7 min

7 min

Financial Independence in India: How to Build Wealth That Works for You

Financial Independence in India: How to Build Wealth That Works for You

Financial Independence in India: How to Build Wealth That Works for You

Learn how to achieve financial independence in India with the right savings, investments, and planning strategies backed by expert guidance.

Learn how to achieve financial independence in India with the right savings, investments, and planning strategies backed by expert guidance.

Learn how to achieve financial independence in India with the right savings, investments, and planning strategies backed by expert guidance.

Ckredence Wealth

Ckredence Wealth

|

India's mutual fund industry crossed ₹79.46 lakh crore in Assets Under Management in March 2026, yet most working professionals still live paycheck to paycheck. The FIRE movement - Financial Independence, Retire Early has gained real traction among Indian millennials.

The PGIM India Retirement Readiness Survey 2025 revealed only 37% of Indians today hold any formal retirement plan down sharply from 67% in 2023.

Is your salary growing but your financial security still feels out of reach?

Do you know exactly how much corpus you need to stop depending on active income?

Are your current investments built to survive India's 5-6% inflation over 20-30 years?

These are the core problems that separate people who build lasting wealth from those who keep postponing financial freedom. This blog breaks down what financial independence in India actually means, how to calculate your path there, which investments work, and how professional wealth management can make a real difference.

Key Takeaways

Build a corpus that covers all living expenses through passive income without a salary

Use the 30x annual expense multiplier for your FIRE number, not the global 25x

Financial independence is a number; financial freedom is a mindset you need both

Savings rate matters more than salary the gap between income and spending decides the speed

SIPs in equity mutual funds are the most accessible tool for building a FIRE corpus

ULIPs and endowment plans delay financial independence avoid mixing insurance with investment

A SEBI-registered wealth manager adds structure and tax efficiency that most self-investors miss

What Is Financial Independence in India?

Financial independence in India means reaching a point where your investments generate enough passive income to cover your entire cost of living without depending on a salary, business income, or anyone else. It is called the Crossover Point: when your assets earn more than you spend each month.

This is not just a retirement concept. For many Indian professionals, it means having the option to walk away from a job that no longer fits, take a career break, or simply stop living under financial anxiety.

The FIRE Framework

FIRE stands for Financial Independence, Retire Early. The model has three parts:

Calculate your FIRE Number - your total required corpus

Build your corpus - through disciplined saving and investing

Live off the returns - using a safe withdrawal strategy

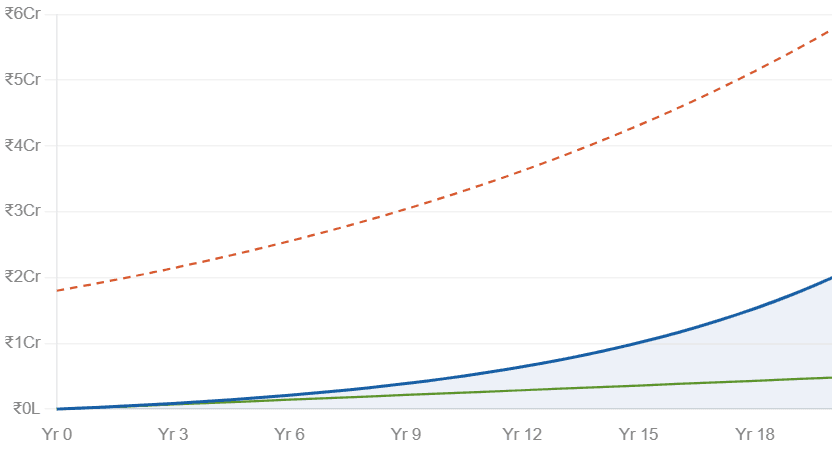

The classic global rule uses a 25x annual expense multiplier, based on the 4% safe withdrawal rate. In India, with higher inflation and longer retirement horizons, most financial planners recommend using 30–33x annual expenses as your target corpus.

Example: If your current annual expenses are ₹6 lakh, your inflation-adjusted annual expense at age 50 (assuming 6% inflation over 20 years) would be approximately ₹19.2 lakh. Your FIRE number would be ₹19.2 lakh × 30 = ₹5.76 crore.

Understanding your FIRE number is step one. Everything else savings rate, asset allocation, tax planning flows from this single target. Learn how Portfolio Management Services can help you build and manage your corpus with structure.

Monthly SIP of ₹20,000 at 12% annual return vs FIRE target (₹6L annual expenses, 6% inflation)

Financial Independence vs Financial Freedom: What Is the Difference?

These two terms get used together constantly. They are not the same thing, and mixing them up causes real planning errors.

Financial Independence is mathematical. It is the point where your investment returns cover your living expenses. You hit a number and your money works for you.

Financial Freedom is psychological. It is the shift from "Can I afford this?" to "Do I want this?" You can have ₹10 crore and still feel financially trapped if your mindset has not changed.

