6 min read time

6 min read time

Wealth Management vs Portfolio Management: Key Differences Every Investor Must Know

Wealth Management vs Portfolio Management: Key Differences Every Investor Must Know

Wealth Management vs Portfolio Management: Key Differences Every Investor Must Know

Learn the real differences between wealth management and portfolio management. Find the right service for your financial goals in India.

Learn the real differences between wealth management and portfolio management. Find the right service for your financial goals in India.

Learn the real differences between wealth management and portfolio management. Find the right service for your financial goals in India.

Ckredence Wealth

Ckredence Wealth

|

India's wealth management industry is set to grow from USD 1.1 trillion in FY2024 to USD 2.3 trillion by FY2029, according to a Deloitte India report published in January 2025.

India's HNI population has already crossed 850,000 and is expected to nearly double to 1.65 million by 2027, with 20% of millionaires now under the age of 40, per Waterfield Advisors.

Yet, a large share of affluent investors still operate without understanding which financial service they actually need.

Are you building an equity portfolio but unsure if that alone is enough to protect what you have built?

Do you know the exact point where managing investments is no longer sufficient for your financial goals?

Is your current financial plan built to handle taxes, estate planning, and generational wealth transfer?

These are the real questions that matter for any serious investor in India today. The terms wealth management and portfolio management are often used as if they mean the same thing. They do not.

Choosing the wrong service at the wrong stage of your financial journey can cost you years of compounding, misaligned tax strategies, or worse, a wealth transfer plan that was never built.

This blog breaks both services down clearly, covers where they differ, and helps you pick the right fit for where you stand financially.

Key Takeaways

Portfolio management grows your investment corpus; wealth management covers your full financial life

Wealth management includes tax, estate, and retirement planning alongside investments

SEBI-registered PMS in India requires a minimum investment of ₹50 lakhs

Wealth management serves HNIs and UHNIs; portfolio management is accessible to a wider investor base

Your financial complexity, not just your corpus size, determines which service you need

What Is Portfolio Management?

Portfolio management is the professional oversight of an individual's or institution's investment assets.

It involves deciding how to split capital across asset classes, equities, mutual funds, bonds, and cash, with the goal of achieving the best possible returns for a given level of risk.

The scope is specific: it stays within the investment space and does not extend to taxes, insurance, or estate planning.

In India, Portfolio Management Services (PMS) give this a formal structure.

SEBI regulates PMS providers under the SEBI (Portfolio Managers) Regulations, 2020, with a minimum investment threshold of ₹50 lakhs per client.

A qualified fund manager makes investment decisions on behalf of the client, managing a direct equity portfolio customised to the investor's risk profile and goals.

