6 min

6 min

Best Retirement Investment Plan in India: for Investors Over ₹1 Crore

Best Retirement Investment Plan in India: for Investors Over ₹1 Crore

Best Retirement Investment Plan in India: for Investors Over ₹1 Crore

Managing retirement corpus over ₹1 crore in India requires a structured mix of NPS, SCSS, PMS, and income-generating instruments. Here is the complete 2026 guide

Managing retirement corpus over ₹1 crore in India requires a structured mix of NPS, SCSS, PMS, and income-generating instruments. Here is the complete 2026 guide

Managing retirement corpus over ₹1 crore in India requires a structured mix of NPS, SCSS, PMS, and income-generating instruments. Here is the complete 2026 guide

Ckredence Wealth

Ckredence Wealth

|

Introduction

For retirement planning in India in 2026, a robust strategy typically combines government-backed safety nets with market-linked growth to counter rising medical costs and inflation.

If you have built a corpus of ₹1 crore or more, the challenge is no longer just accumulation. It is structuring that corpus to generate reliable monthly income, protect capital against inflation over 20 to 25 years, and minimise tax leakage across every withdrawal.

According to a detailed retirement income analysis by HisabKaro, a ₹1 lakh per month withdrawal depletes a ₹1 crore corpus in just 13.8 years at current FD rates, while a blended strategy combining NPS annuity, SCSS, and SWP from a balanced mutual fund can meaningfully extend the corpus life.

Inflation running at approximately 6% annually means ₹50,000 today will require ₹1.2 lakh per month in 15 years to maintain the same lifestyle.

Do you know which combination of retirement instruments best protects a ₹1 crore corpus in 2026?

Are you clear on how NPS, PPF, SCSS, and PMS fit together in a post-retirement income plan?

Have you accounted for taxation on each instrument's withdrawals and how the New Tax Regime affects your post-retirement income?

This guide builds a structured, actionable retirement investment plan specifically designed for investors with ₹1 crore or more in India in 2026.

Key Takeaways

A ₹1 crore corpus in FDs alone generates approximately ₹58,000 per month before tax, which inflation erodes within 10 to 12 years

A blended strategy across NPS, SCSS, PPF, and SWP from balanced mutual funds significantly extends corpus life and monthly income

SCSS at 8.2% and POMIS at 7.4% are the most reliable monthly income instruments for post-retirement investors in 2026

NPS annuity income is taxable at slab rate; PPF and EPF withdrawals are fully tax-free; plan withdrawals accordingly

Investors with ₹50 lakhs or more should use PMS as the growth engine, with guaranteed-income instruments anchoring stability

Core Retirement Investment Options for 2026

For retirement planning in India in 2026, a robust strategy typically involves a multi-layered approach combining government-backed safety nets, market-linked growth engines, and senior-specific income schemes.

Here is a full snapshot of the core instruments and their current returns:

Scheme | Type | Interest / Return (Est.) | Key Feature |

NPS | Market-linked | 9% to 12% | Flexibility in equity/debt mix; additional ₹50,000 tax deduction |

EPF / VPF | Fixed Income | 8.25% | Mandatory for salaried; employer matches 12% contribution |

PPF | Fixed Income | 7.1% | 100% tax-free (EEE); sovereign guarantee; 15-year tenure |

SCSS | Fixed Income | 8.2% | For age 60+; quarterly interest payouts; ₹30 lakh limit |

POMIS | Fixed Income | 7.4% | Monthly interest payout; ₹9 lakh individual / ₹15 lakh joint limit |

PMVVY | Fixed Income | ~7.4% | Government-backed annuity for age 60+; 10-year guaranteed return |

Mutual Funds (SWP) | Market-linked | Variable | High growth potential; tax-efficient systematic withdrawals |

PMS | Market-linked | Variable | Customised direct equity; best for corpus ₹50 lakh+ |

1. Foundational Government Schemes

These provide a low-risk base with high predictability and sovereign guarantees. For any investor with a retirement corpus, these form the non-negotiable foundation.

National Pension System (NPS): A voluntary, market-linked scheme allowing up to 75% equity exposure.

NPS has historically delivered average returns of 8% to 10% per annum and remains a top choice in 2026 for its low cost of 0.09% per annum and unique tax benefits.

