6 min Read

6 min Read

Financial Advisory Services India: Types, Fee Models and How to Choose the Right Advisor

Financial Advisory Services India: Types, Fee Models and How to Choose the Right Advisor

Financial Advisory Services India: Types, Fee Models and How to Choose the Right Advisor

Financial advisory services in India are regulated by SEBI to ensure transparency. Learn the types, fee models, top firms, and how to choose the right advisor for your goals.

Financial advisory services in India are regulated by SEBI to ensure transparency. Learn the types, fee models, top firms, and how to choose the right advisor for your goals.

Financial advisory services in India are regulated by SEBI to ensure transparency. Learn the types, fee models, top firms, and how to choose the right advisor for your goals.

Ckredence Wealth

Ckredence Wealth

|

Introduction

Financial advisory services in India are primarily regulated by the Securities and Exchange Board of India (SEBI), which mandates that professionals offering investment advice must be registered as Registered Investment Advisers (RIAs).

These services range from retail-focused personal wealth management to complex corporate financial advisory.

As of 2026, there are approximately 988 SEBI-registered investment advisors in India, a small number relative to the millions of investors who need guidance, according to Univest citing SEBI data. The industry is increasingly shifting toward conflict-free, fee-only models to protect investor interests.

Do you know the difference between a SEBI-registered RIA and a commission-based distributor, and why it matters for your money?

Are you clear on how much financial advisors in India actually charge, and which fee model offers the best value?

Do you know how to verify an advisor's credentials and choose the right one for your financial goals?

This guide covers everything you need to know about financial advisory services in India, including the types, fee models, top firms, and how to choose the right advisor for your situation.

Key Takeaways

Financial advisory services in India are regulated by SEBI under the Investment Advisers Regulations, 2013, with RIAs required to act in clients’ best interests

Common fee models include fee-only, AUM-based, and commission-based, with fee-only considered the most unbiased

SEBI caps fees at ₹1,25,000 per family annually or 2.5% of AUM

Always verify an advisor’s registration on the SEBI Intermediaries portal before engaging

Ckredence Wealth is a SEBI-registered RIA offering goal-based advisory across PMS, mutual funds, and equity

What Are Financial Advisory Services?

Financial advisory services refer to professional guidance provided to individuals, families, and institutions on managing their money, investments, taxes, and long-term financial goals.

A financial advisor assesses your income, liabilities, risk appetite, and financial objectives to create a personalised roadmap for wealth creation, capital preservation, and tax efficiency.

In India, the Securities and Exchange Board of India mandates that anyone providing investment advice for a fee must be registered as a Registered Investment Adviser (RIA) under SEBI (Investment Advisers) Regulations, 2013.

RIAs are legally bound by a fiduciary duty, meaning they must always act in the client's best interest, not in their own financial interest or that of any product manufacturer.

Types of Financial Advisory Services

Financial advisory services in India cover a broad spectrum of needs, from individual wealth planning to institutional investment management.

Wealth Management and Personal Finance: Tailored for individuals and families, focusing on goal-based planning for retirement, children's education, and long-term wealth creation.

This is the most common form of advisory for HNI and salaried investors in India

Investment Advisory: Providing research-based recommendations on asset classes including equities, mutual funds, and fixed-income products.

SEBI-registered RIAs and Research Analysts both operate in this space, though with different mandates and regulatory frameworks

Corporate Finance and Transaction Advisory: Services for businesses including Mergers and Acquisitions (M&A), capital restructuring, and business valuations.

Typically provided by large consulting firms and investment banks

Tax and Estate Planning: Expert guidance on minimising tax burdens through strategic investment structuring, and managing the legal transfer of wealth to beneficiaries.

Particularly relevant for HNIs and business families planning succession

Risk Management: Identifying potential financial threats to a client's portfolio or business and recommending insurance or diversification strategies to safeguard assets and income

NRI Financial Advisory: Specialised tax and FEMA compliance advisory for non-resident Indians, covering repatriation of funds, NRE and NRO account management, and investing in Indian securities under SEBI and RBI guidelines.