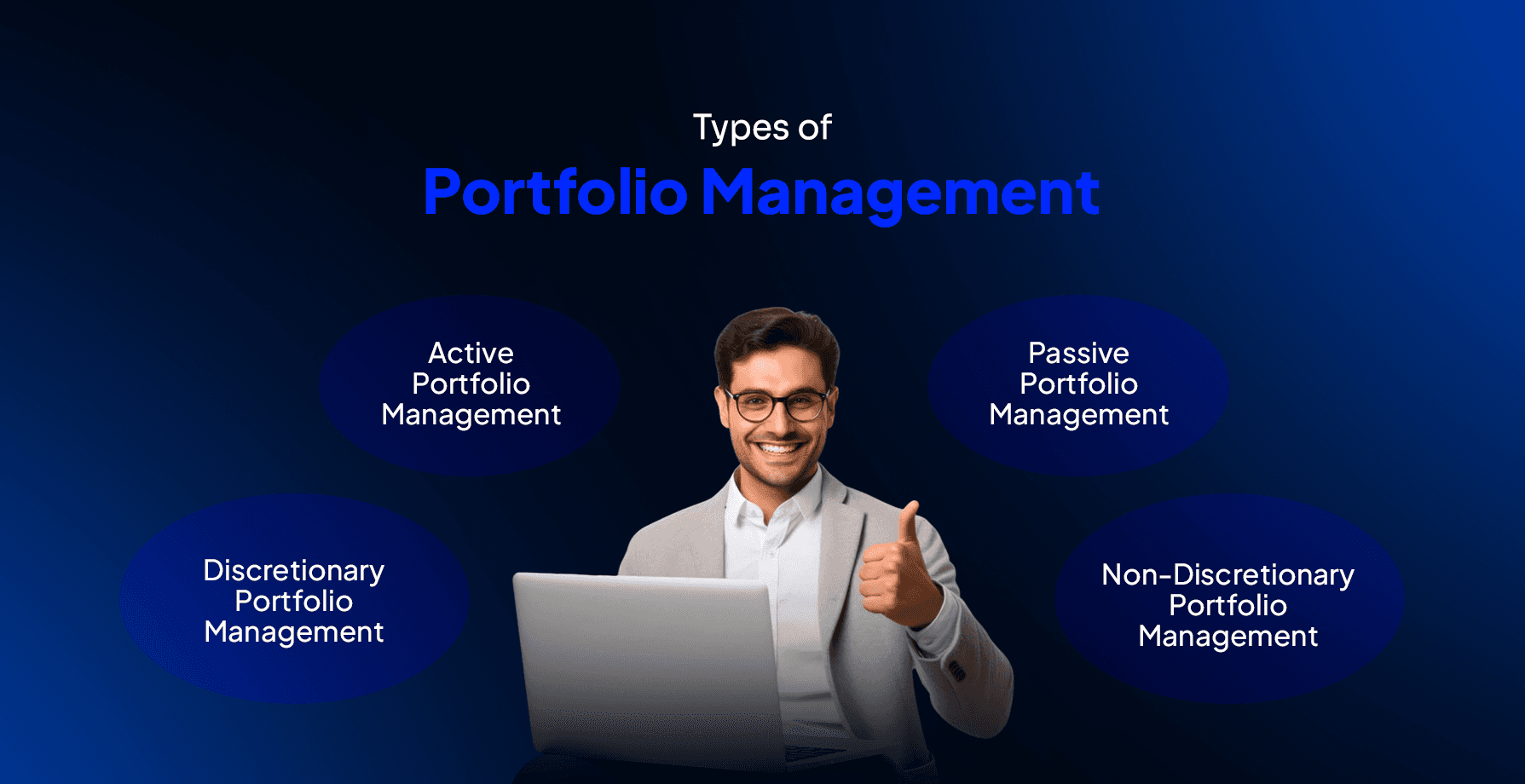

Types of Portfolio Management

There are four main types of portfolio management services in India. Knowing the difference helps you understand exactly what service you are getting:

Active Portfolio Management: The fund manager actively buys and sells securities to outperform a market benchmark like Nifty 50. This requires deep research and frequent decision-making.

Passive Portfolio Management: The goal is to match an index's performance, not beat it. It involves fewer trades and lower transaction costs.

Discretionary Portfolio Management: The manager has full authority to make buy and sell decisions without client sign-off on each trade. Most SEBI-registered PMS in India operates on this model.

Non-Discretionary Portfolio Management: The client retains decision-making authority. The manager advises, but the client approves each transaction before it is executed.

To understand exactly how these two models compare and which is better suited to your needs, read our detailed guide on discretionary vs non-discretionary PMS.

What Does a Portfolio Manager Do?

A portfolio manager handles asset selection, performance tracking, diversification, and rebalancing. Their primary job is to keep your investment mix aligned with your stated goals and risk tolerance.

If equity markets run up and your portfolio becomes overweight in stocks, a portfolio manager rebalances it back to the original allocation.

They protect and grow your investable corpus through research-backed, disciplined investment decisions.

What a portfolio manager does not do is equally important to understand. Tax filing, succession planning, estate structuring, and insurance advisory are outside their mandate. That gap is exactly where wealth management begins.

What Is Wealth Management?

Wealth management addresses a client's full financial life, not just their investments. It brings together investment advisory, tax planning, estate planning, retirement planning, insurance, and cash flow management under a single coordinated strategy.

The goal is not just to grow wealth but to protect it, organise it, and eventually transfer it across generations.

In India, wealth management is typically built for clients with investable assets above ₹50 lakhs, and becomes especially relevant for UHNIs with assets above ₹5 crores.