At age 60, you can withdraw up to 60% of the corpus as a tax-free lump sum. At least 40% must be used to buy an annuity for a regular monthly pension.

The annuity income is taxable at your slab rate. NPS also offers an additional ₹50,000 deduction under Section 80CCD(1B) beyond the ₹1.5 lakh Section 80C limit under the Old Tax Regime.

Employees' Provident Fund (EPF): Mandatory for most salaried employees, offering a stable 8.25% interest rate for FY 2024-25.

It is a foundational Exempt-Exempt-Exempt (EEE) tool under the Old Tax Regime, meaning contributions, growth, and maturity are all tax-free.

For investors who have been salaried for 20+ years, EPF typically forms the largest single component of their retirement corpus.

Public Provident Fund (PPF): PPF offers 7.1% tax-free interest as of Q1 2026 with zero market risk and is highly recommended as a debt anchor in any retirement portfolio.

It is 100% tax-free with sovereign guarantee and a 15-year tenure.

For self-employed individuals and those without EPF, PPF is the primary fixed-income retirement vehicle. Deposits before April 5 each year earn interest for the full year.

2. Growth-Oriented Investments

For investors who are 10 to 15 years away from retirement or have a portion of their corpus that will not be needed for at least 7 years, these growth engines are essential to outpace inflation.

Retirement Mutual Funds (SWP Strategy): Equity-oriented mutual funds with a Systematic Withdrawal Plan (SWP) are one of the most tax-efficient post-retirement income strategies.

A corpus of ₹1 crore in a balanced mutual fund at 8% annual returns can support a ₹50,000 to ₹60,000 monthly withdrawal for 20+ years.

LTCG on equity funds held over 12 months is taxed at 12.5% above ₹1.25 lakhs, making SWP significantly more tax-efficient than FD interest income for investors in the 20-30% slab.

For guidance on how to structure mutual fund investments within a retirement plan, our mutual fund advisory services cover goal-based allocation, SWP structuring, and tax-efficient withdrawal planning tailored to your retirement income needs.

Portfolio Management Services (PMS) for Retirement Growth: For investors with ₹50 lakhs or more, SEBI-registered PMS provides actively managed direct equity portfolios that can serve as the high-growth engine in a retirement portfolio.

A typical retirement-focused PMS allocation targets long-term compounding with a conservative, quality-focused approach. PMS historically outperforms mutual funds over 5 to 10-year periods for disciplined, long-horizon HNI investors.

At Ckredence Wealth, our All Weather investment strategy is specifically designed for exactly this kind of stability-with-growth mandate.

Unit Linked Insurance Plans (ULIPs): Combine life cover with market-linked growth. Under 2026 reforms, annual premiums exceeding ₹2.5 lakh are taxed under capital gains at maturity.

Suitable for investors who need life coverage alongside retirement savings, though the lock-in period and charges must be evaluated carefully relative to direct PMS or mutual fund alternatives.

3. Post-Retirement Income Schemes (Age 60+)

Designed to replace a regular monthly salary with low-risk, predictable payouts. These instruments are the income backbone for the first 10 to 15 years of retirement.

Senior Citizen Savings Scheme (SCSS): SCSS offers an 8.2% interest rate for Q1 FY 2026-27 (April to June 2026), paid quarterly, with a maximum investment limit of ₹30 lakhs per individual.

SCSS is the highest-yielding government-backed scheme for investors aged 60 and above, offering capital safety and quarterly income.

At ₹30 lakhs invested in SCSS, you receive approximately ₹20,500 per month before tax. Interest above ₹1 lakh per year attracts TDS. Eligible investors should maximise the ₹30 lakh limit first before deploying surplus into FDs.

Pradhan Mantri Vaya Vandana Yojana (PMVVY): A government-backed annuity scheme through LIC India, providing a guaranteed approximately 7.4% return for 10 years with monthly pension payouts.

Designed specifically for investors aged 60 and above, with a maximum investment of ₹15 lakhs per senior citizen. The pension is taxable as income.

Post Office Monthly Income Scheme (POMIS): Provides steady monthly interest at 7.4% per annum for a 5-year tenure. Maximum investment is ₹9 lakhs for individuals and ₹15 lakhs for joint accounts.