Our dedicated NRI desk provides end-to-end guidance for NRI investors

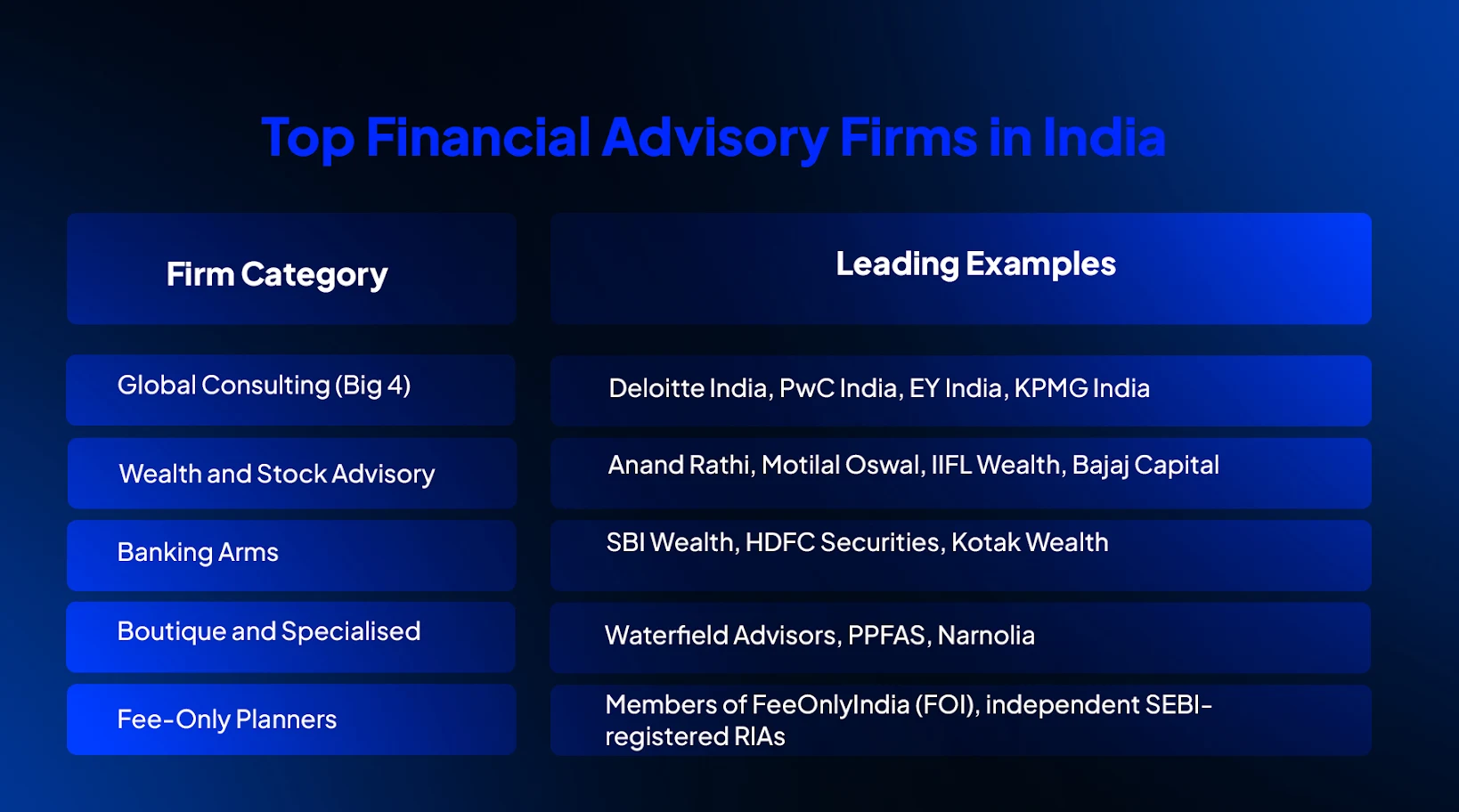

Top Financial Advisory Firms in India

Advisory firms in India range from global consultants to domestic specialists. Here is a category-wise overview of the major players:

For investors specifically looking for SEBI-registered Portfolio Management Services and RIA advisory built around direct equity and goal-based wealth planning,

Ckredence Wealth offers both services under one roof. Learn more about our investment approaches and RIA advisory services.

Fee Models for Financial Advisors in India

Understanding how a financial advisor is compensated is the single most important step before engaging one. The compensation model directly determines whether the advice you receive is in your interest or the advisor's interest.

Fee-Only Financial Advisors (Flat Fee Model)

Fee-only advisors charge a direct flat fee from the client and do not accept commissions from any financial product manufacturer.