The service is most valuable when a client's finances involve multiple income streams, real estate holdings, business stakes, or inheritance planning, situations where managing investments alone is not enough.

Our resource on what is wealth management covers this in full detail for those looking to understand the service before making a decision.

Core Services in Wealth Management

A wealth manager works across several financial functions simultaneously:

Investment Management: Building and monitoring portfolios linked to specific long-term goals

Tax Planning: Reducing tax liability through LTCG planning, HUF structures, and indexation benefits

Estate Planning: Creating wills, trusts, and succession plans for wealth transfer to the next generation

Retirement Planning: Structuring income streams and corpus allocation for post-retirement financial security

Insurance Advisory: Identifying protection gaps and recommending the right life and health cover

Cash Flow Management: Tracking inflows, outflows, EMIs, and liquidity requirements across all assets

Who Needs Wealth Management?

Not every investor needs a wealth manager right away. If your financial life is straightforward, a salary, a few SIPs, and a term plan, portfolio management is sufficient.

Wealth management becomes the right choice when your financial picture includes business income, multiple properties, family trusts, or a need to plan for the next generation.

At that stage, your investments, taxes, and estate plans need to work together, and that calls for a professional with a much wider mandate than a portfolio manager holds.

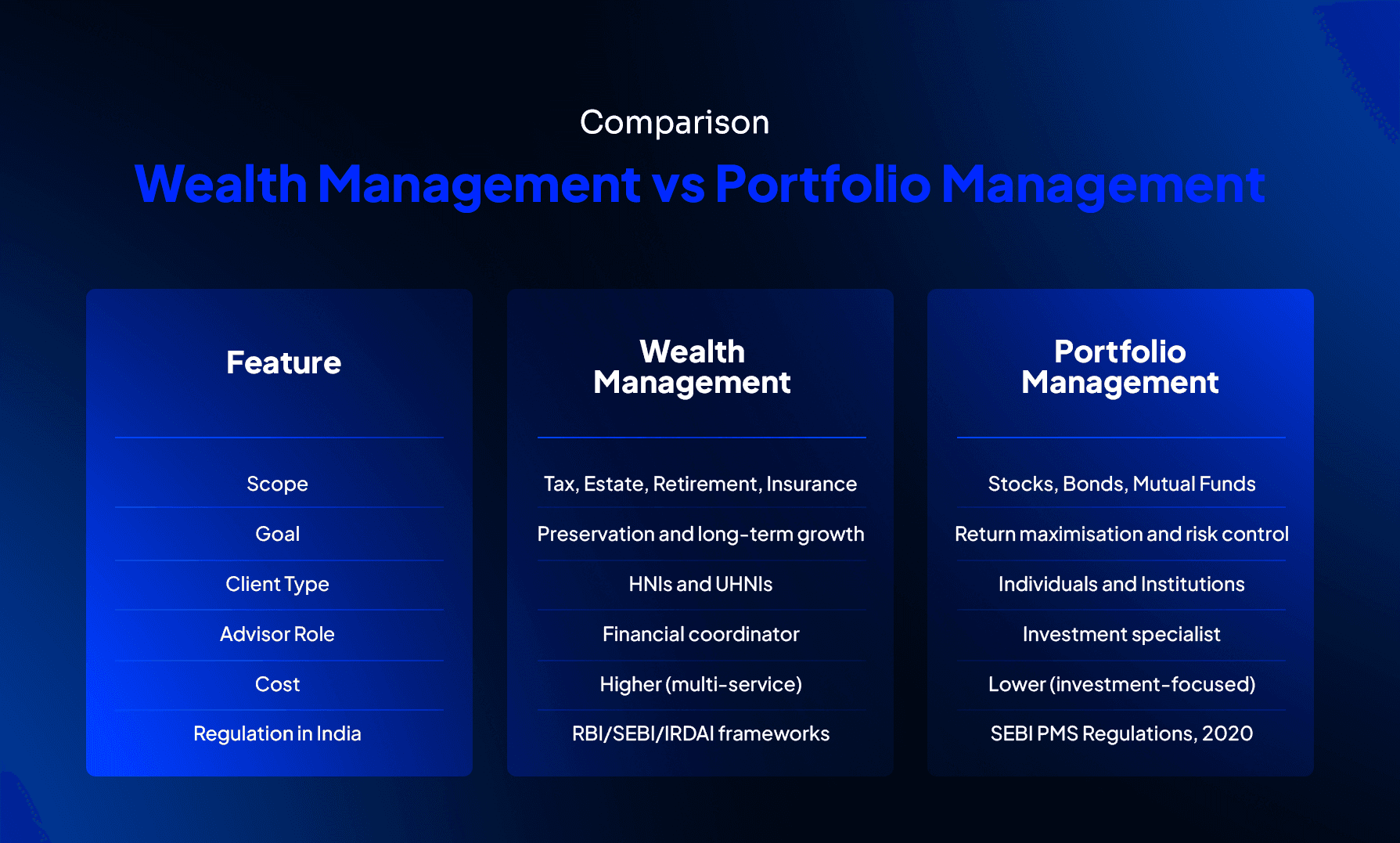

Key Differences Between Wealth Management and Portfolio Management

The wealth management vs portfolio management question ultimately comes down to one idea: scope. Portfolio management is focused and specific. Wealth management is wide-ranging and integrative.

Here is how the two compare across the most important parameters:

1. Scope of Services Portfolio management works within the investment space, covering equities, mutual funds, bonds, and ETFs. Wealth management covers the full financial picture, including tax, estate, retirement, and insurance planning.

2. Financial Goal Portfolio managers aim to grow and protect your investment corpus. Wealth managers aim to grow, protect, and pass on your entire financial wealth across time and generations.

3. Client Profile Portfolio management is accessible to individual investors and institutions with lower entry requirements. Wealth management is built for HNIs and UHNIs with layered, complex financial needs.

4. Role of the Advisor A portfolio manager is an investment specialist. A wealth manager acts as a financial coordinator, working alongside tax consultants, lawyers, and insurance advisors on your behalf.