Many people reach their corpus target and still keep working because the anxiety does not go away. True financial independence requires both a corpus that covers your life, and a mindset that trusts the plan.

This is why a well-built financial plan is not just about numbers. It is about building a system that gives you confidence across both dimensions. Explore financial advisory services that align your plan with your goals.

Types of FIRE in India: Which One Fits You?

Not all paths to financial independence look the same. The FIRE movement has four main variants, and each suits a different income level and lifestyle goal.

Lean FIRE

Lean FIRE targets financial independence at a lower corpus by choosing a frugal, minimalist lifestyle. Monthly expenses are kept to a minimum often below ₹30,000–₹40,000. This approach reaches the FIRE number faster but leaves little room for medical emergencies or family obligations.

Fat FIRE

Fat FIRE targets a larger corpus to support a comfortable or premium lifestyle post-independence. Monthly expenses could be ₹1 lakh or more. High-income professionals doctors, senior executives, business owners typically pursue Fat FIRE.

See how investment planning services for HNIs are structured for this kind of corpus goal.

Barista FIRE

Barista FIRE means reaching a partial corpus and supplementing it with part-time or low-stress income. The investments cover most expenses. A smaller flexible income fills the gap.

Coast FIRE

Coast FIRE means investing enough early in life that compounding alone grows the corpus to your FIRE number without any further contributions. This is ideal for people in their 20s who start early and invest aggressively.

Choosing your FIRE variant is a lifestyle decision first and a financial decision second. The right type depends on your income, family responsibilities, risk tolerance, and the life you want post-independence.

Key Components of Financial Independence in India

Building a FIRE corpus in India requires getting several financial building blocks right simultaneously. Missing even one can push the timeline back significantly.

The FIRE Number

Your FIRE number is the total corpus that, when invested, generates enough returns to cover your annual expenses. In India, use the 30x multiplier as a conservative baseline. Factor in inflation, healthcare costs, and major life goals like children's education or a home purchase.

Asset Allocation

A diversified portfolio is not optional it is structural. Your corpus needs to work across market cycles. A standard long-term portfolio for a FIRE investor in India typically includes:

Equity mutual funds and ETFs - for long-term growth

Debt instruments - for stability and capital preservation

Gold - as a hedge against currency and inflation risk

Real estate - for passive rental income (where feasible)

Understand the full breakdown in this guide on equity vs debt mutual funds before deciding your split.

Systematic Investment Plans (SIPs)

SIPs in equity mutual funds are one of the most effective tools for building a FIRE corpus over 15–20 years. Consistency beats timing every time. Automating contributions removes the temptation to pause during market corrections the moments when staying invested matters most.

Emergency Fund

Before putting money into long-term investments, build a liquid emergency fund covering 6-12 months of expenses. This fund belongs in liquid mutual funds or a high-yield savings account not equities. Its job is to protect your long-term portfolio from being broken during unexpected events.

These four components work together. Miss the emergency fund and a single health event forces you to redeem long-term investments at a loss. Get all four right, and the path becomes predictable.

Why Financial Independence Is Harder in India Than in the West

Global FIRE frameworks do not translate directly to India. India has specific challenges that change the math and the plan.

No Social Security Net

The US has Social Security, Medicare, and 401(k) accounts. India has EPF and NPS, but these often fall short for a 30-40 year retirement. Most of the retirement corpus in India must come from personal savings and investments.

Medical Inflation at 10-12% Annually

One unexpected health event without independent insurance can wipe years of savings. Employer-provided health coverage ends the day you leave the job exactly when you pursue financial independence. Building a robust independent health insurance plan early is non-negotiable.

Family Financial Obligations

In India, financial independence rarely means independence from family. Supporting ageing parents, funding children's education, contributing to family weddings these are real responsibilities that Western FIRE frameworks simply ignore. Your FIRE number must account for these explicitly.

High Inflation on Essentials

A ₹100 grocery bill from 2010 crosses ₹300 today. Education costs are rising faster than general inflation. A corpus that feels large today may feel insufficient 15 years into retirement.

Currency and Market Volatility

India's equity markets can be volatile. Rupee depreciation affects the real value of returns over time. A FIRE plan built entirely on domestic equity without gold or international diversification carries concentration risk most investors underestimate.

A plan that accounts for Indian realities is far more reliable than one adapted from a US or European blog. Read how all-weather investing protects your corpus across different market conditions.

Investment Instruments for Financial Independence: What Actually Works

Prospects searching for financial independence in India want a clear answer: which instruments should I use? Here is a direct comparison based on what each instrument actually delivers.

Approximate long-term annual returns India investment instruments. India inflation: ~5-6%

Key insight: Fixed deposits earn 6.5–7.5% while India's inflation runs at 5–6%. The real return after inflation is minimal. FDs protect capital but do not build it.