Whether you have ₹5 lakhs or ₹5 crores to invest, the fee reflects the effort to create your financial plan, not the size of your portfolio.

In India, a comprehensive financial plan from a fee-only advisor can range from ₹15,000 to ₹50,000 per year depending on the complexity of the client's finances, according to Teji Mandi. This fee could be a one-time retainer, an hourly consultation rate of ₹2,000 to ₹5,000 per hour, or an annual subscription.

Since fee-only advisors earn nothing from product sales, their advice is unbiased. They are legally bound by a fiduciary duty to act only in your best interest.

Fee-Based or AUM-Based Financial Advisors

AUM-based advisors link their earnings to the total value of the portfolio they manage. They charge a percentage of Assets Under Management (AUM) annually.

The industry standard in India typically ranges between 1% and 2.5% of AUM per annum, according to Teji Mandi.

This model motivates the advisor to grow your wealth since their income rises when your portfolio grows. SEBI-registered PMS providers operate under this model. For our fee structure, visit our PMS charges and fee structure guide.

Commission-Based Distributors

Commission-based distributors offer "free" advice but are compensated through trail commissions paid by mutual fund houses or insurance companies for as long as you hold the product. This creates a structural conflict of interest.

The distributor may recommend products that pay higher commissions rather than what is actually best for your portfolio. It is important to distinguish between a SEBI-registered RIA, who has a legal fiduciary duty, and a distributor, who does not.

Service Types and Fee Models: A Quick Reference

Fee Model | How It Works | Typical Cost (2025-26) |

Fee-Only (Flat Fee) | Fixed fee for a comprehensive financial plan; no product commissions | ₹15,000 to ₹1,25,000 per year |

AUM-Based | Charged as a percentage of total assets under management | 1.0% to 2.5% of AUM per annum |

Commission-Based | No direct fee; advisor earns trail commissions from product manufacturers | Embedded in product cost; reduces your net returns |

Key Advisory Categories

Financial advisory services in India serve different investor profiles. Here is how the major categories break down:

Personal Financial Planning: Goal-based strategies for retirement, children's education, and tax optimisation.

Suitable for salaried professionals and self-employed individuals who need a structured financial roadmap. Ckredence Wealth's RIA services cover this category end-to-end

Wealth Management: Tailored solutions for high-net-worth individuals, including portfolio management, estate planning, and multi-asset investment strategies.

Requires a minimum corpus and deep customisation. Explore our PMS service for actively managed equity portfolios

Corporate and Institutional Advisory: Large-scale advisory for M&A transactions, valuations, capital restructuring, and regulatory compliance.

Primarily served by Big 4 firms and investment banks

NRI Advisory Services: Specialised FEMA and tax compliance advisory for non-resident Indians, covering NRE and NRO account structuring, repatriation planning, and investment in Indian equities under SEBI regulations

Key Platforms and Digital Services

The financial advisory landscape in India has expanded significantly with technology-enabled platforms that make professional advice more accessible.

Visual Idea 2: Showcase the below table in the image format

Platform Type | What It Offers | Example |

Goal-Based Planning | Advisor-led clarity on personal finances through SEBI-registered RIAs with transparent, conflict-free fee structures | 1Finance, FeeOnlyIndia |

Execution Support | Digital dashboards combined with human advisory support to help investors track, review, and rebalance portfolios without visiting a branch | Fincart, FinEdge |

Verification Tools | Confirm any advisor's registration number, validity, and regulatory standing before engaging their services | SEBI List of Registered Investment Advisers |

How to Choose the Right Financial Advisor in India

Choosing the right financial advisor is as important as choosing the right investment. The wrong advisor can cost you significantly more than their fee through poor advice, product misalignment, or conflict of interest.

Step 1. Verify SEBI Registration: Always confirm the advisor's SEBI registration number on the official SEBI Intermediaries portal.

A legitimate RIA will provide their registration number upfront and it will match SEBI records.

Step 2. Understand Their Fee Model: Ask clearly whether they are fee-only, AUM-based, or commission-based.

A fee-only or AUM-based SEBI-registered RIA has a legal fiduciary obligation. A commission-based distributor does not.

Step 3. Assess Their Process: A credible advisor starts by understanding your goals, risk profile, and time horizon before recommending any product.

If recommendations begin with products instead of understanding your financial life, that is a clear warning sign.

Step 4. Check Their Certifications: SEBI-registered RIAs must hold NISM certifications.

