8 Min Read

8 Min Read

PMS Charges Explained: Fee Structures, Hidden Costs & What HNIs Must Know in 2026

PMS Charges Explained: Fee Structures, Hidden Costs & What HNIs Must Know in 2026

PMS Charges Explained: Fee Structures, Hidden Costs & What HNIs Must Know in 2026

Know all PMS charges in India - management fees, performance fees, exit loads, GST & how each fee model affects your returns

Know all PMS charges in India - management fees, performance fees, exit loads, GST & how each fee model affects your returns

Know all PMS charges in India - management fees, performance fees, exit loads, GST & how each fee model affects your returns

Ckredence Wealth

Ckredence Wealth

|

Portfolio Management Services (PMS) in India follow a multi-layered fee framework where the headline management fee is only part of what you actually pay. According to SEBI's disclosure norms and a PMSBazaar study of 349 PMS approaches (2023), management fees range from 0.25% to 2.5% per annum on AUM, performance fees go up to 10% to 20% of profits above the hurdle rate, and additional costs include 18% GST, Brokerage charged at actuals per SEBI norms; other operating expenses capped at 0.50% per annum of average AUM , custodian charges, and exit loads of up to 3% in year one.

Are you certain about every PMS charge being deducted before your returns are credited?

Do you know how the high-water mark principle actually works and whether it is protecting you?

Is your current PMS fee model the right fit for your investment size and return goals?

Most HNIs review gross returns but rarely evaluate net-of-fee performance. This blog breaks down every component of PMS charges in India so you can make a well-informed decision before committing your capital.

Key Takeaways

PMS charges follow three structures fixed, performance-only, and hybrid each working differently for your portfolio

The high-water mark principle protects you from paying performance fees on portfolio recovery after a loss

A hybrid fee model can align your portfolio manager's incentives more closely with your actual returns

Exit loads reduce each year under SEBI rules and are nil after three years timing your exit matters

PMS costs go beyond the management fee: GST, brokerage, custodian, and audit fees all contribute to total cost

Choosing a direct plan removes distributor commissions, directly improving your net returns

Fee negotiation is possible at higher investment sizes knowing your benchmarks gives you leverage

What Are PMS Charges?

PMS charges are the fees collected by a SEBI-registered portfolio manager for professionally managing your investment portfolio. Unlike mutual funds, where costs sit invisibly inside the NAV, PMS fees are itemised and deducted directly from your account.

The fee framework is not uniform across investors. Two clients with the same portfolio manager can pay different PMS charges based on investment size, the fee model chosen, and terms negotiated at onboarding.

This flexibility is both an advantage and a responsibility. A well-informed investor can structure a cost-efficient arrangement; one who goes in without preparation often pays more than necessary.

PMS charges broadly fall into three categories: portfolio management fees, performance-linked fees, and operational transaction costs. The next section covers how each of the three fee models works before breaking down individual cost components.