POMIS is the simplest instrument for generating predictable monthly income with sovereign backing. Interest is taxable at slab rate. At ₹9 lakhs invested in POMIS, you receive approximately ₹5,550 per month.

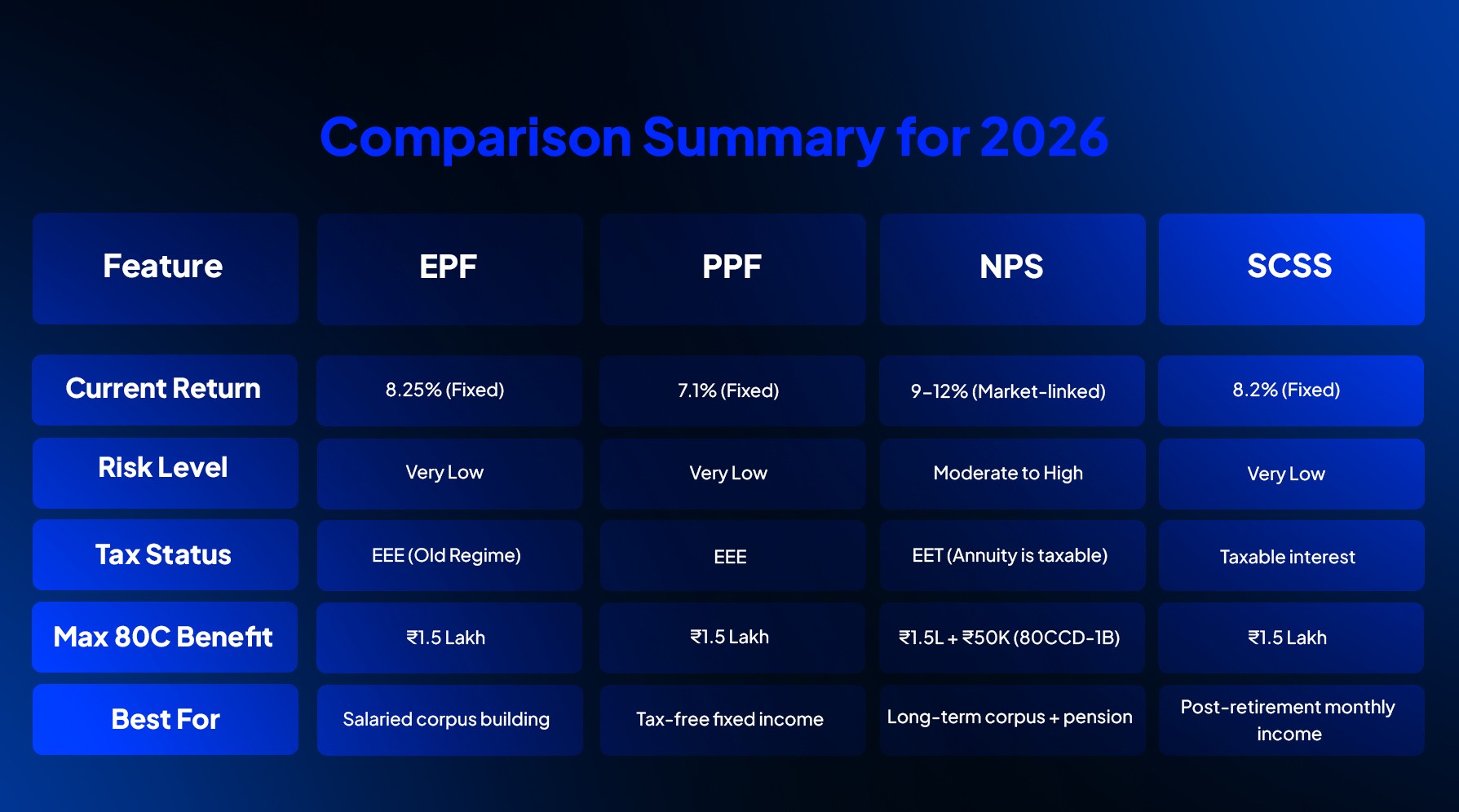

4. Comparison Summary for 2026

Note on Taxation in 2026: The New Tax Regime is now the default. Under this regime, only employer NPS contributions under Section 80CCD(2) remain deductible. Section 80C deductions for PPF, SCSS, and ELSS are available only under the Old Tax Regime. Investors must evaluate which regime offers lower effective tax before making retirement investment decisions.

