or long-term business decision.

Corporate Need | Typical Advisory Support |

|---|---|

Capital requirement | Debt planning, equity funding, private capital discussions |

Business sale or acquisition | Valuation, due diligence, negotiation, transaction support |

Restructuring need | Capital review, debt restructuring, ownership planning |

Public-market preparation | Valuation, documentation, investor communication, compliance support |

Government or infrastructure project | Financial appraisal, bid support, transaction planning |

Corporate financial advisory firms often work with promoters, CFOs, institutional investors, and public-sector entities. Personal wealth advisory should remain a separate discussion even when a business owner has both personal and corporate financial needs.

Financial Advisory Services India: RIA vs Distributor vs Wealth Manager vs Corporate Adviser

The adviser type should match the decision you need to make. A mismatch can create confusion around fees, service scope, responsibility, and product recommendations.

Use this comparison before deciding who to approach.

Decision Factor | SEBI Registered Investment Adviser | Mutual Fund Distributor | Wealth Manager | Corporate Financial Adviser |

|---|---|---|---|---|

Main client need | Personal advice and planning | Investment execution and servicing | Family wealth and multi-asset planning | Business finance and transactions |

Payment approach | Client-paid advisory fee | Product-linked commission may apply | Fee, asset-linked fee, or service-based model | Project, retainer, or transaction-linked fee |

Main work | Goals, allocation, portfolio advice | Mutual fund access and support | Investments, liquidity, estate, family wealth | Funding, valuation, M&A, restructuring |

Suitable for | Investors needing written advice | Investors needing investment support | HNIs, founders, executives, families | Promoters, companies, CFOs |

A distributor is not automatically unsuitable, and an RIA is not automatically needed for every investor. The point is to understand the model before acting on a recommendation.

Not sure whether you need a financial plan, investment support, or a wider wealth review? Map your current holdings against your goals before selecting a service model. |

How Financial Advisory Services in India Should Work

A useful advisory process follows a clear sequence. It should move from financial facts to goals, then from goals to asset allocation and investment decisions.

Financial facts → Goals → Risk profile → Asset allocation

Investment selection → Portfolio review

Financial Facts and Goal Mapping

The adviser should first understand income, liabilities, insurance, existing investments, cash needs, family responsibilities, and future plans. This gives each investment a purpose.

For example, money meant for near-term liquidity should not be treated like retirement capital. The goal decides the time horizon and acceptable risk.

Risk Capacity and Risk Comfort

Risk capacity refers to how much market movement an investor can financially handle. Risk comfort refers to how much volatility an investor can emotionally accept.

Both matter. A high-income professional may still need low-risk investments for upcoming commitments or family needs.

Asset Allocation Before Product Selection

Asset allocation decides how money is split across equity, debt, cash, gold, and other investment categories. Product selection should come after this decision, not before it.

Our guide to asset allocation in India explains why a portfolio should be built around financial purpose rather than recent returns.

Portfolio Review and Rebalancing

Portfolio review checks whether investments still match goals, risk level, and liquidity needs. It can also identify duplicate funds, hidden concentration, or an investment that no longer has a role.

A review may lead to changes, but it does not always require action. Sometimes the right decision is to stay with a plan that still fits.

How to Choose Financial Advisory Services in India

Selecting an adviser should involve more than checking online reviews or past returns. You should understand the adviser’s registration, payment model, role, and review process.

The questions below help investors compare services without relying only on brand names.

Check Regulatory Identity

Ask whether the person is a SEBI Registered Investment Adviser, mutual fund distributor, broker, portfolio manager, wealth manager, or corporate adviser. The answer affects the type of guidance and service you may receive.

Registration can be verified through the relevant regulator or industry body. Do not treat a social-media profile or visiting card as proof of regulatory status.

Ask How the Adviser Is Paid

Ask about advisory fees, asset-linked fees, transaction fees, trail commissions, and any product-linked compensation. The answer should be available in writing.

Fees alone do not decide whether a service is suitable. However, unclear compensation can make it hard to understand possible conflicts.