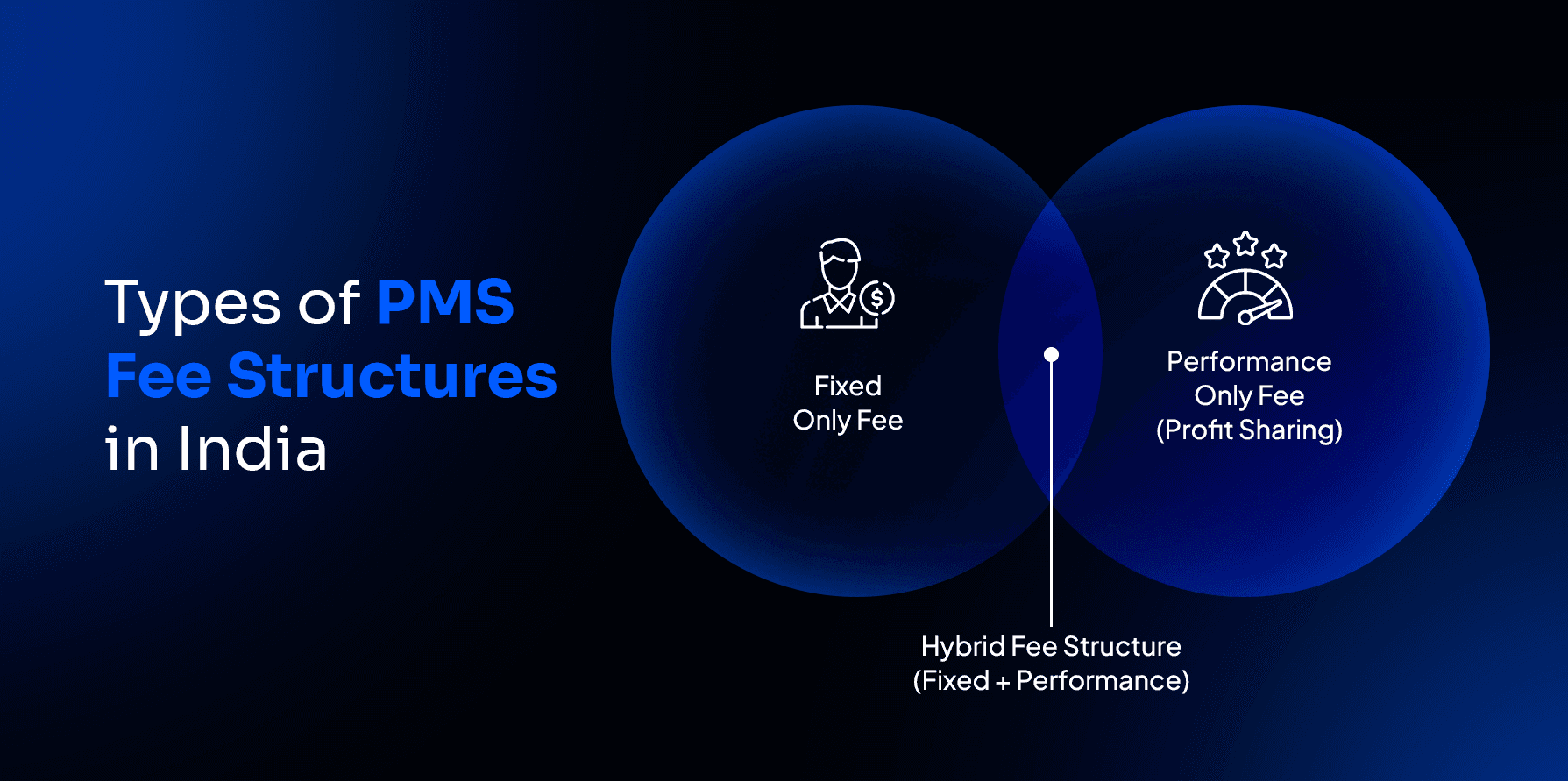

Types of PMS Fee Structures in India

SEBI-registered portfolio managers in India offer three fee models. Each carries a different cost logic and creates a different incentive structure for the fund manager.

1. Fixed-Only Fee

How it works: A fixed percentage of your average portfolio value is charged quarterly, regardless of market performance or returns delivered.

Typical range: 0.25% to 2.5% per annum on AUM

Best suited for: Investors who prefer predictable costs and are comfortable paying for professional management in all market conditions.

Key consideration: For a ₹1 crore portfolio at 2% fixed fee, you pay ₹2 lakh per year before GST whether markets are up or down. This model works in your favour during high-return years and against you in flat or negative ones.

2. Performance-Only Fee (Profit Sharing)

How it works: No fixed management fee applies. The portfolio manager earns a percentage of profits only when your portfolio exceeds a pre-agreed hurdle rate the minimum return before performance fees are triggered.