Step-by-Step Retirement Planning Guide for ₹1 Crore+

Step 1 — Assess Your Required Corpus

Estimate your monthly post-retirement expenses, factoring in an annual inflation rate of approximately 6%. ₹50,000 monthly today will require approximately ₹1.2 lakh per month in 15 years.

Use the 25x rule: your required retirement corpus equals your annual post-retirement expenses multiplied by 25. For ₹1 lakh per month in today's money, with 6% inflation over 20 years, the required corpus is approximately ₹4 crore to ₹5 crore.

Step 2 — Maximise Tax Efficiency

Use Section 80C (₹1.5 lakh) via EPF, PPF, or ELSS under the Old Tax Regime if your total deductions make it beneficial

Use Section 80CCD(1B) for an additional ₹50,000 deduction exclusively for NPS under the Old Regime

Under the New Tax Regime, employer NPS contributions up to 14% of salary remain deductible under 80CCD(2), making employer NPS the most powerful remaining tax benefit for salaried investors

For a full breakdown of how each instrument is taxed at withdrawal, our guide on taxation on mutual funds and PMS covers every relevant scenario including NPS, mutual fund SWP, and PMS capital gains.

Step 3 — Select Investment Vehicles Based on Age

20s and 30s: Focus on equity — NPS with maximum equity allocation, multi-cap and flexi-cap mutual funds via SIP — for long-term compounding

40s and 50s: Balanced approach — hybrid mutual funds, VPF top-up, and SEBI-registered PMS for direct equity management — to protect capital while maintaining growth

Post-60: Safety-first income generation — SCSS, POMIS, PMVVY for guaranteed monthly cash flow, supplemented by SWP from balanced mutual funds for inflation-adjusted income

Step 4 — Plan for Regular Income Through Annuities

At retirement (age 60), you have two annuity choices for your NPS corpus. An Immediate Annuity means investing a lump sum in an IRDAI-approved annuity plan to start receiving monthly pension immediately.

A Deferred Annuity means locking in current rates now for payouts that begin later. Current NPS annuity rates from IRDAI-approved annuity service providers range from 5.5% to 7.5% annually in 2026.

The 60% lump sum is tax-free and can be deployed in SCSS, POMIS, or a balanced mutual fund SWP for additional income.

For guidance on how equity and debt allocation should shift as you approach and enter retirement, our guide on equity vs debt mutual funds walks through every key parameter to help you decide the right allocation for each stage of your financial journey.

Sample Retirement Income Plan for ₹1 Crore Corpus

Here is how a ₹1 crore corpus can be structured for maximum monthly income and corpus longevity in 2026:

Instrument | Allocation | Monthly Income (Approx.) |

SCSS | ₹30 lakh | ₹20,500 (taxable above ₹1L/yr) |

POMIS | ₹9 lakh | ₹5,550 (taxable) |

Balanced Mutual Fund (SWP) | ₹40 lakh | ₹18,000 to ₹22,000 (tax-efficient) |

Liquid / Emergency Buffer | ₹21 lakh | Available on demand |

Total Monthly Income | ₹1 crore | ₹44,000 to ₹48,000 |

For investors with ₹2 crore or more, adding PMS as the long-term growth engine alongside this income structure allows the corpus to continue compounding while generating current income from the fixed-income portion.

Why Should You Choose Ckredence Wealth for Retirement Planning?

Building a retirement plan that works for 25+ years requires more than selecting the right products. It requires a partner who structures your entire corpus around your income needs, tax position, and risk profile, and reviews it regularly as your life changes.

What We Offer:

SEBI-registered RIA services for comprehensive retirement planning covering NPS optimisation, tax strategy, and income structuring

Four SEBI-registered PMS strategies for investors with ₹50 lakhs or more who need the growth component managed actively

₹805+ Crores in AUM managed across 376+ active clients with 37 years of wealth management experience

Dedicated relationship managers and regular portfolio reviews across all life stages

For a detailed comparison of how PMS and mutual funds fit into a retirement portfolio, read our guide on portfolio management services vs mutual funds. For how to structure equity and debt in your retirement portfolio, read our guide on equity vs debt mutual funds.