Review the Scope of Work

Clarify whether the service includes financial planning, investment selection, tax coordination, insurance review, estate planning, implementation, or portfolio review. Some services may only provide product access.

A defined scope avoids disappointment later. It also helps investors compare one adviser with another on the same basis.

Ask for Written Documentation

A good advisory relationship should have clear records. These may include a financial plan, investment rationale, fee disclosure, review approach, and notes on recommended changes.

Documentation helps investors understand why an action was taken. It also makes future reviews more useful.

Check Product Bias

Ask whether the adviser can explain why a product fits your goals and what alternatives were considered. A product should have a stated role in the portfolio.

Investors comparing managed equity options can read PMS vs mutual funds vs AIFs before treating one structure as a replacement for another.

A portfolio can hold many investments and still lack direction. Before adding another fund, PMS, policy, or stock, review what the current holdings are meant to do. |

When Financial Advisory Services in India May Help

Financial advisory services may be useful when financial decisions become harder to manage alone. This often happens when income grows, investments spread across products, family responsibilities change, or business wealth becomes part of the picture.

Advice is not only for large portfolios. It may be useful when a wrong decision could affect liquidity, retirement, taxes, or family plans.

Financial Situation | Why Advisory May Help |

|---|---|

Several financial goals | Helps assign investments to specific goals |

Scattered investments | Helps identify overlap and missing allocation |

Business income or sale proceeds | Helps separate personal wealth from business capital |

Retirement or education planning | Helps link time horizon with risk and liquidity |

Family wealth or succession needs | Helps coordinate investments with long-term transfer plans |

Advisory may not be needed immediately when goals are simple, the portfolio is easy to monitor, and the investor understands costs and allocation. The right level of support should match the complexity of the decision.

For investors planning life after active income, our guide to a retirement investment plan in India explains how future income needs can affect investment choices.

Why Choose Ckredence Wealth for Financial Advisory Services in India?

At Ckredence Wealth, financial advisory begins with the investor’s full financial situation rather than a single product. We discuss goals, liquidity needs, risk capacity, current holdings, and the role each investment should play.

Our discussions focus on:

Asset allocation before product selection.

Mutual funds, PMS, equity, debt, liquidity, and family wealth decisions in one view.

Portfolio reviews when income, family commitments, business responsibilities, or goals change.

Clearer understanding of what each holding adds to the portfolio.

For investors who are deciding between broader wealth planning and focused investment management, our guide to wealth management versus portfolio management explains the difference.

Before your next investment becomes another line in a scattered portfolio, give it a role. Bring your current holdings, financial goals, and upcoming commitments. Leave with a clearer view of what each investment should do and what needs review. |

Conclusion

Financial advisory services in India can cover personal wealth planning, investment advice, family wealth decisions, or corporate finance work. The right adviser should match the actual decision you need help with, rather than simply present a product or service package.

A useful financial plan begins with goals, risk, liquidity, and asset allocation. Registration, fees, service scope, and review process should be clear before money is invested or a long-term advisory relationship begins.

FAQs

01.

What are financial advisory services in India?

Financial advisory services help individuals, families, and businesses make structured financial decisions. They may cover investments, retirement, funding, valuation, or transaction support.

02.

How is a SEBI Registered Investment Adviser different from a mutual fund distributor?

A SEBI Registered Investment Adviser charges clients directly for personalised investment advice. A mutual fund distributor may receive trail commission for regular-plan transactions.

03.

What is the difference between personal and corporate financial advisory?

Personal financial advisory focuses on investments, life goals, and family wealth. Corporate financial advisory focuses on funding, valuation, mergers, restructuring, and business transactions.

04.

How should I choose a financial adviser in India?

Check regulatory identity, payment model, service scope, written documentation, and review process. Choose an adviser whose role matches your financial needs.

As of June 2026, SEBI listed 1,034 Investment Advisers, 525 Portfolio Managers, and 246 Merchant Bankers. These categories serve very different needs, from personal wealth planning and portfolio advice to business funding, mergers, valuations, and transaction support.