Typical structure: 10%–20% of profits above the hurdle rate, commonly set at 8%–10% per annum

Best suited for: Investors comfortable with outcome-linked costs who want zero fees in underperforming years.

Key consideration: In years of strong outperformance, total fees under this model can exceed a fixed-fee structure. It works best when you have vetted the manager's track record across multiple market cycles.

3. Hybrid Fee Structure (Fixed + Performance)

How it works: A lower fixed fee is charged quarterly and a performance fee applies only when returns cross the hurdle rate.

Typical structure: 1%–1.5% fixed fee annually +15%–20% profit sharing above the hurdle rate

Best suited for: Investors who want moderate base costs with a performance incentive for the fund manager built in.

Data from PMSBazaar's study shows that among 349 PMS approaches, 184 offer all three models and the hybrid is the most commonly selected by HNI clients. It distributes cost more evenly: you pay less in flat years and share gains in strong ones.

The fee model you select shapes how your portfolio manager approaches risk and performance. Understanding the incentive behind each model is just as important as comparing the percentages themselves.

Complete Breakdown of All PMS Charges

PMS charges extend well beyond the management or performance fee. Here is every cost component that applies to a PMS investment in India.

1. Management Fee The base recurring charge for portfolio management services, billed quarterly on average portfolio value. Ranges from 0.25% to 2.5% annually, with 18% GST applied separately on top.

2. Performance Fee Charged annually when portfolio returns exceed the hurdle rate. Typically 10%–20% of profits above the agreed threshold, governed by the high-water mark principle.

3. Entry Load A one-time charge ranging from 1% to 3% of the invested amount at the time of onboarding. More common in regular plan routes direct plan investors often avoid this charge entirely.

4. Exit Load A fee for withdrawing before a defined holding period, structured by SEBI as a reducing annual slab:

Withdrawal Timing | Maximum Exit Load |

Within Year 1 | Up to 3% |

Within Year 2 | Up to 2% |

Within Year 3 | Up to 1% |

After Year 3 | Nil |

5. Custodian Charges Your securities are held by a SEBI-registered custodian who charges annually for holding and transaction recording. The amount varies by provider and must be disclosed in your PMS agreement.

6. Brokerage Fees Charged per trade at actuals rates vary by provider, typically ranging from 0.1% to 0.5% per cash market transaction. In actively managed portfolios with high turnover, cumulative brokerage becomes a meaningful annual cost.

7. Audit Fees SEBI mandates annual auditing of PMS accounts. These fees are passed through to the investor and listed in the client agreement.

8. GST on Management Fees 18% GST is levied separately on the management fee. On a 2% annual fee for a ₹1 crore portfolio, GST alone adds ₹36,000 per year a number most investors fail to factor into return projections.

All charges must appear in the PMS Disclosure Document before onboarding. SEBI also mandates quarterly fee statements so you can track every deduction in real time.

Ready to review your PMS fee structure? Schedule a Consultation today.

How the High-Water Mark Principle Works

The high-water mark is a SEBI-mandated protection ensuring you never pay performance fees on portfolio recovery only on genuine new gains beyond your portfolio's previous peak value.

This protects you from paying fees twice on the same rupee of profit. The high-water mark resets only upward never downward.

The hurdle rate and high-water mark work as a dual safeguard. Even after crossing the previous peak, performance fees apply only on returns above the hurdle rate on that new base. Always confirm both are clearly documented in your PMS client agreement before signing.