Equity mutual funds and PMS are the primary engines for corpus growth over 15–20 year horizons. ULIPs and endowment plans typically deliver 4–6% returns with high charges they delay financial independence, not build it.

A structured portfolio uses equity for growth, debt for stability, gold for hedging, and professional management for strategy alignment. Explore mutual fund options and PMS strategies to find the right combination for your FIRE goal.

Steps to Achieve Financial Independence in India

The path to financial independence is not complicated. It is the consistent execution that most people miss. These steps apply whether you are starting at 25 or correcting course at 40.

Step 1: Define Your FIRE Number

Calculate your current annual expenses. Adjust for inflation at 6% over your target retirement window. Multiply by 30. Write it down as a specific rupee figure not a range.

Step 2: Track Every Rupee

Split income into three buckets: needs (50%), wants (30%), and savings/investments (20%). Over time, push the savings rate higher ideally to 40–50% for a faster FIRE timeline.

Step 3: Build the Emergency Fund

Keep 6-12 months of expenses in liquid form before investing in equity. This is the foundation on which everything else sits.

Step 4: Get Term and Health Insurance

Pure term insurance protects your family's plan if you are no longer around. Independent health insurance protects your corpus from medical emergencies. Both are essential before building a corpus.

Step 5: Clear High-Interest Debt First

Credit card debt in India carries 36-42% annual interest. No equity investment reliably beats that return. Clear all high-interest debt before building long-term wealth.

Step 6: Start SIPs in Equity Mutual Funds

Begin SIPs in diversified equity mutual funds. Automate on salary day. Increase the SIP amount by 10-15% every year as your income grows.

Step 7: Optimise Your Tax Position

Use Section 80C instruments PPF, ELSS efficiently. Understand the Old vs. New Tax Regime for your income level. Capital gains planning directly affects net returns.

Step 8: Diversify Across Asset Classes

Blend equity, debt, gold, and real estate. Avoid over-concentration in one sector or one fund house. Review portfolio management strategies to understand how professionals diversify across market cycles.

Step 9: Build Multiple Passive Income Streams

Dividend-yielding stocks, rental income, systematic withdrawal plans build income from multiple sources. Financial independence requires your money to work across channels, not just one SIP.

Step 10: Review and Rebalance Annually

Markets shift. Life changes. Review the portfolio yearly. Rebalance if equity has grown disproportionately and replace consistently underperforming funds.

Financial Independence by Life Stage: A Practical Roadmap

One of the most searched questions around financial independence India is: where should I be at my age? Here is a stage-by-stage breakdown.

Recommended portfolio allocation by life stage - financial independence India

In Your 20s: Build the Base

Your biggest asset in your 20s is time. Compounding works hardest over the longest periods. The priorities here are:

Start SIPs even ₹5,000 a month as early as possible

Build the emergency fund before investing in equity

Get term insurance while premiums are low

Avoid lifestyle inflation as income grows

Aim to save at least 20–30% of take-home salary

An equity-heavy portfolio (80–90% equity) is appropriate at this stage. Risk tolerance is high and time horizon is long.

In Your 30s: Grow and Protect

Income typically peaks in the 30s. So does lifestyle spending. The key challenge is keeping the savings rate high as expenses grow.

Increase SIP amounts with step-up SIPs of 10-15% annually

Add independent health insurance beyond employer cover

Begin tax optimisation understand capital gains and Section 80C fully

Set a specific FIRE number and track progress against it annually

This is also the decade where most financial mistakes happen ULIP purchases, underinsurance, and lifestyle-driven portfolio gaps.

In Your 40s: Accelerate and Preserve

At 40+, the horizon to financial independence is narrowing. Execution discipline matters more than strategy shifts.

Boost retirement-specific contributions NPS, PPF maximisation

Shift toward a balanced allocation reduce equity to 60–70%, increase debt

Plan for children's education and wedding costs as separate funds

Engage a SEBI-registered wealth manager for structured corpus management

The goal at this stage is not just growth it is capital preservation alongside growth.

In Your 50s and Beyond: Shift to Income

The priority changes from building the corpus to living off it.

Move to income-generating assets systematic withdrawal plans, dividend portfolios

Maximise health insurance coverage top-ups and super top-up plans

Complete estate planning will, nominee updates, asset documentation

Keep 2–3 years of expenses in liquid form to avoid selling during market downturns

Financial independence at this stage means the system is working and the plan is holding. See how a structured retirement investment plan keeps the corpus intact through this phase.

The Mindset Behind Financial Independence

Most FIRE content focuses on numbers. The part most people miss is behavioural and it is where most financial independence journeys actually break down.

Emotional Investing Is the Biggest Risk

Selling equity during a market correction, chasing last year's top-performing funds, pausing SIPs when markets look uncertain these are emotional decisions that erode corpus value over time. Financial independence is built during the boring, consistent years.