5. Fiduciary Responsibility Wealth managers in India typically operate under a fiduciary standard, acting in the client's best interest with full transparency. Portfolio managers may operate under different contractual arrangements depending on the PMS structure chosen.

6. Cost Structure Portfolio management fees in India are typically a fixed percentage of AUM. To understand exactly what PMS costs look like in India, refer to this detailed breakdown of PMS charges and fee structures.

Wealth management costs more due to the broader range of services, and may include AUM-based charges plus flat advisory fees for services like estate structuring.

Comparison: Wealth Management vs Portfolio Management

When to Choose Portfolio Management vs Wealth Management

This is the question most investors avoid asking directly. The answer is not about how much money you have. It is about how complex your financial situation is.

Choose Portfolio Management When:

Your primary need is professional investment management. You have a clear goal, equity growth, retirement corpus, or education funding, and want an expert to manage your investments with discipline.

In India, SEBI-registered PMS is the right vehicle if you have ₹50 lakhs or more in investable surplus and want direct equity exposure managed by a qualified fund manager.

Each portfolio is built around a defined strategy that accounts for your risk profile and financial goals. Explore our four investment approaches to see how portfolios are structured for different market conditions and investor goals.

Choose Wealth Management When:

Your financial life involves more than just investments. You have business income, real estate, multiple dependents, an estate to plan, or a need to think about generational wealth transfer.

A single investment-focused service is not enough at this stage.

You need one advisor who can see your complete financial picture, your investments, tax obligations, insurance gaps, and legacy plans, and bring all of them together as one coordinated strategy.

That is what wealth management is built to do.

If managing your investments is the need, choose portfolio management. If managing your financial life is the need, choose wealth management. Many HNIs in India eventually need both, a PMS for portfolio growth and a wealth manager to coordinate everything else.

Why Should You Choose Ckredence Wealth for Portfolio Management and Wealth Advisory?

Indian investors need more than just a fund manager today. Whether your goal is equity growth, tax-efficient investing, or building a financial plan for the next generation, you need an advisor who understands both the investment landscape and the broader financial picture.