Ready to build a retirement plan that lasts? Schedule a consultation with our team.

Conclusion

A retirement investment plan for investors with ₹1 crore or more in India in 2026 cannot rely on a single instrument. It must combine guaranteed-income schemes like SCSS and POMIS for predictable monthly cash flow, market-linked instruments like NPS and equity mutual funds for long-term growth, and tax-efficient structures that minimise leakage across withdrawals over a 20 to 25-year retirement horizon.

The investors who retire comfortably in India are not those with the largest corpus at age 60. They are the ones who have structured it correctly, reviewed it regularly, and had a professional advisor helping them navigate tax changes, market cycles, and income needs at every stage of the journey.

Investments are subject to market risks. Please read all scheme-related documents carefully before investing. Past performance is not indicative of future returns.

FAQs

What is the best retirement investment plan in India for investors with ₹1 crore?

A blended strategy works best. Deploy ₹30 lakhs in SCSS (8.2% quarterly income), ₹9 lakhs in POMIS (7.4% monthly income), ₹40+ lakhs in a balanced mutual fund SWP for tax-efficient monthly withdrawals, and retain a liquid buffer. Investors with ₹50 lakhs or more should consider PMS for the long-term growth component.

How much monthly income can I generate from ₹1 crore after retirement in India?

A blended strategy across SCSS, POMIS, and balanced fund SWP can generate approximately ₹44,000 to ₹48,000 per month from a ₹1 crore corpus in 2026, while preserving a significant portion for emergencies and continued growth. Relying only on FDs at 7% to 8% generates approximately ₹58,000 before tax but depletes the corpus much faster through inflation.

Is NPS a good option for retirement planning in India in 2026?

Yes, particularly for salaried investors. NPS offers market-linked returns of 9% to 12%, an additional ₹50,000 tax deduction under Section 80CCD(1B), and a 60% tax-free lump sum at retirement. The mandatory 40% annuity is taxable at slab rate, which must be factored into post-retirement income planning.

What is the SCSS interest rate in 2026 and who is eligible?

SCSS offers 8.2% per annum as of Q1 FY 2026-27, paid quarterly, with a maximum investment of ₹30 lakhs per individual. It is available to Indian residents aged 60 and above, or aged 55 to 60 if recently retired. Interest above ₹1 lakh per year attracts TDS and is taxable at the investor's applicable income slab rate.

Introduction

For retirement planning in India in 2026, a robust strategy typically combines government-backed safety nets with market-linked growth to counter rising medical costs and inflation.

If you have built a corpus of ₹1 crore or more, the challenge is no longer just accumulation. It is structuring that corpus to generate reliable monthly income, protect capital against inflation over 20 to 25 years, and minimise tax leakage across every withdrawal.

According to a detailed retirement income analysis by HisabKaro, a ₹1 lakh per month withdrawal depletes a ₹1 crore corpus in just 13.8 years at current FD rates, while a blended strategy combining NPS annuity, SCSS, and SWP from a balanced mutual fund can meaningfully extend the corpus life.

Inflation running at approximately 6% annually means ₹50,000 today will require ₹1.2 lakh per month in 15 years to maintain the same lifestyle.

Do you know which combination of retirement instruments best protects a ₹1 crore corpus in 2026?

Are you clear on how NPS, PPF, SCSS, and PMS fit together in a post-retirement income plan?

Have you accounted for taxation on each instrument's withdrawals and how the New Tax Regime affects your post-retirement income?

This guide builds a structured, actionable retirement investment plan specifically designed for investors with ₹1 crore or more in India in 2026.

Key Takeaways

A ₹1 crore corpus in FDs alone generates approximately ₹58,000 per month before tax, which inflation erodes within 10 to 12 years

A blended strategy across NPS, SCSS, PPF, and SWP from balanced mutual funds significantly extends corpus life and monthly income

SCSS at 8.2% and POMIS at 7.4% are the most reliable monthly income instruments for post-retirement investors in 2026

NPS annuity income is taxable at slab rate; PPF and EPF withdrawals are fully tax-free; plan withdrawals accordingly

Investors with ₹50 lakhs or more should use PMS as the growth engine, with guaranteed-income instruments anchoring stability

Core Retirement Investment Options for 2026

For retirement planning in India in 2026, a robust strategy typically involves a multi-layered approach combining government-backed safety nets, market-linked growth engines, and senior-specific income schemes.