Savings Rate Over Salary

A professional earning ₹40 lakh a year and saving 15% builds wealth slower than someone earning ₹20 lakh and saving 40%. The gap between income and spending matters more than the income itself.

Patience as a Strategy

A ₹10,000 monthly SIP at 12% annual return grows to approximately ₹1 crore in 20 years. The same SIP paused for 5 years in between reaches significantly less. Consistency over 15-20 years is the actual wealth-building mechanism not stock selection or market timing.

Working With a Plan, Not Against Fear

Financial independence is not about being afraid of losing your job. It is about building a system that gives you choices. That kind of discipline is much easier to maintain with a professional guiding the process.

Common Mistakes That Delay Financial Independence

Most people in India are working hard but making avoidable errors that push their FIRE timeline back by years.

Mixing Insurance with Investment

ULIPs and endowment plans promise both coverage and returns. In practice, they deliver poor returns of 4-6% with high charges and inadequate coverage. Separate insurance from investment entirely pure term plans for protection, equity mutual funds or PMS for wealth creation.

Lifestyle Inflation

Income grows in the 30s, and so does spending. Every time salary increases, direct a portion toward increasing SIPs before upgrading lifestyle. The key is to grow investments faster than lifestyle upgrades.

Investing Without a Plan

Random investing buying funds based on last year's returns, holding underperformers out of loyalty does not build a FIRE corpus. Every rupee invested should serve a specific goal within a structured plan.

Ignoring India-Specific Risks

India's challenges medical inflation, family obligations, limited social security cannot be solved by a global FIRE template. Indian investors need a plan that addresses these local realities with specific instruments and buffers.

Starting Late and Going Aggressive to Compensate

Investors who start late often take outsized risks concentrated bets, heavy small-cap exposure to make up lost time. A higher savings rate, not higher risk, is the correct response to starting late.

Why Should You Choose Ckredence Wealth for Financial Independence?

Financial independence is a personal goal. But it requires a professional system.

Ckredence Wealth is a SEBI-registered Portfolio Management Service provider (Registration: INP000007164) with 37 years of legacy in wealth management.

With ₹805+ crore in AUM across 376 active clients, the firm has helped HNIs, business owners, senior executives, and professionals build structured, goal-aligned portfolios across market cycles.

What makes Ckredence Wealth the right partner:

Four distinct PMS strategies - All Weather, Diversified, Business Cycle, and ICE Growth each designed for specific market conditions and investor risk profiles

Risk-adjusted portfolio construction that balances capital preservation and long-term growth

Transparent fee structures fixed fees of 2.50%, 0.75%, or 0.25% based on scheme, with performance-based options aligned to client outcomes

Dedicated relationship managers for ongoing support, portfolio reviews, and investment consultations

Goal-based planning covering retirement, children's education, wealth accumulation, and legacy building

Your financial independence journey needs more than a SIP app. It needs a plan built around your FIRE number, your risk profile, your life stage, and your India-specific obligation with a team that adjusts as markets and circumstances change.

Ready to build your path to financial independence? Schedule a Consultation with Ckredence Wealth

Conclusion

Financial independence in India is achievable not just for the ultra-wealthy, but for any professional who starts with a clear FIRE number, the right asset mix, and the discipline to stay the course across life stages. The FIRE movement in India is not about escaping work; it is about building a corpus that gives you the freedom to choose how you live.

The path is clear: calculate your FIRE number, build your emergency fund, clear high-interest debt, start SIPs early, protect against India-specific risks, and rebalance annually.

What makes the difference between those who get there and those who do not is structure, consistency, and the right professional guidance and that is exactly what Ckredence Wealth brings to your journey.

01.

What is financial independence in India?

Financial independence in India means your investments generate enough passive income to cover all living expenses without a salary. It requires building a corpus of approximately 30 times your annual inflation-adjusted expenses.

02.

How much corpus do I need for financial independence in India?

The FIRE number in India uses a 30x annual expense multiplier due to 5-6% inflation. If your inflation-adjusted annual expenses at retirement are ₹12 lakh, you need approximately ₹3.6 crore as your target corpus.

03.

What is the best investment for financial independence in India?

Equity mutual funds through SIPs are the most accessible long-term wealth-building tool for financial independence in India. A diversified portfolio combining equity, debt, gold, and real estate provides both growth and capital preservation.

04.

How does a portfolio management service help with financial independence?

A SEBI-registered PMS like Ckredence Wealth builds a personalised portfolio aligned to your FIRE number and risk profile. It removes emotional decision-making and brings structured asset allocation, tax planning, and annual rebalancing to your financial independence journey.

India's mutual fund industry crossed ₹79.46 lakh crore in Assets Under Management in March 2026, yet most working professionals still live paycheck to paycheck. The FIRE movement - Financial Independence, Retire Early has gained real traction among Indian millennials.