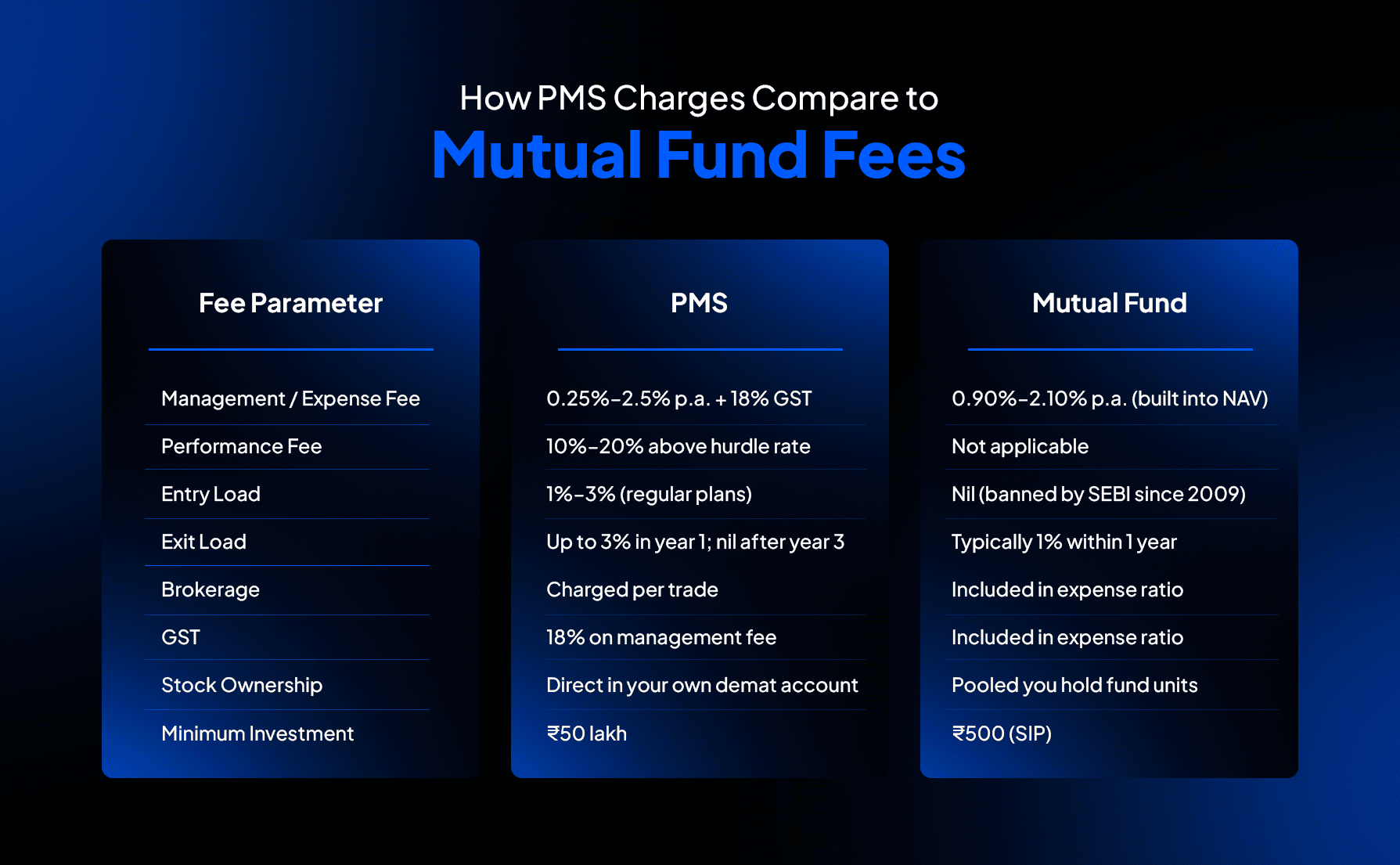

How PMS Charges Compare to Mutual Fund Fees

HNIs moving from mutual funds to PMS often underestimate the total cost difference. The two structures are built on completely different fee logics.

PMS total costs are higher, and this is widely accepted because PMS delivers direct stock ownership and personalised portfolio construction that mutual funds cannot replicate. The value case holds only when the manager consistently generates net-of-fee returns that outpace what mutual funds can deliver.

