8 Min Read

8 Min Read

All-Weather Investing Explained: How India’s HNIs Can Build a Balanced Portfolio for Every Market Cycle

All-Weather Investing Explained: How India’s HNIs Can Build a Balanced Portfolio for Every Market Cycle

All-Weather Investing Explained: How India’s HNIs Can Build a Balanced Portfolio for Every Market Cycle

Discover how HNIs can use an all-weather investing strategy to protect and grow wealth in India via a SEBI-registered PMS approach.

Discover how HNIs can use an all-weather investing strategy to protect and grow wealth in India via a SEBI-registered PMS approach.

Discover how HNIs can use an all-weather investing strategy to protect and grow wealth in India via a SEBI-registered PMS approach.

Ckredence Wealth

Ckredence Wealth

|

According to data published by Securities and Exchange Board of India (SEBI), the total Assets Under Management (AUM) of India’s PMS industry has grown significantly, indicating rising trust among affluent investors. ( Source:- Securities and Exchange Board of India)

If you’re a business owner, a salaried high-net-worth individual (HNI) or part of a family office, you might be asking:

How can I preserve capital when markets swing wildly?

How do I achieve growth without taking outsized risk?

How do I structure a portfolio for tax-efficiency, succession and a legacy in India?

Key Takeaways

A disciplined all-weather portfolio balances growth and capital preservation.

True diversification must span equities, debt, inflation-hedges and alternatives, not just vary within equities.

Risk metrics such as Sharpe ratio, beta and maximum drawdown matter for an HNI-oriented portfolio.

In India, asset-mix must also address tax-optimisation, liquidity needs, family succession and regulatory frameworks.

A SEBI-registered PMS offers customised all-weather design compared to generic mutual funds.

Regular monitoring and rebalancing are essential to keep the portfolio resilient across cycles.

Transparent fee-structure and compliance (SEBI registration) serve as strong trust signals for HNIs.

What is “All-Weather Investing” and why does it matter for HNIs?

An all-weather investing strategy is designed to perform across all market environments, growth up, growth down, inflation high, deflation, interest-rate shock.

At its core, it spreads risk across asset classes such that no single market cycle derails the portfolio. The concept was popularised by firms like Bridgewater Associates in the “All Weather” risk-parity framework.

In India’s context, HNIs and family offices face multiple pressures: market swings, tax rules, legacy planning, liquidity constraints. An all-weather portfolio offers a way to preserve capital while retaining growth potential, rather than chasing only high returns in favourable markets.

Unlike a growth-only strategy, it acknowledges that cycles matter—and that diversification across stress-scenarios is more than just spreading across sectors.

This type of strategy matters because

When equities fall 25-30 % in a correction, having alternate asset classes can cushion the hit.

When inflation surges, real-asset exposure can protect purchasing power.

For HNIs looking at legacy, it helps reduce sequence-risk and increases chance of meeting long-term objectives.

How does an all-weather portfolio differ from a typical mutual fund or PMS offering?

Yes, an all-weather portfolio via a PMS is different from a standard mutual fund or off-the-shelf PMS.

Feature | Typical Mutual Fund | Standard PMS | All-Weather PMS (HNIs) |

Customisation | Low – one size fits many | Medium – segregated accounts | High – tailored asset-mix, liquidity, tax |

Minimum investment | ₹ 5,000 to ₹ 1 Lakh | Typically ₹ 50 Lakh+ (SEBI min) | ₹ 50 Lakh+ or higher, HNI focus |

Asset-class scope | Often equities/debt only | May include alternatives | Equities + debt + inflation-hedges + alt |

Risk-adjusted measures | Less visibility at client level | Available but standard | Emphasis on Sharpe, beta, drawdown |

Regulatory transparency | SEBI registered via AMC & MF | SEBI-registered PMS | Fully SEBI-registered PMS, audited |

Note: SEBI regulates PMS under detailed guidelines (reporting, disclosure, investor eligibility) to protect clients.

For HNIs, the ability to customise matters, you may have specific tax or legacy objectives, require liquidity or prefer capital-preservation, and expect more than just upside.