Here is a full snapshot of the core instruments and their current returns:

Scheme | Type | Interest / Return (Est.) | Key Feature |

NPS | Market-linked | 9% to 12% | Flexibility in equity/debt mix; additional ₹50,000 tax deduction |

EPF / VPF | Fixed Income | 8.25% | Mandatory for salaried; employer matches 12% contribution |

PPF | Fixed Income | 7.1% | 100% tax-free (EEE); sovereign guarantee; 15-year tenure |

SCSS | Fixed Income | 8.2% | For age 60+; quarterly interest payouts; ₹30 lakh limit |

POMIS | Fixed Income | 7.4% | Monthly interest payout; ₹9 lakh individual / ₹15 lakh joint limit |

PMVVY | Fixed Income | ~7.4% | Government-backed annuity for age 60+; 10-year guaranteed return |

Mutual Funds (SWP) | Market-linked | Variable | High growth potential; tax-efficient systematic withdrawals |

PMS | Market-linked | Variable | Customised direct equity; best for corpus ₹50 lakh+ |

1. Foundational Government Schemes

These provide a low-risk base with high predictability and sovereign guarantees. For any investor with a retirement corpus, these form the non-negotiable foundation.

National Pension System (NPS): A voluntary, market-linked scheme allowing up to 75% equity exposure.

NPS has historically delivered average returns of 8% to 10% per annum and remains a top choice in 2026 for its low cost of 0.09% per annum and unique tax benefits.

At age 60, you can withdraw up to 60% of the corpus as a tax-free lump sum. At least 40% must be used to buy an annuity for a regular monthly pension.

The annuity income is taxable at your slab rate. NPS also offers an additional ₹50,000 deduction under Section 80CCD(1B) beyond the ₹1.5 lakh Section 80C limit under the Old Tax Regime.

Employees' Provident Fund (EPF): Mandatory for most salaried employees, offering a stable 8.25% interest rate for FY 2024-25.

It is a foundational Exempt-Exempt-Exempt (EEE) tool under the Old Tax Regime, meaning contributions, growth, and maturity are all tax-free.

For investors who have been salaried for 20+ years, EPF typically forms the largest single component of their retirement corpus.

Public Provident Fund (PPF): PPF offers 7.1% tax-free interest as of Q1 2026 with zero market risk and is highly recommended as a debt anchor in any retirement portfolio.

It is 100% tax-free with sovereign guarantee and a 15-year tenure.

For self-employed individuals and those without EPF, PPF is the primary fixed-income retirement vehicle. Deposits before April 5 each year earn interest for the full year.

2. Growth-Oriented Investments

For investors who are 10 to 15 years away from retirement or have a portion of their corpus that will not be needed for at least 7 years, these growth engines are essential to outpace inflation.

Retirement Mutual Funds (SWP Strategy): Equity-oriented mutual funds with a Systematic Withdrawal Plan (SWP) are one of the most tax-efficient post-retirement income strategies.

A corpus of ₹1 crore in a balanced mutual fund at 8% annual returns can support a ₹50,000 to ₹60,000 monthly withdrawal for 20+ years.

LTCG on equity funds held over 12 months is taxed at 12.5% above ₹1.25 lakhs, making SWP significantly more tax-efficient than FD interest income for investors in the 20-30% slab.

For guidance on how to structure mutual fund investments within a retirement plan, our mutual fund advisory services cover goal-based allocation, SWP structuring, and tax-efficient withdrawal planning tailored to your retirement income needs.

Portfolio Management Services (PMS) for Retirement Growth: For investors with ₹50 lakhs or more, SEBI-registered PMS provides actively managed direct equity portfolios that can serve as the high-growth engine in a retirement portfolio.

A typical retirement-focused PMS allocation targets long-term compounding with a conservative, quality-focused approach. PMS historically outperforms mutual funds over 5 to 10-year periods for disciplined, long-horizon HNI investors.

At Ckredence Wealth, our All Weather investment strategy is specifically designed for exactly this kind of stability-with-growth mandate.

Unit Linked Insurance Plans (ULIPs): Combine life cover with market-linked growth. Under 2026 reforms, annual premiums exceeding ₹2.5 lakh are taxed under capital gains at maturity.