Additional qualifications like CFP (Certified Financial Planner) or CFA (Chartered Financial Analyst) indicate advanced technical expertise.

Step 5. Review Reporting and Transparency: Ask how often you will receive portfolio reports, how fees are disclosed, and how the advisor handles market corrections.

Transparent documentation and regular communication are the hallmarks of a credible advisory relationship.

Conclusion

Financial advisory services in India have evolved significantly under SEBI's regulatory framework, offering investors access to structured, transparent, and conflict-free professional guidance across personal planning, wealth management, and corporate advisory. The most important decision is not which advisor to choose, but which fee model and type of advisor aligns with your financial complexity and goals.

For most retail investors, a SEBI-registered fee-only or AUM-based RIA is the safest and most aligned choice. For HNIs with ₹50 lakhs or more seeking active portfolio management alongside comprehensive advisory, a combined PMS and RIA service provider like Ckredence Wealth offers the most complete solution.

Investments are subject to market risks. Please read all scheme-related documents carefully before investing. Past performance is not indicative of future returns.

FAQs

What are financial advisory services in India and who regulates them?

Financial advisory services in India include investment planning, wealth management, tax and estate planning, and corporate advisory. They are regulated by the Securities and Exchange Board of India (SEBI) under the Investment Advisers Regulations, 2013. Any professional charging a fee for investment advice must be registered as a SEBI-registered RIA.

How much do financial advisors charge in India?

Fee-only advisors charge ₹15,000 to ₹1,25,000 per year for comprehensive financial planning. AUM-based advisors charge 1% to 2.5% of the portfolio value annually. SEBI caps flat fees at ₹1,25,000 per family per year and AUM fees at 2.5% per annum to ensure fair pricing for investors.

What is the difference between a SEBI-registered RIA and a mutual fund distributor?

A SEBI-registered RIA has a legal fiduciary duty to act in your best interest and charges a direct fee. A mutual fund distributor earns commissions from product manufacturers and is not bound by the same fiduciary obligation, which can create a conflict of interest in their recommendations.

How do I verify a financial advisor's credentials in India?

You can verify any financial advisor's SEBI registration on the official SEBI Intermediaries portal at sebi.gov.in by searching their name or registration number. Confirm that their registration number, validity date, and contact details match what they have provided to you before engaging their services.

Introduction

Financial advisory services in India are primarily regulated by the Securities and Exchange Board of India (SEBI), which mandates that professionals offering investment advice must be registered as Registered Investment Advisers (RIAs).

These services range from retail-focused personal wealth management to complex corporate financial advisory.

As of 2026, there are approximately 988 SEBI-registered investment advisors in India, a small number relative to the millions of investors who need guidance, according to Univest citing SEBI data. The industry is increasingly shifting toward conflict-free, fee-only models to protect investor interests.

Do you know the difference between a SEBI-registered RIA and a commission-based distributor, and why it matters for your money?

Are you clear on how much financial advisors in India actually charge, and which fee model offers the best value?

Do you know how to verify an advisor's credentials and choose the right one for your financial goals?

This guide covers everything you need to know about financial advisory services in India, including the types, fee models, top firms, and how to choose the right advisor for your situation.

Key Takeaways

Financial advisory services in India are regulated by SEBI under the Investment Advisers Regulations, 2013, with RIAs required to act in clients’ best interests

Common fee models include fee-only, AUM-based, and commission-based, with fee-only considered the most unbiased

SEBI caps fees at ₹1,25,000 per family annually or 2.5% of AUM

Always verify an advisor’s registration on the SEBI Intermediaries portal before engaging

Ckredence Wealth is a SEBI-registered RIA offering goal-based advisory across PMS, mutual funds, and equity

What Are Financial Advisory Services?

Financial advisory services refer to professional guidance provided to individuals, families, and institutions on managing their money, investments, taxes, and long-term financial goals.

A financial advisor assesses your income, liabilities, risk appetite, and financial objectives to create a personalised roadmap for wealth creation, capital preservation, and tax efficiency.

In India, the Securities and Exchange Board of India mandates that anyone providing investment advice for a fee must be registered as a Registered Investment Adviser (RIA) under SEBI (Investment Advisers) Regulations, 2013.

RIAs are legally bound by a fiduciary duty, meaning they must always act in the client's best interest, not in their own financial interest or that of any product manufacturer.