An all-weather PMS addresses that.

Furthermore, HNI investors with investable assets of ₹ 50 Lakh or more find PMS increasingly relevant. (Source:- CFA Society India)

What are the core principles and asset-mix building blocks of all-weather investing?

An all-weather portfolio is built on one simple idea, no market condition lasts forever. Growth, slowdown, inflation, or rate changes, each phase demands a different response from your investments.

By combining assets that behave differently across these conditions, investors can protect their wealth and still pursue steady growth.

This approach ensures that even when one asset class struggles, another can help balance the impact creating resilience across cycles.

Core Principles of all-weather investing :

1. There’s no single winning asset class.

Market cycles rotate, equities, bonds, and commodities take turns outperforming. Spreading exposure ensures no single event dominates your portfolio’s outcome.

2. The mix matters more than timing.

The right asset allocation drives long-term results. A balanced portfolio blends instruments that react differently to changes in growth, inflation, or policy.

3. Diversify beyond asset types.

True diversification extends to economic conditions. Including gold, real estate investment trusts (REITs), or inflation-indexed bonds offers protection in high-inflation or uncertain environments.

4. Focus on risk-adjusted returns.

Stability is more valuable than short-term highs. Ratios such as Sharpe (>1) and beta (<1) help assess if returns justify the risks taken.