What We Bring to the Table:

Four SEBI-registered PMS strategies, All Weather, Diversified, Business Cycle, and ICE Growth, each built for different market conditions and investor goals

Wealth advisory services covering investment planning, tax efficiency, and goal-based financial structuring

₹805+ Crores in AUM managed across 376+ active clients across Gujarat and Maharashtra

37 years of experience managing wealth for HNIs, UHNIs, business owners, and family offices

Why Investors Stay With Us:

Transparent fee structures, fixed and performance-linked, with no hidden charges

Dedicated relationship managers providing regular portfolio updates and investment reviews

Branch presence in Surat, Mumbai, and Vadodara for personal, relationship-based advisory

At Ckredence Wealth, we work with investors who are serious about protecting and growing what they have built. Our approach combines professional portfolio management with personalised wealth advisory, giving you the best of both under one roof.

Ready to build the right financial plan? Schedule a Consultation with our team today.

Conclusion

The choice between wealth management and portfolio management directly shapes how well your money works for you over the years ahead. Portfolio management brings investment discipline and expert stock selection.

Wealth management brings a full financial strategy that connects your investments, taxes, estate plans, and retirement goals as one.

Portfolio management is right for investment-specific goals with a defined corpus. Wealth management is right when your financial life is complex and multi-layered. In India, SEBI-registered PMS is a strong starting point for HNIs entering professionally managed investing, and working with a SEBI-registered, experienced advisor protects you both legally and financially.

FAQs

1.

What is the main difference between wealth management and portfolio management?

Portfolio management focuses only on managing investment assets like equities and mutual funds. Wealth management covers the full financial picture, including tax, estate planning, and retirement.

2.

Who needs wealth management vs portfolio management in India?

Portfolio management suits investors with clear investment goals and a defined corpus to deploy. Wealth management is ideal for HNIs with multiple income streams or estate planning needs.

3.

Is PMS the same as wealth management in India?

No. PMS is a SEBI-regulated service focused on managing direct equity portfolios for HNIs. Wealth management is broader, covering tax, estate, insurance, and financial planning alongside investments.

4.

How do portfolio management fees compare to wealth management fees in India?

Portfolio management fees are generally lower, charged as a percentage of your assets under management. Wealth management costs more due to the wider range of services it covers.

India's wealth management industry is set to grow from USD 1.1 trillion in FY2024 to USD 2.3 trillion by FY2029, according to a Deloitte India report published in January 2025.

India's HNI population has already crossed 850,000 and is expected to nearly double to 1.65 million by 2027, with 20% of millionaires now under the age of 40, per Waterfield Advisors.

Yet, a large share of affluent investors still operate without understanding which financial service they actually need.

Are you building an equity portfolio but unsure if that alone is enough to protect what you have built?

Do you know the exact point where managing investments is no longer sufficient for your financial goals?

Is your current financial plan built to handle taxes, estate planning, and generational wealth transfer?

These are the real questions that matter for any serious investor in India today. The terms wealth management and portfolio management are often used as if they mean the same thing. They do not.

Choosing the wrong service at the wrong stage of your financial journey can cost you years of compounding, misaligned tax strategies, or worse, a wealth transfer plan that was never built.

This blog breaks both services down clearly, covers where they differ, and helps you pick the right fit for where you stand financially.

Key Takeaways

Portfolio management grows your investment corpus; wealth management covers your full financial life

Wealth management includes tax, estate, and retirement planning alongside investments

SEBI-registered PMS in India requires a minimum investment of ₹50 lakhs

Wealth management serves HNIs and UHNIs; portfolio management is accessible to a wider investor base

Your financial complexity, not just your corpus size, determines which service you need

What Is Portfolio Management?

Portfolio management is the professional oversight of an individual's or institution's investment assets.

It involves deciding how to split capital across asset classes, equities, mutual funds, bonds, and cash, with the goal of achieving the best possible returns for a given level of risk.

The scope is specific: it stays within the investment space and does not extend to taxes, insurance, or estate planning.

In India, Portfolio Management Services (PMS) give this a formal structure.

SEBI regulates PMS providers under the SEBI (Portfolio Managers) Regulations, 2020, with a minimum investment threshold of ₹50 lakhs per client.

A qualified fund manager makes investment decisions on behalf of the client, managing a direct equity portfolio customised to the investor's risk profile and goals.