Suitable for investors who need life coverage alongside retirement savings, though the lock-in period and charges must be evaluated carefully relative to direct PMS or mutual fund alternatives.

3. Post-Retirement Income Schemes (Age 60+)

Designed to replace a regular monthly salary with low-risk, predictable payouts. These instruments are the income backbone for the first 10 to 15 years of retirement.

Senior Citizen Savings Scheme (SCSS): SCSS offers an 8.2% interest rate for Q1 FY 2026-27 (April to June 2026), paid quarterly, with a maximum investment limit of ₹30 lakhs per individual.

SCSS is the highest-yielding government-backed scheme for investors aged 60 and above, offering capital safety and quarterly income.

At ₹30 lakhs invested in SCSS, you receive approximately ₹20,500 per month before tax. Interest above ₹1 lakh per year attracts TDS. Eligible investors should maximise the ₹30 lakh limit first before deploying surplus into FDs.

Pradhan Mantri Vaya Vandana Yojana (PMVVY): A government-backed annuity scheme through LIC India, providing a guaranteed approximately 7.4% return for 10 years with monthly pension payouts.

Designed specifically for investors aged 60 and above, with a maximum investment of ₹15 lakhs per senior citizen. The pension is taxable as income.

Post Office Monthly Income Scheme (POMIS): Provides steady monthly interest at 7.4% per annum for a 5-year tenure. Maximum investment is ₹9 lakhs for individuals and ₹15 lakhs for joint accounts.

POMIS is the simplest instrument for generating predictable monthly income with sovereign backing. Interest is taxable at slab rate. At ₹9 lakhs invested in POMIS, you receive approximately ₹5,550 per month.

4. Comparison Summary for 2026

Note on Taxation in 2026: The New Tax Regime is now the default. Under this regime, only employer NPS contributions under Section 80CCD(2) remain deductible. Section 80C deductions for PPF, SCSS, and ELSS are available only under the Old Tax Regime. Investors must evaluate which regime offers lower effective tax before making retirement investment decisions.

Step-by-Step Retirement Planning Guide for ₹1 Crore+

Step 1 — Assess Your Required Corpus

Estimate your monthly post-retirement expenses, factoring in an annual inflation rate of approximately 6%. ₹50,000 monthly today will require approximately ₹1.2 lakh per month in 15 years.

Use the 25x rule: your required retirement corpus equals your annual post-retirement expenses multiplied by 25. For ₹1 lakh per month in today's money, with 6% inflation over 20 years, the required corpus is approximately ₹4 crore to ₹5 crore.

Step 2 — Maximise Tax Efficiency

Use Section 80C (₹1.5 lakh) via EPF, PPF, or ELSS under the Old Tax Regime if your total deductions make it beneficial

Use Section 80CCD(1B) for an additional ₹50,000 deduction exclusively for NPS under the Old Regime

Under the New Tax Regime, employer NPS contributions up to 14% of salary remain deductible under 80CCD(2), making employer NPS the most powerful remaining tax benefit for salaried investors

For a full breakdown of how each instrument is taxed at withdrawal, our guide on taxation on mutual funds and PMS covers every relevant scenario including NPS, mutual fund SWP, and PMS capital gains.

Step 3 — Select Investment Vehicles Based on Age

20s and 30s: Focus on equity — NPS with maximum equity allocation, multi-cap and flexi-cap mutual funds via SIP — for long-term compounding

40s and 50s: Balanced approach — hybrid mutual funds, VPF top-up, and SEBI-registered PMS for direct equity management — to protect capital while maintaining growth

Post-60: Safety-first income generation — SCSS, POMIS, PMVVY for guaranteed monthly cash flow, supplemented by SWP from balanced mutual funds for inflation-adjusted income

Step 4 — Plan for Regular Income Through Annuities

At retirement (age 60), you have two annuity choices for your NPS corpus. An Immediate Annuity means investing a lump sum in an IRDAI-approved annuity plan to start receiving monthly pension immediately.

A Deferred Annuity means locking in current rates now for payouts that begin later. Current NPS annuity rates from IRDAI-approved annuity service providers range from 5.5% to 7.5% annually in 2026.

The 60% lump sum is tax-free and can be deployed in SCSS, POMIS, or a balanced mutual fund SWP for additional income.