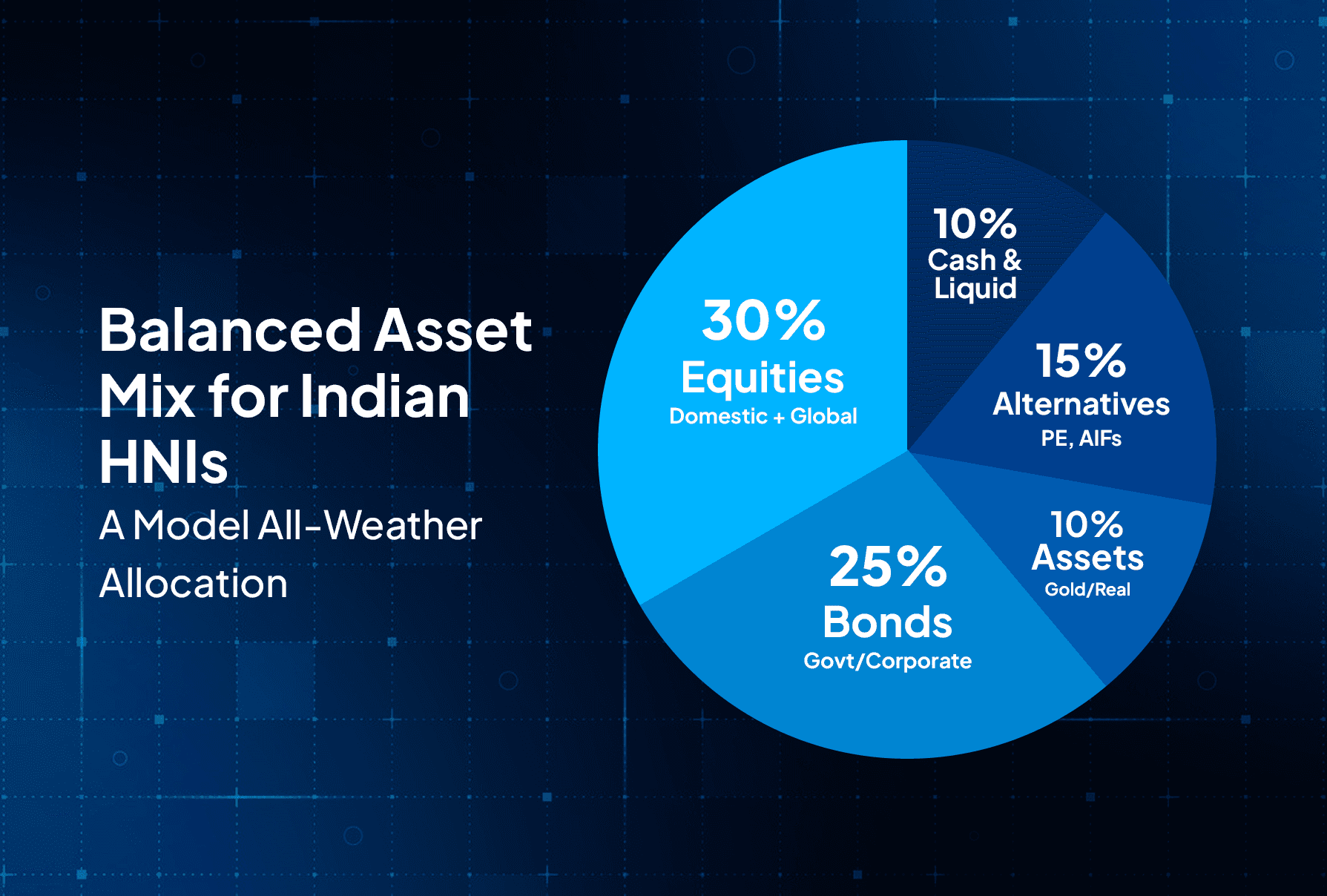

Sample Allocation Framework for Indian HNIs

Asset Class | Allocation Range | Purpose |

Equities (domestic + global) | 30–40 % | Long-term growth |

Government / Corporate Bonds | 25–35 % | Income and stability |

Gold / Commodities / Real Assets | 10–20 % | Inflation hedge |

Alternatives (PE, AIFs, structured credit) | 5–15 % | Diversified alpha |

Cash / Liquid Assets | Up to 10 % | Liquidity buffer |

For India’s high-inflation years (2022–25), exposure to gold and short-duration debt acted as natural stabilisers. Global ETFs or diversified PMS options can further reduce domestic market dependency.

A risk-managed portfolio typically targets 8–12 % annualised volatility with beta below 1, balancing both preservation and growth.

(Banking Frontiers, 2024 – Ultra HNIs allocate ~32 % to equities in India.)

How to implement an all-weather strategy in India via PMS: Ckredence’s approach

Translating the concept into action requires structured execution. One that aligns with Indian regulations, market realities, and investor behaviour. Portfolio Management Services (PMS) provide this framework by offering disciplined asset allocation, continuous monitoring, and custom reporting under SEBI’s supervision.

Key Implementation Elements

1. Strategic Asset Allocation

A PMS portfolio spreads risk across equities, debt, and non-traditional assets to maintain balance across cycles rather than reacting to short-term trends.

2. Transparent Structure and Fees

Investors receive detailed reports, audited statements, and fee models defined by SEBI guidelines, which typically include a fixed component (0.25 % – 2.50 %) and performance-based charges beyond a hurdle rate.

3. Continuous Monitoring

Dedicated portfolio teams track correlations, rebalance assets periodically, and communicate updates through real-time dashboards or digital channels.

4. Personalisation and Compliance

Each investor’s risk profile, liquidity need, and tax position are considered. The structure ensures compliance while aligning portfolios with long-term goals like capital growth, income, or succession planning.

For investors evaluating post-tax returns, our explainer on taxation of mutual funds and PMS provides useful clarity.

Risk management and monitoring: How to keep your all-weather portfolio resilient

Any all-weather strategy succeeds only when risk control is built into its design. Risk management isn’t a one-time exercise, it’s a continuous cycle of measurement, review, and adjustment.

Core Risk Practices for keeping all-weather portfolio resilient are:

1. Regular Rebalancing

Portfolios are reviewed every 6–12 months or after major market events to restore target allocations.

2. Correlation Tracking

Analysts track whether assets are moving in sync. If correlations rise, diversification is reassessed to maintain protection.

3. Drawdown and Volatility Limits

Defined thresholds help investors know when exposure becomes excessive. PMS tools can alert managers if a drawdown breaches pre-set limits.

4. Scenario Planning

Stress tests simulate inflation spikes, rate hikes, or liquidity shocks — crucial for Indian HNIs exposed to domestic and global risks.

5. Transparent Reporting

SEBI mandates monthly and quarterly reports outlining holdings and performance, keeping investors informed and confident.