The PGIM India Retirement Readiness Survey 2025 revealed only 37% of Indians today hold any formal retirement plan down sharply from 67% in 2023.

Is your salary growing but your financial security still feels out of reach?

Do you know exactly how much corpus you need to stop depending on active income?

Are your current investments built to survive India's 5-6% inflation over 20-30 years?

These are the core problems that separate people who build lasting wealth from those who keep postponing financial freedom. This blog breaks down what financial independence in India actually means, how to calculate your path there, which investments work, and how professional wealth management can make a real difference.

Key Takeaways

Build a corpus that covers all living expenses through passive income without a salary

Use the 30x annual expense multiplier for your FIRE number, not the global 25x

Financial independence is a number; financial freedom is a mindset you need both

Savings rate matters more than salary the gap between income and spending decides the speed

SIPs in equity mutual funds are the most accessible tool for building a FIRE corpus

ULIPs and endowment plans delay financial independence avoid mixing insurance with investment

A SEBI-registered wealth manager adds structure and tax efficiency that most self-investors miss

What Is Financial Independence in India?

Financial independence in India means reaching a point where your investments generate enough passive income to cover your entire cost of living without depending on a salary, business income, or anyone else. It is called the Crossover Point: when your assets earn more than you spend each month.

This is not just a retirement concept. For many Indian professionals, it means having the option to walk away from a job that no longer fits, take a career break, or simply stop living under financial anxiety.

The FIRE Framework

FIRE stands for Financial Independence, Retire Early. The model has three parts:

Calculate your FIRE Number - your total required corpus

Build your corpus - through disciplined saving and investing

Live off the returns - using a safe withdrawal strategy

The classic global rule uses a 25x annual expense multiplier, based on the 4% safe withdrawal rate. In India, with higher inflation and longer retirement horizons, most financial planners recommend using 30–33x annual expenses as your target corpus.

Example: If your current annual expenses are ₹6 lakh, your inflation-adjusted annual expense at age 50 (assuming 6% inflation over 20 years) would be approximately ₹19.2 lakh. Your FIRE number would be ₹19.2 lakh × 30 = ₹5.76 crore.

Understanding your FIRE number is step one. Everything else savings rate, asset allocation, tax planning flows from this single target. Learn how Portfolio Management Services can help you build and manage your corpus with structure.

Monthly SIP of ₹20,000 at 12% annual return vs FIRE target (₹6L annual expenses, 6% inflation)

Financial Independence vs Financial Freedom: What Is the Difference?

These two terms get used together constantly. They are not the same thing, and mixing them up causes real planning errors.

Financial Independence is mathematical. It is the point where your investment returns cover your living expenses. You hit a number and your money works for you.

Financial Freedom is psychological. It is the shift from "Can I afford this?" to "Do I want this?" You can have ₹10 crore and still feel financially trapped if your mindset has not changed.

Many people reach their corpus target and still keep working because the anxiety does not go away. True financial independence requires both a corpus that covers your life, and a mindset that trusts the plan.

This is why a well-built financial plan is not just about numbers. It is about building a system that gives you confidence across both dimensions. Explore financial advisory services that align your plan with your goals.

Types of FIRE in India: Which One Fits You?

Not all paths to financial independence look the same. The FIRE movement has four main variants, and each suits a different income level and lifestyle goal.

Lean FIRE

Lean FIRE targets financial independence at a lower corpus by choosing a frugal, minimalist lifestyle. Monthly expenses are kept to a minimum often below ₹30,000–₹40,000. This approach reaches the FIRE number faster but leaves little room for medical emergencies or family obligations.

Fat FIRE

Fat FIRE targets a larger corpus to support a comfortable or premium lifestyle post-independence. Monthly expenses could be ₹1 lakh or more. High-income professionals doctors, senior executives, business owners typically pursue Fat FIRE.

See how investment planning services for HNIs are structured for this kind of corpus goal.

Barista FIRE

Barista FIRE means reaching a partial corpus and supplementing it with part-time or low-stress income. The investments cover most expenses. A smaller flexible income fills the gap.

Coast FIRE

Coast FIRE means investing enough early in life that compounding alone grows the corpus to your FIRE number without any further contributions. This is ideal for people in their 20s who start early and invest aggressively.

Choosing your FIRE variant is a lifestyle decision first and a financial decision second. The right type depends on your income, family responsibilities, risk tolerance, and the life you want post-independence.

Key Components of Financial Independence in India

Building a FIRE corpus in India requires getting several financial building blocks right simultaneously. Missing even one can push the timeline back significantly.

The FIRE Number

Your FIRE number is the total corpus that, when invested, generates enough returns to cover your annual expenses. In India, use the 30x multiplier as a conservative baseline. Factor in inflation, healthcare costs, and major life goals like children's education or a home purchase.