For guidance on how equity and debt allocation should shift as you approach and enter retirement, our guide on equity vs debt mutual funds walks through every key parameter to help you decide the right allocation for each stage of your financial journey.

Sample Retirement Income Plan for ₹1 Crore Corpus

Here is how a ₹1 crore corpus can be structured for maximum monthly income and corpus longevity in 2026:

Instrument | Allocation | Monthly Income (Approx.) |

SCSS | ₹30 lakh | ₹20,500 (taxable above ₹1L/yr) |

POMIS | ₹9 lakh | ₹5,550 (taxable) |

Balanced Mutual Fund (SWP) | ₹40 lakh | ₹18,000 to ₹22,000 (tax-efficient) |

Liquid / Emergency Buffer | ₹21 lakh | Available on demand |

Total Monthly Income | ₹1 crore | ₹44,000 to ₹48,000 |

For investors with ₹2 crore or more, adding PMS as the long-term growth engine alongside this income structure allows the corpus to continue compounding while generating current income from the fixed-income portion.

Why Should You Choose Ckredence Wealth for Retirement Planning?

Building a retirement plan that works for 25+ years requires more than selecting the right products. It requires a partner who structures your entire corpus around your income needs, tax position, and risk profile, and reviews it regularly as your life changes.

What We Offer:

SEBI-registered RIA services for comprehensive retirement planning covering NPS optimisation, tax strategy, and income structuring

Four SEBI-registered PMS strategies for investors with ₹50 lakhs or more who need the growth component managed actively

₹805+ Crores in AUM managed across 376+ active clients with 37 years of wealth management experience

Dedicated relationship managers and regular portfolio reviews across all life stages

For a detailed comparison of how PMS and mutual funds fit into a retirement portfolio, read our guide on portfolio management services vs mutual funds. For how to structure equity and debt in your retirement portfolio, read our guide on equity vs debt mutual funds.

Ready to build a retirement plan that lasts? Schedule a consultation with our team.

Conclusion

A retirement investment plan for investors with ₹1 crore or more in India in 2026 cannot rely on a single instrument. It must combine guaranteed-income schemes like SCSS and POMIS for predictable monthly cash flow, market-linked instruments like NPS and equity mutual funds for long-term growth, and tax-efficient structures that minimise leakage across withdrawals over a 20 to 25-year retirement horizon.

The investors who retire comfortably in India are not those with the largest corpus at age 60. They are the ones who have structured it correctly, reviewed it regularly, and had a professional advisor helping them navigate tax changes, market cycles, and income needs at every stage of the journey.

Investments are subject to market risks. Please read all scheme-related documents carefully before investing. Past performance is not indicative of future returns.

FAQs

What is the best retirement investment plan in India for investors with ₹1 crore?

A blended strategy works best. Deploy ₹30 lakhs in SCSS (8.2% quarterly income), ₹9 lakhs in POMIS (7.4% monthly income), ₹40+ lakhs in a balanced mutual fund SWP for tax-efficient monthly withdrawals, and retain a liquid buffer. Investors with ₹50 lakhs or more should consider PMS for the long-term growth component.

How much monthly income can I generate from ₹1 crore after retirement in India?

A blended strategy across SCSS, POMIS, and balanced fund SWP can generate approximately ₹44,000 to ₹48,000 per month from a ₹1 crore corpus in 2026, while preserving a significant portion for emergencies and continued growth. Relying only on FDs at 7% to 8% generates approximately ₹58,000 before tax but depletes the corpus much faster through inflation.

Is NPS a good option for retirement planning in India in 2026?

Yes, particularly for salaried investors. NPS offers market-linked returns of 9% to 12%, an additional ₹50,000 tax deduction under Section 80CCD(1B), and a 60% tax-free lump sum at retirement. The mandatory 40% annuity is taxable at slab rate, which must be factored into post-retirement income planning.

What is the SCSS interest rate in 2026 and who is eligible?

SCSS offers 8.2% per annum as of Q1 FY 2026-27, paid quarterly, with a maximum investment of ₹30 lakhs per individual. It is available to Indian residents aged 60 and above, or aged 55 to 60 if recently retired. Interest above ₹1 lakh per year attracts TDS and is taxable at the investor's applicable income slab rate.