Such discipline allows HNIs to manage risk proactively rather than react emotionally — ensuring portfolios remain resilient in every environment.

Measuring success: What to expect from an all-weather investing approach

Performance in an all-weather strategy is measured not just by absolute returns but by consistency. The true indicator of success is how well your portfolio compounds while limiting large drawdowns.

Key Performance Indicators

Metric | Typical Target | Meaning |

CAGR | Stable, long-term growth | Measures compounding effect |

Sharpe Ratio > 1 | Efficient return per unit of risk | Reflects stability |

Beta < 1 | Lower volatility vs. market | Indicates diversification benefit |

Max Drawdown < 15 % | Limited downside | Protects capital during shocks |

According to State Street Global Advisors (2024), global all-weather portfolios report up to 40 % lower volatility than pure-equity strategies.

For Indian HNIs, success often means staying invested through uncertainty — achieving smoother compounding, maintaining liquidity, and securing wealth transfer to the next generation.

Why Should You Choose Ckredence?

Credence Wealth Management brings regulatory credibility, data-backed processes, and human expertise together to serve HNI and family-office investors.

A SEBI-registered PMS (Reg. No. INP000007164), the firm manages ₹ 610 Crore + AUM for 435 + clients across Gujarat and Maharashtra, combining a 35-year legacy with modern portfolio technology.

What Sets the Experience Apart:

1. Depth of Experience – Over three decades of PMS and wealth advisory experience provide practical insight into market behaviour and client psychology.

2. All-Weather Design Framework – Every portfolio integrates diversification, risk metrics, and rebalancing schedules tuned for Indian conditions.

3. Transparent Fee Policy – A structured, SEBI-compliant fee range (0.25 % – 2.50 % fixed + performance-linked) ensures clarity from the outset.

4. Client-First Process – Portfolios are personalised around liquidity, tax, and legacy priorities, supported by prompt digital reporting and WhatsApp-based access.

5. Proven Outcomes – Clients using the All-Weather PMS have demonstrated improved risk-adjusted consistency during volatile years (as per internal audited records; past performance is not indicative of future returns).

By blending human judgment with disciplined frameworks, Ckredence offers investors a way to pursue steady, compliant, and transparent wealth creation, year after year.

Conclusion

An all-weather investing framework offers Indian HNIs a way to balance capital preservation with growth, tailor their asset-mix for inflation, currency, interest-rate regimes, and still plan for legacy, taxes and liquidity.

By selecting a SEBI-registered PMS provider like Ckredence, you gain: customisation, transparency, regional understanding and reporting that aligns with HNI expectations.

The key is: build for multiple seasons, monitor consistently, stay disciplined, and work with a team that understands high-net-worth, business-owner and family-office needs.

Ready to take the next step?

Connect with us today and get a portfolio snapshot tailored to your wealth-goals.

FAQs

Q 1. What minimum investment is required for an all-weather PMS in India?

The minimum varies by PMS provider, but SEBI-registered discretionary PMS typically require investments of ₹ 50 Lakh or more.( Source:- The Times of India)

Q 2. Can a mutual fund serve as an all-weather portfolio instead of a PMS?

Mutual funds may offer diversified portfolios, but they lack customisation, liquidity flexibility and HNI-specific structuring found in PMS.

Q 3. How often should I rebalance my all-weather portfolio?

Typically every 6-12 months or after significant market events. Discipline in rebalancing ensures the asset-mix remains aligned.

Q 4. Will an all-weather portfolio guarantee no losses?

No investment approach guarantees zero losses. All-weather strategies aim to reduce volatility and drawdowns, but market risk remains. Full disclosure: past performance is not a guarantee of future results.

Disclaimer: This blog is for informational purposes only. It does not constitute investment advice. Investments in PMS are subject to market risk and regulatory norms of SEBI. Past performance is not necessarily indicative of future performance

According to data published by Securities and Exchange Board of India (SEBI), the total Assets Under Management (AUM) of India’s PMS industry has grown significantly, indicating rising trust among affluent investors. ( Source:- Securities and Exchange Board of India)

If you’re a business owner, a salaried high-net-worth individual (HNI) or part of a family office, you might be asking:

How can I preserve capital when markets swing wildly?