Types of Financial Advisory Services

Financial advisory services in India cover a broad spectrum of needs, from individual wealth planning to institutional investment management.

Wealth Management and Personal Finance: Tailored for individuals and families, focusing on goal-based planning for retirement, children's education, and long-term wealth creation.

This is the most common form of advisory for HNI and salaried investors in India

Investment Advisory: Providing research-based recommendations on asset classes including equities, mutual funds, and fixed-income products.

SEBI-registered RIAs and Research Analysts both operate in this space, though with different mandates and regulatory frameworks

Corporate Finance and Transaction Advisory: Services for businesses including Mergers and Acquisitions (M&A), capital restructuring, and business valuations.

Typically provided by large consulting firms and investment banks

Tax and Estate Planning: Expert guidance on minimising tax burdens through strategic investment structuring, and managing the legal transfer of wealth to beneficiaries.

Particularly relevant for HNIs and business families planning succession

Risk Management: Identifying potential financial threats to a client's portfolio or business and recommending insurance or diversification strategies to safeguard assets and income

NRI Financial Advisory: Specialised tax and FEMA compliance advisory for non-resident Indians, covering repatriation of funds, NRE and NRO account management, and investing in Indian securities under SEBI and RBI guidelines.

Our dedicated NRI desk provides end-to-end guidance for NRI investors

Top Financial Advisory Firms in India

Advisory firms in India range from global consultants to domestic specialists. Here is a category-wise overview of the major players:

For investors specifically looking for SEBI-registered Portfolio Management Services and RIA advisory built around direct equity and goal-based wealth planning,

Ckredence Wealth offers both services under one roof. Learn more about our investment approaches and RIA advisory services.

Fee Models for Financial Advisors in India

Understanding how a financial advisor is compensated is the single most important step before engaging one. The compensation model directly determines whether the advice you receive is in your interest or the advisor's interest.

Fee-Only Financial Advisors (Flat Fee Model)

Fee-only advisors charge a direct flat fee from the client and do not accept commissions from any financial product manufacturer.

Whether you have ₹5 lakhs or ₹5 crores to invest, the fee reflects the effort to create your financial plan, not the size of your portfolio.

In India, a comprehensive financial plan from a fee-only advisor can range from ₹15,000 to ₹50,000 per year depending on the complexity of the client's finances, according to Teji Mandi. This fee could be a one-time retainer, an hourly consultation rate of ₹2,000 to ₹5,000 per hour, or an annual subscription.

Since fee-only advisors earn nothing from product sales, their advice is unbiased. They are legally bound by a fiduciary duty to act only in your best interest.

Fee-Based or AUM-Based Financial Advisors

AUM-based advisors link their earnings to the total value of the portfolio they manage. They charge a percentage of Assets Under Management (AUM) annually.

The industry standard in India typically ranges between 1% and 2.5% of AUM per annum, according to Teji Mandi.

This model motivates the advisor to grow your wealth since their income rises when your portfolio grows. SEBI-registered PMS providers operate under this model. For our fee structure, visit our PMS charges and fee structure guide.

Commission-Based Distributors

Commission-based distributors offer "free" advice but are compensated through trail commissions paid by mutual fund houses or insurance companies for as long as you hold the product. This creates a structural conflict of interest.

The distributor may recommend products that pay higher commissions rather than what is actually best for your portfolio. It is important to distinguish between a SEBI-registered RIA, who has a legal fiduciary duty, and a distributor, who does not.

Service Types and Fee Models: A Quick Reference

Fee Model | How It Works | Typical Cost (2025-26) |

Fee-Only (Flat Fee) | Fixed fee for a comprehensive financial plan; no product commissions | ₹15,000 to ₹1,25,000 per year |

AUM-Based | Charged as a percentage of total assets under management | 1.0% to 2.5% of AUM per annum |

Commission-Based | No direct fee; advisor earns trail commissions from product manufacturers | Embedded in product cost; reduces your net returns |

Key Advisory Categories

Financial advisory services in India serve different investor profiles. Here is how the major categories break down:

Personal Financial Planning: Goal-based strategies for retirement, children's education, and tax optimisation.

Suitable for salaried professionals and self-employed individuals who need a structured financial roadmap. Ckredence Wealth's RIA services cover this category end-to-end

Wealth Management: Tailored solutions for high-net-worth individuals, including portfolio management, estate planning, and multi-asset investment strategies.