Types of Portfolio Management

There are four main types of portfolio management services in India. Knowing the difference helps you understand exactly what service you are getting:

Active Portfolio Management: The fund manager actively buys and sells securities to outperform a market benchmark like Nifty 50. This requires deep research and frequent decision-making.

Passive Portfolio Management: The goal is to match an index's performance, not beat it. It involves fewer trades and lower transaction costs.

Discretionary Portfolio Management: The manager has full authority to make buy and sell decisions without client sign-off on each trade. Most SEBI-registered PMS in India operates on this model.

Non-Discretionary Portfolio Management: The client retains decision-making authority. The manager advises, but the client approves each transaction before it is executed.

To understand exactly how these two models compare and which is better suited to your needs, read our detailed guide on discretionary vs non-discretionary PMS.

What Does a Portfolio Manager Do?

A portfolio manager handles asset selection, performance tracking, diversification, and rebalancing. Their primary job is to keep your investment mix aligned with your stated goals and risk tolerance.

If equity markets run up and your portfolio becomes overweight in stocks, a portfolio manager rebalances it back to the original allocation.

They protect and grow your investable corpus through research-backed, disciplined investment decisions.

What a portfolio manager does not do is equally important to understand. Tax filing, succession planning, estate structuring, and insurance advisory are outside their mandate. That gap is exactly where wealth management begins.

What Is Wealth Management?

Wealth management addresses a client's full financial life, not just their investments. It brings together investment advisory, tax planning, estate planning, retirement planning, insurance, and cash flow management under a single coordinated strategy.

The goal is not just to grow wealth but to protect it, organise it, and eventually transfer it across generations.

In India, wealth management is typically built for clients with investable assets above ₹50 lakhs, and becomes especially relevant for UHNIs with assets above ₹5 crores.

The service is most valuable when a client's finances involve multiple income streams, real estate holdings, business stakes, or inheritance planning, situations where managing investments alone is not enough.

Our resource on what is wealth management covers this in full detail for those looking to understand the service before making a decision.

Core Services in Wealth Management

A wealth manager works across several financial functions simultaneously:

Investment Management: Building and monitoring portfolios linked to specific long-term goals

Tax Planning: Reducing tax liability through LTCG planning, HUF structures, and indexation benefits

Estate Planning: Creating wills, trusts, and succession plans for wealth transfer to the next generation

Retirement Planning: Structuring income streams and corpus allocation for post-retirement financial security

Insurance Advisory: Identifying protection gaps and recommending the right life and health cover

Cash Flow Management: Tracking inflows, outflows, EMIs, and liquidity requirements across all assets

Who Needs Wealth Management?

Not every investor needs a wealth manager right away. If your financial life is straightforward, a salary, a few SIPs, and a term plan, portfolio management is sufficient.

Wealth management becomes the right choice when your financial picture includes business income, multiple properties, family trusts, or a need to plan for the next generation.

At that stage, your investments, taxes, and estate plans need to work together, and that calls for a professional with a much wider mandate than a portfolio manager holds.

Key Differences Between Wealth Management and Portfolio Management

The wealth management vs portfolio management question ultimately comes down to one idea: scope. Portfolio management is focused and specific. Wealth management is wide-ranging and integrative.

Here is how the two compare across the most important parameters:

1. Scope of Services Portfolio management works within the investment space, covering equities, mutual funds, bonds, and ETFs. Wealth management covers the full financial picture, including tax, estate, retirement, and insurance planning.

2. Financial Goal Portfolio managers aim to grow and protect your investment corpus. Wealth managers aim to grow, protect, and pass on your entire financial wealth across time and generations.

3. Client Profile Portfolio management is accessible to individual investors and institutions with lower entry requirements. Wealth management is built for HNIs and UHNIs with layered, complex financial needs.

4. Role of the Advisor A portfolio manager is an investment specialist. A wealth manager acts as a financial coordinator, working alongside tax consultants, lawyers, and insurance advisors on your behalf.

5. Fiduciary Responsibility Wealth managers in India typically operate under a fiduciary standard, acting in the client's best interest with full transparency. Portfolio managers may operate under different contractual arrangements depending on the PMS structure chosen.