Are you looking for help with your investments or a business financial decision?

Do you know whether your adviser earns through fees, commissions, or transactions?

Does your current portfolio reflect your goals, liquidity needs, and comfort with risk?

Financial advisory services in India can refer to personal wealth advice or corporate finance support. The right choice depends on the decision you need to make, not simply on the amount you plan to invest.

Figure: SEBI-registered financial service categories in India. Source: SEBI Recognised Intermediaries, June 2026.

TL;DR

Financial advisory services in India can cover personal wealth decisions or corporate finance needs.

SEBI Registered Investment Advisers, distributors, wealth managers, and corporate advisers have different roles.

Personal advice should begin with goals, risk profile, liquidity needs, and asset allocation.

Mutual fund distribution and investment advice follow different payment models.

Corporate advisory may include capital raising, business valuation, restructuring, or transaction support.

Ask for fee disclosures, service scope, product rationale, and review frequency before signing up.

The right adviser depends on your financial complexity, not only your portfolio value.

What Are Financial Advisory Services in India?

Financial advisory services in India help individuals, families, companies, and institutions make informed financial decisions. The work can involve investments, tax coordination, retirement planning, business valuation, capital raising, restructuring, or transaction support.

The term is broad. That is why many readers compare services that are not meant for the same purpose.

Personal Financial Advisory Services

Personal financial advisory focuses on an individual or family’s money decisions. It may cover financial goals, risk profile, asset allocation, mutual funds, PMS, debt, liquidity, retirement, and wealth transfer planning.

The starting point should be the investor’s full financial position. A list of funds or stocks without that context may not solve the actual problem.

Corporate Financial Advisory Services

Corporate financial advisory focuses on business-level decisions. It may involve funding, debt structuring, valuation, business sale, mergers, acquisition support, restructuring, or public-market preparation.

This work is generally relevant for business owners, promoters, CFOs, institutions, and government entities. It is different from personal investment planning.

Personal financial advice helps you decide what your money should do. Corporate financial advice helps a business decide how capital, ownership, and transactions should be handled. |

Personal Financial Advisory Services in India

Personal financial advisory services help investors connect money decisions with future goals. The work should move from financial facts to asset allocation and then to investment selection.

A strong process does not begin with a product recommendation. It begins with questions about income, liabilities, dependants, existing investments, emergency needs, and future responsibilities.

SEBI Registered Investment Advisers

A SEBI Registered Investment Adviser provides personalised investment guidance based on a client’s goals, risk appetite, and financial position. Advisers charge clients directly and are expected to follow fiduciary standards.

This model may suit investors who want a written investment view, allocation guidance, and periodic review. Before working with an adviser, verify the registration and understand the scope of advice.

Fee-Only Financial Planners

A fee-only planner is paid directly by the client rather than through product commissions. The work may include goal planning, cash-flow review, retirement planning, insurance review, and portfolio guidance.

Ask what the fee includes. Some planners may provide a financial plan only, while others may also support implementation and review discussions.

Wealth Management Services

Wealth management is generally useful when the financial picture includes several asset classes, family wealth, business proceeds, estate planning, or succession needs. The service may cover investments, liquidity planning, tax coordination, and family-level decisions.

The exact scope varies by firm. Investors should ask which activities are advisory, which are execution-related, and which are handled by external professionals.

Mutual Fund Distribution and Execution Support

Mutual fund distributors can help investors with transactions, SIP setup, paperwork, servicing, and portfolio communication. Under AMFI guidance, distributors may receive trail commission on regular-plan investments.

This model may help investors who need transaction support. However, investors should understand the difference between mutual fund advisory services, direct plans, regular plans, and distributor compensation before investing.

“The right adviser should explain the role of every investment before asking you to buy it.” |

Corporate Financial Advisory Services in India

Corporate financial advisory services focus on business value, capital, ownership, and transactions. This includes areas such as funding, debt structuring, valuation, due diligence, mergers, business sale, restructuring, and public-market preparation.