How PMS Charges Impact Your Net Returns

The real measure of PMS charges is not the percentage, it’s the corpus you receive after all deductions. Fee structures interact with compounding in ways that are not obvious until you look at a 7-10 year horizon.

A Practical Comparison

Consider two investors, both starting with ₹1 crore at a gross return of 15% per annum over 10 years.

Investor A - 2% fixed fee annually (+ 18% GST, effective ~2.36%) Investor B - 1% fixed fee + 15% performance share above a 10% hurdle

In years of strong outperformance, Investor B may pay more in total fees. In flat or moderate years, Investor B pays significantly less than Investor A.

What This Means for HNI Investors

High-return years are most costly under performance-fee models

Flat or low-return years are most costly under fixed-fee structures

Hybrid models spread cost more evenly across different market conditions

The right fee model is not the cheapest it is the one that matches the manager's actual performance record and your return expectations. Always ask for net-of-fee CAGR data across at least 3 years before selecting any PMS fee structure.

Can You Negotiate PMS Fees?

PMS fees in India are negotiable. SEBI defines caps and disclosure requirements but does not set minimum fees, leaving room for investors to seek better terms based on their investment size and profile.

What Is Negotiable

Fixed fee percentage reduction

Lower profit-sharing rate (e.g., 15% instead of 20% above hurdle)

Waiver of entry load for large investments

Extended exit load-free holding period

What Cannot Be Changed

SEBI's exit load caps and the mandatory high-water mark principle are fixed for all SEBI-registered portfolio managers. Any manager suggesting otherwise is operating outside regulatory compliance.

Knowing standard fee benchmarks before entering a negotiation puts you in a significantly stronger position. A credible portfolio manager will always be transparent about what is adjustable and what is governed by SEBI rules.

Why Should You Choose Ckredence Wealth for PMS?

PMS charges only create value when the manager behind them has a consistent, research-backed track record. Ckredence Wealth brings 37 years of wealth management experience to every client relationship, with SEBI registration (INP000007164) and a transparent fee structure that leaves nothing undisclosed.

What Sets Ckredence Apart:

₹805.85 Crores in AUM managed across 376 active clients

Four distinct PMS strategies: All Weather, Diversified, Business Cycle, and ICE Growth

Transparent fixed and performance fee disclosures fully aligned with SEBI mandates

Quarterly fee statements with charge-level breakdowns for every client

Built for HNIs Who Demand Clarity:

Dedicated relationship managers for regular portfolio and fee reviews

Technology-enabled dashboards for real-time performance and cost visibility

Branch offices in Surat, Mumbai, and Vadodara for direct, personal client access

At Ckredence Wealth, every fee we charge is matched by clear accountability to deliver returns that justify it. Our clients receive portfolio management and a long-term partnership built on full cost transparency.

Ready to review your PMS fee structure? Schedule a Consultation today.

Conclusion

PMS charges span management fees, performance fees, GST, brokerage, custodian costs, and exit loads — together forming your true total cost of holding a professionally managed portfolio. The fee model you choose directly shapes how your portfolio manager approaches risk, returns, and accountability.

The best PMS is not the one with the lowest charges. It is the one where every rupee of cost is matched by performance, transparency, and professional accountability — and where the fee structure is built to work in your favour, not just the manager's.

FAQs

What is the total cost of investing in a PMS in India?

Total cost of investing in a PMS in India include a management fee of 0.25%–2.5% per annum, performance fees of 10%–20% above a hurdle rate, and additional costs like 18% GST, brokerage, custodian fees, and exit loads. The exact total depends on your chosen fee model and provider.

How does the high-water mark protect PMS investors?

The high-water mark principle protect PMS investors by ensuring performance fees apply only when your portfolio crosses its previous highest value. You do not pay fees on returns that simply recover earlier losses.

What is the exit load structure for PMS as per SEBI rules?