Requires a minimum corpus and deep customisation. Explore our PMS service for actively managed equity portfolios

Corporate and Institutional Advisory: Large-scale advisory for M&A transactions, valuations, capital restructuring, and regulatory compliance.

Primarily served by Big 4 firms and investment banks

NRI Advisory Services: Specialised FEMA and tax compliance advisory for non-resident Indians, covering NRE and NRO account structuring, repatriation planning, and investment in Indian equities under SEBI regulations

Key Platforms and Digital Services

The financial advisory landscape in India has expanded significantly with technology-enabled platforms that make professional advice more accessible.

Visual Idea 2: Showcase the below table in the image format

Platform Type | What It Offers | Example |

Goal-Based Planning | Advisor-led clarity on personal finances through SEBI-registered RIAs with transparent, conflict-free fee structures | 1Finance, FeeOnlyIndia |

Execution Support | Digital dashboards combined with human advisory support to help investors track, review, and rebalance portfolios without visiting a branch | Fincart, FinEdge |

Verification Tools | Confirm any advisor's registration number, validity, and regulatory standing before engaging their services | SEBI List of Registered Investment Advisers |

How to Choose the Right Financial Advisor in India

Choosing the right financial advisor is as important as choosing the right investment. The wrong advisor can cost you significantly more than their fee through poor advice, product misalignment, or conflict of interest.

Step 1. Verify SEBI Registration: Always confirm the advisor's SEBI registration number on the official SEBI Intermediaries portal.

A legitimate RIA will provide their registration number upfront and it will match SEBI records.

Step 2. Understand Their Fee Model: Ask clearly whether they are fee-only, AUM-based, or commission-based.

A fee-only or AUM-based SEBI-registered RIA has a legal fiduciary obligation. A commission-based distributor does not.

Step 3. Assess Their Process: A credible advisor starts by understanding your goals, risk profile, and time horizon before recommending any product.

If recommendations begin with products instead of understanding your financial life, that is a clear warning sign.

Step 4. Check Their Certifications: SEBI-registered RIAs must hold NISM certifications.

Additional qualifications like CFP (Certified Financial Planner) or CFA (Chartered Financial Analyst) indicate advanced technical expertise.

Step 5. Review Reporting and Transparency: Ask how often you will receive portfolio reports, how fees are disclosed, and how the advisor handles market corrections.

Transparent documentation and regular communication are the hallmarks of a credible advisory relationship.

Conclusion

Financial advisory services in India have evolved significantly under SEBI's regulatory framework, offering investors access to structured, transparent, and conflict-free professional guidance across personal planning, wealth management, and corporate advisory. The most important decision is not which advisor to choose, but which fee model and type of advisor aligns with your financial complexity and goals.

For most retail investors, a SEBI-registered fee-only or AUM-based RIA is the safest and most aligned choice. For HNIs with ₹50 lakhs or more seeking active portfolio management alongside comprehensive advisory, a combined PMS and RIA service provider like Ckredence Wealth offers the most complete solution.

Investments are subject to market risks. Please read all scheme-related documents carefully before investing. Past performance is not indicative of future returns.

FAQs

What are financial advisory services in India and who regulates them?

Financial advisory services in India include investment planning, wealth management, tax and estate planning, and corporate advisory. They are regulated by the Securities and Exchange Board of India (SEBI) under the Investment Advisers Regulations, 2013. Any professional charging a fee for investment advice must be registered as a SEBI-registered RIA.

How much do financial advisors charge in India?

Fee-only advisors charge ₹15,000 to ₹1,25,000 per year for comprehensive financial planning. AUM-based advisors charge 1% to 2.5% of the portfolio value annually. SEBI caps flat fees at ₹1,25,000 per family per year and AUM fees at 2.5% per annum to ensure fair pricing for investors.

What is the difference between a SEBI-registered RIA and a mutual fund distributor?

A SEBI-registered RIA has a legal fiduciary duty to act in your best interest and charges a direct fee. A mutual fund distributor earns commissions from product manufacturers and is not bound by the same fiduciary obligation, which can create a conflict of interest in their recommendations.

How do I verify a financial advisor's credentials in India?

You can verify any financial advisor's SEBI registration on the official SEBI Intermediaries portal at sebi.gov.in by searching their name or registration number. Confirm that their registration number, validity date, and contact details match what they have provided to you before engaging their services.