Corporate advisory is not meant for an individual deciding between mutual funds and direct equity. It is generally used when a company needs support for a financial event or long-term business decision.

Corporate Need | Typical Advisory Support |

|---|---|

Capital requirement | Debt planning, equity funding, private capital discussions |

Business sale or acquisition | Valuation, due diligence, negotiation, transaction support |

Restructuring need | Capital review, debt restructuring, ownership planning |

Public-market preparation | Valuation, documentation, investor communication, compliance support |

Government or infrastructure project | Financial appraisal, bid support, transaction planning |

Corporate financial advisory firms often work with promoters, CFOs, institutional investors, and public-sector entities. Personal wealth advisory should remain a separate discussion even when a business owner has both personal and corporate financial needs.

Financial Advisory Services India: RIA vs Distributor vs Wealth Manager vs Corporate Adviser

The adviser type should match the decision you need to make. A mismatch can create confusion around fees, service scope, responsibility, and product recommendations.

Use this comparison before deciding who to approach.

Decision Factor | SEBI Registered Investment Adviser | Mutual Fund Distributor | Wealth Manager | Corporate Financial Adviser |

|---|---|---|---|---|

Main client need | Personal advice and planning | Investment execution and servicing | Family wealth and multi-asset planning | Business finance and transactions |

Payment approach | Client-paid advisory fee | Product-linked commission may apply | Fee, asset-linked fee, or service-based model | Project, retainer, or transaction-linked fee |

Main work | Goals, allocation, portfolio advice | Mutual fund access and support | Investments, liquidity, estate, family wealth | Funding, valuation, M&A, restructuring |

Suitable for | Investors needing written advice | Investors needing investment support | HNIs, founders, executives, families | Promoters, companies, CFOs |

A distributor is not automatically unsuitable, and an RIA is not automatically needed for every investor. The point is to understand the model before acting on a recommendation.

Not sure whether you need a financial plan, investment support, or a wider wealth review? Map your current holdings against your goals before selecting a service model. |

How Financial Advisory Services in India Should Work

A useful advisory process follows a clear sequence. It should move from financial facts to goals, then from goals to asset allocation and investment decisions.

Financial facts → Goals → Risk profile → Asset allocation

Investment selection → Portfolio review

Financial Facts and Goal Mapping

The adviser should first understand income, liabilities, insurance, existing investments, cash needs, family responsibilities, and future plans. This gives each investment a purpose.

For example, money meant for near-term liquidity should not be treated like retirement capital. The goal decides the time horizon and acceptable risk.

Risk Capacity and Risk Comfort

Risk capacity refers to how much market movement an investor can financially handle. Risk comfort refers to how much volatility an investor can emotionally accept.

Both matter. A high-income professional may still need low-risk investments for upcoming commitments or family needs.

Asset Allocation Before Product Selection

Asset allocation decides how money is split across equity, debt, cash, gold, and other investment categories. Product selection should come after this decision, not before it.

Our guide to asset allocation in India explains why a portfolio should be built around financial purpose rather than recent returns.

Portfolio Review and Rebalancing

Portfolio review checks whether investments still match goals, risk level, and liquidity needs. It can also identify duplicate funds, hidden concentration, or an investment that no longer has a role.

A review may lead to changes, but it does not always require action. Sometimes the right decision is to stay with a plan that still fits.

How to Choose Financial Advisory Services in India

Selecting an adviser should involve more than checking online reviews or past returns. You should understand the adviser’s registration, payment model, role, and review process.

The questions below help investors compare services without relying only on brand names.

Check Regulatory Identity

Ask whether the person is a SEBI Registered Investment Adviser, mutual fund distributor, broker, portfolio manager, wealth manager, or corporate adviser. The answer affects the type of guidance and service you may receive.

Registration can be verified through the relevant regulator or industry body. Do not treat a social-media profile or visiting card as proof of regulatory status.