The exit load structure for PMS as per SEBI rules are SEBI allows exit loads up to 3% in year one, 2% in year two, and 1% in year three of investment. No exit load can be charged after three years, regardless of when you withdraw.

How are PMS charges different from mutual fund expense ratios? PMS charges are itemised separately management fee, GST, brokerage, and performance fee are all distinct line items. Mutual fund expense ratios bundle all costs into one NAV-adjusted figure with no performance-linked component.

Portfolio Management Services (PMS) in India follow a multi-layered fee framework where the headline management fee is only part of what you actually pay. According to SEBI's disclosure norms and a PMSBazaar study of 349 PMS approaches (2023), management fees range from 0.25% to 2.5% per annum on AUM, performance fees go up to 10% to 20% of profits above the hurdle rate, and additional costs include 18% GST, Brokerage charged at actuals per SEBI norms; other operating expenses capped at 0.50% per annum of average AUM , custodian charges, and exit loads of up to 3% in year one.

Are you certain about every PMS charge being deducted before your returns are credited?

Do you know how the high-water mark principle actually works and whether it is protecting you?

Is your current PMS fee model the right fit for your investment size and return goals?

Most HNIs review gross returns but rarely evaluate net-of-fee performance. This blog breaks down every component of PMS charges in India so you can make a well-informed decision before committing your capital.

Key Takeaways

PMS charges follow three structures fixed, performance-only, and hybrid each working differently for your portfolio

The high-water mark principle protects you from paying performance fees on portfolio recovery after a loss

A hybrid fee model can align your portfolio manager's incentives more closely with your actual returns

Exit loads reduce each year under SEBI rules and are nil after three years timing your exit matters

PMS costs go beyond the management fee: GST, brokerage, custodian, and audit fees all contribute to total cost

Choosing a direct plan removes distributor commissions, directly improving your net returns

Fee negotiation is possible at higher investment sizes knowing your benchmarks gives you leverage

What Are PMS Charges?

PMS charges are the fees collected by a SEBI-registered portfolio manager for professionally managing your investment portfolio. Unlike mutual funds, where costs sit invisibly inside the NAV, PMS fees are itemised and deducted directly from your account.

The fee framework is not uniform across investors. Two clients with the same portfolio manager can pay different PMS charges based on investment size, the fee model chosen, and terms negotiated at onboarding.

This flexibility is both an advantage and a responsibility. A well-informed investor can structure a cost-efficient arrangement; one who goes in without preparation often pays more than necessary.

PMS charges broadly fall into three categories: portfolio management fees, performance-linked fees, and operational transaction costs. The next section covers how each of the three fee models works before breaking down individual cost components.

Types of PMS Fee Structures in India

SEBI-registered portfolio managers in India offer three fee models. Each carries a different cost logic and creates a different incentive structure for the fund manager.

1. Fixed-Only Fee

How it works: A fixed percentage of your average portfolio value is charged quarterly, regardless of market performance or returns delivered.

Typical range: 0.25% to 2.5% per annum on AUM

Best suited for: Investors who prefer predictable costs and are comfortable paying for professional management in all market conditions.

Key consideration: For a ₹1 crore portfolio at 2% fixed fee, you pay ₹2 lakh per year before GST whether markets are up or down. This model works in your favour during high-return years and against you in flat or negative ones.

2. Performance-Only Fee (Profit Sharing)

How it works: No fixed management fee applies. The portfolio manager earns a percentage of profits only when your portfolio exceeds a pre-agreed hurdle rate the minimum return before performance fees are triggered.

Typical structure: 10%–20% of profits above the hurdle rate, commonly set at 8%–10% per annum

Best suited for: Investors comfortable with outcome-linked costs who want zero fees in underperforming years.

Key consideration: In years of strong outperformance, total fees under this model can exceed a fixed-fee structure. It works best when you have vetted the manager's track record across multiple market cycles.