Asset Allocation

A diversified portfolio is not optional it is structural. Your corpus needs to work across market cycles. A standard long-term portfolio for a FIRE investor in India typically includes:

Equity mutual funds and ETFs - for long-term growth

Debt instruments - for stability and capital preservation

Gold - as a hedge against currency and inflation risk

Real estate - for passive rental income (where feasible)

Understand the full breakdown in this guide on equity vs debt mutual funds before deciding your split.

Systematic Investment Plans (SIPs)

SIPs in equity mutual funds are one of the most effective tools for building a FIRE corpus over 15–20 years. Consistency beats timing every time. Automating contributions removes the temptation to pause during market corrections the moments when staying invested matters most.

Emergency Fund

Before putting money into long-term investments, build a liquid emergency fund covering 6-12 months of expenses. This fund belongs in liquid mutual funds or a high-yield savings account not equities. Its job is to protect your long-term portfolio from being broken during unexpected events.

These four components work together. Miss the emergency fund and a single health event forces you to redeem long-term investments at a loss. Get all four right, and the path becomes predictable.

Why Financial Independence Is Harder in India Than in the West

Global FIRE frameworks do not translate directly to India. India has specific challenges that change the math and the plan.

No Social Security Net

The US has Social Security, Medicare, and 401(k) accounts. India has EPF and NPS, but these often fall short for a 30-40 year retirement. Most of the retirement corpus in India must come from personal savings and investments.

Medical Inflation at 10-12% Annually

One unexpected health event without independent insurance can wipe years of savings. Employer-provided health coverage ends the day you leave the job exactly when you pursue financial independence. Building a robust independent health insurance plan early is non-negotiable.

Family Financial Obligations

In India, financial independence rarely means independence from family. Supporting ageing parents, funding children's education, contributing to family weddings these are real responsibilities that Western FIRE frameworks simply ignore. Your FIRE number must account for these explicitly.

High Inflation on Essentials

A ₹100 grocery bill from 2010 crosses ₹300 today. Education costs are rising faster than general inflation. A corpus that feels large today may feel insufficient 15 years into retirement.

Currency and Market Volatility

India's equity markets can be volatile. Rupee depreciation affects the real value of returns over time. A FIRE plan built entirely on domestic equity without gold or international diversification carries concentration risk most investors underestimate.

A plan that accounts for Indian realities is far more reliable than one adapted from a US or European blog. Read how all-weather investing protects your corpus across different market conditions.

Investment Instruments for Financial Independence: What Actually Works

Prospects searching for financial independence in India want a clear answer: which instruments should I use? Here is a direct comparison based on what each instrument actually delivers.

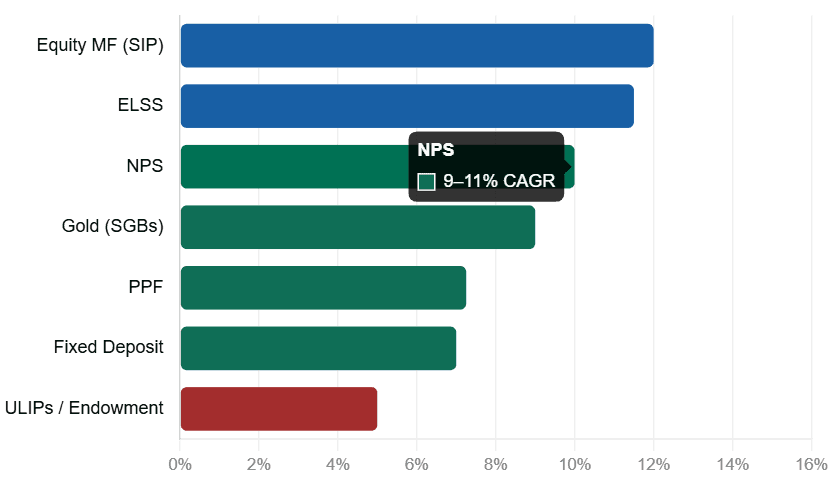

Approximate long-term annual returns India investment instruments. India inflation: ~5-6%

Key insight: Fixed deposits earn 6.5–7.5% while India's inflation runs at 5–6%. The real return after inflation is minimal. FDs protect capital but do not build it.

Equity mutual funds and PMS are the primary engines for corpus growth over 15–20 year horizons. ULIPs and endowment plans typically deliver 4–6% returns with high charges they delay financial independence, not build it.

A structured portfolio uses equity for growth, debt for stability, gold for hedging, and professional management for strategy alignment. Explore mutual fund options and PMS strategies to find the right combination for your FIRE goal.

Steps to Achieve Financial Independence in India

The path to financial independence is not complicated. It is the consistent execution that most people miss. These steps apply whether you are starting at 25 or correcting course at 40.

Step 1: Define Your FIRE Number

Calculate your current annual expenses. Adjust for inflation at 6% over your target retirement window. Multiply by 30. Write it down as a specific rupee figure not a range.