Ask How the Adviser Is Paid

Ask about advisory fees, asset-linked fees, transaction fees, trail commissions, and any product-linked compensation. The answer should be available in writing.

Fees alone do not decide whether a service is suitable. However, unclear compensation can make it hard to understand possible conflicts.

Review the Scope of Work

Clarify whether the service includes financial planning, investment selection, tax coordination, insurance review, estate planning, implementation, or portfolio review. Some services may only provide product access.

A defined scope avoids disappointment later. It also helps investors compare one adviser with another on the same basis.

Ask for Written Documentation

A good advisory relationship should have clear records. These may include a financial plan, investment rationale, fee disclosure, review approach, and notes on recommended changes.

Documentation helps investors understand why an action was taken. It also makes future reviews more useful.

Check Product Bias

Ask whether the adviser can explain why a product fits your goals and what alternatives were considered. A product should have a stated role in the portfolio.

Investors comparing managed equity options can read PMS vs mutual funds vs AIFs before treating one structure as a replacement for another.

A portfolio can hold many investments and still lack direction. Before adding another fund, PMS, policy, or stock, review what the current holdings are meant to do. |

When Financial Advisory Services in India May Help

Financial advisory services may be useful when financial decisions become harder to manage alone. This often happens when income grows, investments spread across products, family responsibilities change, or business wealth becomes part of the picture.

Advice is not only for large portfolios. It may be useful when a wrong decision could affect liquidity, retirement, taxes, or family plans.

Financial Situation | Why Advisory May Help |

|---|---|

Several financial goals | Helps assign investments to specific goals |

Scattered investments | Helps identify overlap and missing allocation |

Business income or sale proceeds | Helps separate personal wealth from business capital |

Retirement or education planning | Helps link time horizon with risk and liquidity |

Family wealth or succession needs | Helps coordinate investments with long-term transfer plans |

Advisory may not be needed immediately when goals are simple, the portfolio is easy to monitor, and the investor understands costs and allocation. The right level of support should match the complexity of the decision.

For investors planning life after active income, our guide to a retirement investment plan in India explains how future income needs can affect investment choices.

Why Choose Ckredence Wealth for Financial Advisory Services in India?

At Ckredence Wealth, financial advisory begins with the investor’s full financial situation rather than a single product. We discuss goals, liquidity needs, risk capacity, current holdings, and the role each investment should play.

Our discussions focus on:

Asset allocation before product selection.

Mutual funds, PMS, equity, debt, liquidity, and family wealth decisions in one view.

Portfolio reviews when income, family commitments, business responsibilities, or goals change.

Clearer understanding of what each holding adds to the portfolio.

For investors who are deciding between broader wealth planning and focused investment management, our guide to wealth management versus portfolio management explains the difference.

Before your next investment becomes another line in a scattered portfolio, give it a role. Bring your current holdings, financial goals, and upcoming commitments. Leave with a clearer view of what each investment should do and what needs review. |

Conclusion

Financial advisory services in India can cover personal wealth planning, investment advice, family wealth decisions, or corporate finance work. The right adviser should match the actual decision you need help with, rather than simply present a product or service package.

A useful financial plan begins with goals, risk, liquidity, and asset allocation. Registration, fees, service scope, and review process should be clear before money is invested or a long-term advisory relationship begins.

FAQs

01.

What are financial advisory services in India?

Financial advisory services help individuals, families, and businesses make structured financial decisions. They may cover investments, retirement, funding, valuation, or transaction support.

02.

How is a SEBI Registered Investment Adviser different from a mutual fund distributor?

A SEBI Registered Investment Adviser charges clients directly for personalised investment advice. A mutual fund distributor may receive trail commission for regular-plan transactions.

03.

What is the difference between personal and corporate financial advisory?

Personal financial advisory focuses on investments, life goals, and family wealth. Corporate financial advisory focuses on funding, valuation, mergers, restructuring, and business transactions.

04.

How should I choose a financial adviser in India?

Check regulatory identity, payment model, service scope, written documentation, and review process. Choose an adviser whose role matches your financial needs.