3. Hybrid Fee Structure (Fixed + Performance)

How it works: A lower fixed fee is charged quarterly and a performance fee applies only when returns cross the hurdle rate.

Typical structure: 1%–1.5% fixed fee annually +15%–20% profit sharing above the hurdle rate

Best suited for: Investors who want moderate base costs with a performance incentive for the fund manager built in.

Data from PMSBazaar's study shows that among 349 PMS approaches, 184 offer all three models and the hybrid is the most commonly selected by HNI clients. It distributes cost more evenly: you pay less in flat years and share gains in strong ones.

The fee model you select shapes how your portfolio manager approaches risk and performance. Understanding the incentive behind each model is just as important as comparing the percentages themselves.

Complete Breakdown of All PMS Charges

PMS charges extend well beyond the management or performance fee. Here is every cost component that applies to a PMS investment in India.

1. Management Fee The base recurring charge for portfolio management services, billed quarterly on average portfolio value. Ranges from 0.25% to 2.5% annually, with 18% GST applied separately on top.

2. Performance Fee Charged annually when portfolio returns exceed the hurdle rate. Typically 10%–20% of profits above the agreed threshold, governed by the high-water mark principle.

3. Entry Load A one-time charge ranging from 1% to 3% of the invested amount at the time of onboarding. More common in regular plan routes direct plan investors often avoid this charge entirely.

4. Exit Load A fee for withdrawing before a defined holding period, structured by SEBI as a reducing annual slab:

Withdrawal Timing | Maximum Exit Load |

Within Year 1 | Up to 3% |

Within Year 2 | Up to 2% |

Within Year 3 | Up to 1% |

After Year 3 | Nil |

5. Custodian Charges Your securities are held by a SEBI-registered custodian who charges annually for holding and transaction recording. The amount varies by provider and must be disclosed in your PMS agreement.

6. Brokerage Fees Charged per trade at actuals rates vary by provider, typically ranging from 0.1% to 0.5% per cash market transaction. In actively managed portfolios with high turnover, cumulative brokerage becomes a meaningful annual cost.

7. Audit Fees SEBI mandates annual auditing of PMS accounts. These fees are passed through to the investor and listed in the client agreement.

8. GST on Management Fees 18% GST is levied separately on the management fee. On a 2% annual fee for a ₹1 crore portfolio, GST alone adds ₹36,000 per year a number most investors fail to factor into return projections.

All charges must appear in the PMS Disclosure Document before onboarding. SEBI also mandates quarterly fee statements so you can track every deduction in real time.

Ready to review your PMS fee structure? Schedule a Consultation today.

How the High-Water Mark Principle Works

The high-water mark is a SEBI-mandated protection ensuring you never pay performance fees on portfolio recovery only on genuine new gains beyond your portfolio's previous peak value.

This protects you from paying fees twice on the same rupee of profit. The high-water mark resets only upward never downward.

The hurdle rate and high-water mark work as a dual safeguard. Even after crossing the previous peak, performance fees apply only on returns above the hurdle rate on that new base. Always confirm both are clearly documented in your PMS client agreement before signing.

How PMS Charges Compare to Mutual Fund Fees

HNIs moving from mutual funds to PMS often underestimate the total cost difference. The two structures are built on completely different fee logics.

PMS total costs are higher, and this is widely accepted because PMS delivers direct stock ownership and personalised portfolio construction that mutual funds cannot replicate. The value case holds only when the manager consistently generates net-of-fee returns that outpace what mutual funds can deliver.

How PMS Charges Impact Your Net Returns

The real measure of PMS charges is not the percentage, it’s the corpus you receive after all deductions. Fee structures interact with compounding in ways that are not obvious until you look at a 7-10 year horizon.

A Practical Comparison

Consider two investors, both starting with ₹1 crore at a gross return of 15% per annum over 10 years.