Step 2: Track Every Rupee

Split income into three buckets: needs (50%), wants (30%), and savings/investments (20%). Over time, push the savings rate higher ideally to 40–50% for a faster FIRE timeline.

Step 3: Build the Emergency Fund

Keep 6-12 months of expenses in liquid form before investing in equity. This is the foundation on which everything else sits.

Step 4: Get Term and Health Insurance

Pure term insurance protects your family's plan if you are no longer around. Independent health insurance protects your corpus from medical emergencies. Both are essential before building a corpus.

Step 5: Clear High-Interest Debt First

Credit card debt in India carries 36-42% annual interest. No equity investment reliably beats that return. Clear all high-interest debt before building long-term wealth.

Step 6: Start SIPs in Equity Mutual Funds

Begin SIPs in diversified equity mutual funds. Automate on salary day. Increase the SIP amount by 10-15% every year as your income grows.

Step 7: Optimise Your Tax Position

Use Section 80C instruments PPF, ELSS efficiently. Understand the Old vs. New Tax Regime for your income level. Capital gains planning directly affects net returns.

Step 8: Diversify Across Asset Classes

Blend equity, debt, gold, and real estate. Avoid over-concentration in one sector or one fund house. Review portfolio management strategies to understand how professionals diversify across market cycles.

Step 9: Build Multiple Passive Income Streams

Dividend-yielding stocks, rental income, systematic withdrawal plans build income from multiple sources. Financial independence requires your money to work across channels, not just one SIP.

Step 10: Review and Rebalance Annually

Markets shift. Life changes. Review the portfolio yearly. Rebalance if equity has grown disproportionately and replace consistently underperforming funds.

Financial Independence by Life Stage: A Practical Roadmap

One of the most searched questions around financial independence India is: where should I be at my age? Here is a stage-by-stage breakdown.

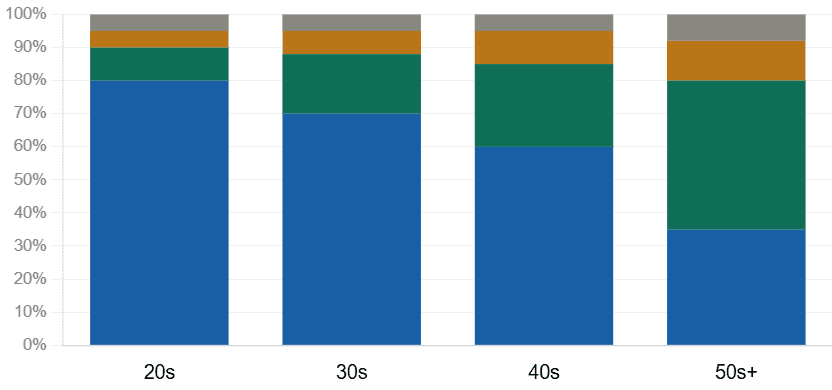

Recommended portfolio allocation by life stage - financial independence India

In Your 20s: Build the Base

Your biggest asset in your 20s is time. Compounding works hardest over the longest periods. The priorities here are:

Start SIPs even ₹5,000 a month as early as possible

Build the emergency fund before investing in equity

Get term insurance while premiums are low

Avoid lifestyle inflation as income grows

Aim to save at least 20–30% of take-home salary

An equity-heavy portfolio (80–90% equity) is appropriate at this stage. Risk tolerance is high and time horizon is long.

In Your 30s: Grow and Protect

Income typically peaks in the 30s. So does lifestyle spending. The key challenge is keeping the savings rate high as expenses grow.

Increase SIP amounts with step-up SIPs of 10-15% annually

Add independent health insurance beyond employer cover

Begin tax optimisation understand capital gains and Section 80C fully

Set a specific FIRE number and track progress against it annually

This is also the decade where most financial mistakes happen ULIP purchases, underinsurance, and lifestyle-driven portfolio gaps.

In Your 40s: Accelerate and Preserve

At 40+, the horizon to financial independence is narrowing. Execution discipline matters more than strategy shifts.

Boost retirement-specific contributions NPS, PPF maximisation

Shift toward a balanced allocation reduce equity to 60–70%, increase debt

Plan for children's education and wedding costs as separate funds

Engage a SEBI-registered wealth manager for structured corpus management

The goal at this stage is not just growth it is capital preservation alongside growth.

In Your 50s and Beyond: Shift to Income

The priority changes from building the corpus to living off it.

Move to income-generating assets systematic withdrawal plans, dividend portfolios

Maximise health insurance coverage top-ups and super top-up plans

Complete estate planning will, nominee updates, asset documentation

Keep 2–3 years of expenses in liquid form to avoid selling during market downturns

Financial independence at this stage means the system is working and the plan is holding. See how a structured retirement investment plan keeps the corpus intact through this phase.

The Mindset Behind Financial Independence

Most FIRE content focuses on numbers. The part most people miss is behavioural and it is where most financial independence journeys actually break down.