How do I achieve growth without taking outsized risk?

How do I structure a portfolio for tax-efficiency, succession and a legacy in India?

Key Takeaways

A disciplined all-weather portfolio balances growth and capital preservation.

True diversification must span equities, debt, inflation-hedges and alternatives, not just vary within equities.

Risk metrics such as Sharpe ratio, beta and maximum drawdown matter for an HNI-oriented portfolio.

In India, asset-mix must also address tax-optimisation, liquidity needs, family succession and regulatory frameworks.

A SEBI-registered PMS offers customised all-weather design compared to generic mutual funds.

Regular monitoring and rebalancing are essential to keep the portfolio resilient across cycles.

Transparent fee-structure and compliance (SEBI registration) serve as strong trust signals for HNIs.

What is “All-Weather Investing” and why does it matter for HNIs?

An all-weather investing strategy is designed to perform across all market environments, growth up, growth down, inflation high, deflation, interest-rate shock.

At its core, it spreads risk across asset classes such that no single market cycle derails the portfolio. The concept was popularised by firms like Bridgewater Associates in the “All Weather” risk-parity framework.

In India’s context, HNIs and family offices face multiple pressures: market swings, tax rules, legacy planning, liquidity constraints. An all-weather portfolio offers a way to preserve capital while retaining growth potential, rather than chasing only high returns in favourable markets.

Unlike a growth-only strategy, it acknowledges that cycles matter—and that diversification across stress-scenarios is more than just spreading across sectors.

This type of strategy matters because

When equities fall 25-30 % in a correction, having alternate asset classes can cushion the hit.

When inflation surges, real-asset exposure can protect purchasing power.

For HNIs looking at legacy, it helps reduce sequence-risk and increases chance of meeting long-term objectives.

How does an all-weather portfolio differ from a typical mutual fund or PMS offering?

Yes, an all-weather portfolio via a PMS is different from a standard mutual fund or off-the-shelf PMS.

Feature | Typical Mutual Fund | Standard PMS | All-Weather PMS (HNIs) |

Customisation | Low – one size fits many | Medium – segregated accounts | High – tailored asset-mix, liquidity, tax |

Minimum investment | ₹ 5,000 to ₹ 1 Lakh | Typically ₹ 50 Lakh+ (SEBI min) | ₹ 50 Lakh+ or higher, HNI focus |

Asset-class scope | Often equities/debt only | May include alternatives | Equities + debt + inflation-hedges + alt |

Risk-adjusted measures | Less visibility at client level | Available but standard | Emphasis on Sharpe, beta, drawdown |

Regulatory transparency | SEBI registered via AMC & MF | SEBI-registered PMS | Fully SEBI-registered PMS, audited |

Note: SEBI regulates PMS under detailed guidelines (reporting, disclosure, investor eligibility) to protect clients.

For HNIs, the ability to customise matters, you may have specific tax or legacy objectives, require liquidity or prefer capital-preservation, and expect more than just upside.

An all-weather PMS addresses that.

Furthermore, HNI investors with investable assets of ₹ 50 Lakh or more find PMS increasingly relevant. (Source:- CFA Society India)

What are the core principles and asset-mix building blocks of all-weather investing?

An all-weather portfolio is built on one simple idea, no market condition lasts forever. Growth, slowdown, inflation, or rate changes, each phase demands a different response from your investments.

By combining assets that behave differently across these conditions, investors can protect their wealth and still pursue steady growth.

This approach ensures that even when one asset class struggles, another can help balance the impact creating resilience across cycles.

Core Principles of all-weather investing :

1. There’s no single winning asset class.

Market cycles rotate, equities, bonds, and commodities take turns outperforming. Spreading exposure ensures no single event dominates your portfolio’s outcome.

2. The mix matters more than timing.

The right asset allocation drives long-term results. A balanced portfolio blends instruments that react differently to changes in growth, inflation, or policy.

3. Diversify beyond asset types.

True diversification extends to economic conditions. Including gold, real estate investment trusts (REITs), or inflation-indexed bonds offers protection in high-inflation or uncertain environments.