Investor A - 2% fixed fee annually (+ 18% GST, effective ~2.36%) Investor B - 1% fixed fee + 15% performance share above a 10% hurdle

In years of strong outperformance, Investor B may pay more in total fees. In flat or moderate years, Investor B pays significantly less than Investor A.

What This Means for HNI Investors

High-return years are most costly under performance-fee models

Flat or low-return years are most costly under fixed-fee structures

Hybrid models spread cost more evenly across different market conditions

The right fee model is not the cheapest it is the one that matches the manager's actual performance record and your return expectations. Always ask for net-of-fee CAGR data across at least 3 years before selecting any PMS fee structure.

Can You Negotiate PMS Fees?

PMS fees in India are negotiable. SEBI defines caps and disclosure requirements but does not set minimum fees, leaving room for investors to seek better terms based on their investment size and profile.

What Is Negotiable

Fixed fee percentage reduction

Lower profit-sharing rate (e.g., 15% instead of 20% above hurdle)

Waiver of entry load for large investments

Extended exit load-free holding period

What Cannot Be Changed

SEBI's exit load caps and the mandatory high-water mark principle are fixed for all SEBI-registered portfolio managers. Any manager suggesting otherwise is operating outside regulatory compliance.

Knowing standard fee benchmarks before entering a negotiation puts you in a significantly stronger position. A credible portfolio manager will always be transparent about what is adjustable and what is governed by SEBI rules.

Why Should You Choose Ckredence Wealth for PMS?

PMS charges only create value when the manager behind them has a consistent, research-backed track record. Ckredence Wealth brings 37 years of wealth management experience to every client relationship, with SEBI registration (INP000007164) and a transparent fee structure that leaves nothing undisclosed.

What Sets Ckredence Apart:

₹805.85 Crores in AUM managed across 376 active clients

Four distinct PMS strategies: All Weather, Diversified, Business Cycle, and ICE Growth

Transparent fixed and performance fee disclosures fully aligned with SEBI mandates

Quarterly fee statements with charge-level breakdowns for every client

Built for HNIs Who Demand Clarity:

Dedicated relationship managers for regular portfolio and fee reviews

Technology-enabled dashboards for real-time performance and cost visibility

Branch offices in Surat, Mumbai, and Vadodara for direct, personal client access

At Ckredence Wealth, every fee we charge is matched by clear accountability to deliver returns that justify it. Our clients receive portfolio management and a long-term partnership built on full cost transparency.

Ready to review your PMS fee structure? Schedule a Consultation today.

Conclusion

PMS charges span management fees, performance fees, GST, brokerage, custodian costs, and exit loads — together forming your true total cost of holding a professionally managed portfolio. The fee model you choose directly shapes how your portfolio manager approaches risk, returns, and accountability.

The best PMS is not the one with the lowest charges. It is the one where every rupee of cost is matched by performance, transparency, and professional accountability — and where the fee structure is built to work in your favour, not just the manager's.

FAQs

What is the total cost of investing in a PMS in India?

Total cost of investing in a PMS in India include a management fee of 0.25%–2.5% per annum, performance fees of 10%–20% above a hurdle rate, and additional costs like 18% GST, brokerage, custodian fees, and exit loads. The exact total depends on your chosen fee model and provider.

How does the high-water mark protect PMS investors?

The high-water mark principle protect PMS investors by ensuring performance fees apply only when your portfolio crosses its previous highest value. You do not pay fees on returns that simply recover earlier losses.

What is the exit load structure for PMS as per SEBI rules?

The exit load structure for PMS as per SEBI rules are SEBI allows exit loads up to 3% in year one, 2% in year two, and 1% in year three of investment. No exit load can be charged after three years, regardless of when you withdraw.

How are PMS charges different from mutual fund expense ratios? PMS charges are itemised separately management fee, GST, brokerage, and performance fee are all distinct line items. Mutual fund expense ratios bundle all costs into one NAV-adjusted figure with no performance-linked component.