Emotional Investing Is the Biggest Risk

Selling equity during a market correction, chasing last year's top-performing funds, pausing SIPs when markets look uncertain these are emotional decisions that erode corpus value over time. Financial independence is built during the boring, consistent years.

Savings Rate Over Salary

A professional earning ₹40 lakh a year and saving 15% builds wealth slower than someone earning ₹20 lakh and saving 40%. The gap between income and spending matters more than the income itself.

Patience as a Strategy

A ₹10,000 monthly SIP at 12% annual return grows to approximately ₹1 crore in 20 years. The same SIP paused for 5 years in between reaches significantly less. Consistency over 15-20 years is the actual wealth-building mechanism not stock selection or market timing.

Working With a Plan, Not Against Fear

Financial independence is not about being afraid of losing your job. It is about building a system that gives you choices. That kind of discipline is much easier to maintain with a professional guiding the process.

Common Mistakes That Delay Financial Independence

Most people in India are working hard but making avoidable errors that push their FIRE timeline back by years.

Mixing Insurance with Investment

ULIPs and endowment plans promise both coverage and returns. In practice, they deliver poor returns of 4-6% with high charges and inadequate coverage. Separate insurance from investment entirely pure term plans for protection, equity mutual funds or PMS for wealth creation.

Lifestyle Inflation

Income grows in the 30s, and so does spending. Every time salary increases, direct a portion toward increasing SIPs before upgrading lifestyle. The key is to grow investments faster than lifestyle upgrades.

Investing Without a Plan

Random investing buying funds based on last year's returns, holding underperformers out of loyalty does not build a FIRE corpus. Every rupee invested should serve a specific goal within a structured plan.

Ignoring India-Specific Risks

India's challenges medical inflation, family obligations, limited social security cannot be solved by a global FIRE template. Indian investors need a plan that addresses these local realities with specific instruments and buffers.

Starting Late and Going Aggressive to Compensate

Investors who start late often take outsized risks concentrated bets, heavy small-cap exposure to make up lost time. A higher savings rate, not higher risk, is the correct response to starting late.

Why Should You Choose Ckredence Wealth for Financial Independence?

Financial independence is a personal goal. But it requires a professional system.

Ckredence Wealth is a SEBI-registered Portfolio Management Service provider (Registration: INP000007164) with 37 years of legacy in wealth management.

With ₹805+ crore in AUM across 376 active clients, the firm has helped HNIs, business owners, senior executives, and professionals build structured, goal-aligned portfolios across market cycles.

What makes Ckredence Wealth the right partner:

Four distinct PMS strategies - All Weather, Diversified, Business Cycle, and ICE Growth each designed for specific market conditions and investor risk profiles

Risk-adjusted portfolio construction that balances capital preservation and long-term growth

Transparent fee structures fixed fees of 2.50%, 0.75%, or 0.25% based on scheme, with performance-based options aligned to client outcomes

Dedicated relationship managers for ongoing support, portfolio reviews, and investment consultations

Goal-based planning covering retirement, children's education, wealth accumulation, and legacy building

Your financial independence journey needs more than a SIP app. It needs a plan built around your FIRE number, your risk profile, your life stage, and your India-specific obligation with a team that adjusts as markets and circumstances change.

Ready to build your path to financial independence? Schedule a Consultation with Ckredence Wealth

Conclusion

Financial independence in India is achievable not just for the ultra-wealthy, but for any professional who starts with a clear FIRE number, the right asset mix, and the discipline to stay the course across life stages. The FIRE movement in India is not about escaping work; it is about building a corpus that gives you the freedom to choose how you live.

The path is clear: calculate your FIRE number, build your emergency fund, clear high-interest debt, start SIPs early, protect against India-specific risks, and rebalance annually.

What makes the difference between those who get there and those who do not is structure, consistency, and the right professional guidance and that is exactly what Ckredence Wealth brings to your journey.

01.

What is financial independence in India?

Financial independence in India means your investments generate enough passive income to cover all living expenses without a salary. It requires building a corpus of approximately 30 times your annual inflation-adjusted expenses.

02.

How much corpus do I need for financial independence in India?

The FIRE number in India uses a 30x annual expense multiplier due to 5-6% inflation. If your inflation-adjusted annual expenses at retirement are ₹12 lakh, you need approximately ₹3.6 crore as your target corpus.

03.

What is the best investment for financial independence in India?

Equity mutual funds through SIPs are the most accessible long-term wealth-building tool for financial independence in India. A diversified portfolio combining equity, debt, gold, and real estate provides both growth and capital preservation.

04.

How does a portfolio management service help with financial independence?

A SEBI-registered PMS like Ckredence Wealth builds a personalised portfolio aligned to your FIRE number and risk profile. It removes emotional decision-making and brings structured asset allocation, tax planning, and annual rebalancing to your financial independence journey.