6. Cost Structure Portfolio management fees in India are typically a fixed percentage of AUM. To understand exactly what PMS costs look like in India, refer to this detailed breakdown of PMS charges and fee structures.

Wealth management costs more due to the broader range of services, and may include AUM-based charges plus flat advisory fees for services like estate structuring.

Comparison: Wealth Management vs Portfolio Management

When to Choose Portfolio Management vs Wealth Management

This is the question most investors avoid asking directly. The answer is not about how much money you have. It is about how complex your financial situation is.

Choose Portfolio Management When:

Your primary need is professional investment management. You have a clear goal, equity growth, retirement corpus, or education funding, and want an expert to manage your investments with discipline.

In India, SEBI-registered PMS is the right vehicle if you have ₹50 lakhs or more in investable surplus and want direct equity exposure managed by a qualified fund manager.

Each portfolio is built around a defined strategy that accounts for your risk profile and financial goals. Explore our four investment approaches to see how portfolios are structured for different market conditions and investor goals.

Choose Wealth Management When:

Your financial life involves more than just investments. You have business income, real estate, multiple dependents, an estate to plan, or a need to think about generational wealth transfer.

A single investment-focused service is not enough at this stage.

You need one advisor who can see your complete financial picture, your investments, tax obligations, insurance gaps, and legacy plans, and bring all of them together as one coordinated strategy.

That is what wealth management is built to do.

If managing your investments is the need, choose portfolio management. If managing your financial life is the need, choose wealth management. Many HNIs in India eventually need both, a PMS for portfolio growth and a wealth manager to coordinate everything else.

Why Should You Choose Ckredence Wealth for Portfolio Management and Wealth Advisory?

Indian investors need more than just a fund manager today. Whether your goal is equity growth, tax-efficient investing, or building a financial plan for the next generation, you need an advisor who understands both the investment landscape and the broader financial picture.

What We Bring to the Table:

Four SEBI-registered PMS strategies, All Weather, Diversified, Business Cycle, and ICE Growth, each built for different market conditions and investor goals

Wealth advisory services covering investment planning, tax efficiency, and goal-based financial structuring

₹805+ Crores in AUM managed across 376+ active clients across Gujarat and Maharashtra

37 years of experience managing wealth for HNIs, UHNIs, business owners, and family offices

Why Investors Stay With Us:

Transparent fee structures, fixed and performance-linked, with no hidden charges

Dedicated relationship managers providing regular portfolio updates and investment reviews

Branch presence in Surat, Mumbai, and Vadodara for personal, relationship-based advisory

At Ckredence Wealth, we work with investors who are serious about protecting and growing what they have built. Our approach combines professional portfolio management with personalised wealth advisory, giving you the best of both under one roof.

Ready to build the right financial plan? Schedule a Consultation with our team today.

Conclusion

The choice between wealth management and portfolio management directly shapes how well your money works for you over the years ahead. Portfolio management brings investment discipline and expert stock selection.

Wealth management brings a full financial strategy that connects your investments, taxes, estate plans, and retirement goals as one.

Portfolio management is right for investment-specific goals with a defined corpus. Wealth management is right when your financial life is complex and multi-layered. In India, SEBI-registered PMS is a strong starting point for HNIs entering professionally managed investing, and working with a SEBI-registered, experienced advisor protects you both legally and financially.

FAQs

1.

What is the main difference between wealth management and portfolio management?

Portfolio management focuses only on managing investment assets like equities and mutual funds. Wealth management covers the full financial picture, including tax, estate planning, and retirement.

2.

Who needs wealth management vs portfolio management in India?

Portfolio management suits investors with clear investment goals and a defined corpus to deploy. Wealth management is ideal for HNIs with multiple income streams or estate planning needs.

3.

Is PMS the same as wealth management in India?

No. PMS is a SEBI-regulated service focused on managing direct equity portfolios for HNIs. Wealth management is broader, covering tax, estate, insurance, and financial planning alongside investments.

4.

How do portfolio management fees compare to wealth management fees in India?

Portfolio management fees are generally lower, charged as a percentage of your assets under management. Wealth management costs more due to the wider range of services it covers.