4. Focus on risk-adjusted returns.

Stability is more valuable than short-term highs. Ratios such as Sharpe (>1) and beta (<1) help assess if returns justify the risks taken.

Sample Allocation Framework for Indian HNIs

Asset Class | Allocation Range | Purpose |

Equities (domestic + global) | 30–40 % | Long-term growth |

Government / Corporate Bonds | 25–35 % | Income and stability |

Gold / Commodities / Real Assets | 10–20 % | Inflation hedge |

Alternatives (PE, AIFs, structured credit) | 5–15 % | Diversified alpha |

Cash / Liquid Assets | Up to 10 % | Liquidity buffer |

For India’s high-inflation years (2022–25), exposure to gold and short-duration debt acted as natural stabilisers. Global ETFs or diversified PMS options can further reduce domestic market dependency.

A risk-managed portfolio typically targets 8–12 % annualised volatility with beta below 1, balancing both preservation and growth.

(Banking Frontiers, 2024 – Ultra HNIs allocate ~32 % to equities in India.)

How to implement an all-weather strategy in India via PMS: Ckredence’s approach

Translating the concept into action requires structured execution. One that aligns with Indian regulations, market realities, and investor behaviour. Portfolio Management Services (PMS) provide this framework by offering disciplined asset allocation, continuous monitoring, and custom reporting under SEBI’s supervision.

Key Implementation Elements

1. Strategic Asset Allocation

A PMS portfolio spreads risk across equities, debt, and non-traditional assets to maintain balance across cycles rather than reacting to short-term trends.

2. Transparent Structure and Fees

Investors receive detailed reports, audited statements, and fee models defined by SEBI guidelines, which typically include a fixed component (0.25 % – 2.50 %) and performance-based charges beyond a hurdle rate.

3. Continuous Monitoring

Dedicated portfolio teams track correlations, rebalance assets periodically, and communicate updates through real-time dashboards or digital channels.

4. Personalisation and Compliance

Each investor’s risk profile, liquidity need, and tax position are considered. The structure ensures compliance while aligning portfolios with long-term goals like capital growth, income, or succession planning.

For investors evaluating post-tax returns, our explainer on taxation of mutual funds and PMS provides useful clarity.

Risk management and monitoring: How to keep your all-weather portfolio resilient

Any all-weather strategy succeeds only when risk control is built into its design. Risk management isn’t a one-time exercise, it’s a continuous cycle of measurement, review, and adjustment.

Core Risk Practices for keeping all-weather portfolio resilient are:

1. Regular Rebalancing

Portfolios are reviewed every 6–12 months or after major market events to restore target allocations.

2. Correlation Tracking

Analysts track whether assets are moving in sync. If correlations rise, diversification is reassessed to maintain protection.

3. Drawdown and Volatility Limits

Defined thresholds help investors know when exposure becomes excessive. PMS tools can alert managers if a drawdown breaches pre-set limits.

4. Scenario Planning

Stress tests simulate inflation spikes, rate hikes, or liquidity shocks — crucial for Indian HNIs exposed to domestic and global risks.

5. Transparent Reporting

SEBI mandates monthly and quarterly reports outlining holdings and performance, keeping investors informed and confident.

Such discipline allows HNIs to manage risk proactively rather than react emotionally — ensuring portfolios remain resilient in every environment.

Measuring success: What to expect from an all-weather investing approach

Performance in an all-weather strategy is measured not just by absolute returns but by consistency. The true indicator of success is how well your portfolio compounds while limiting large drawdowns.

Key Performance Indicators

Metric | Typical Target | Meaning |

CAGR | Stable, long-term growth | Measures compounding effect |

Sharpe Ratio > 1 | Efficient return per unit of risk | Reflects stability |

Beta < 1 | Lower volatility vs. market | Indicates diversification benefit |

Max Drawdown < 15 % | Limited downside | Protects capital during shocks |

According to State Street Global Advisors (2024), global all-weather portfolios report up to 40 % lower volatility than pure-equity strategies.

For Indian HNIs, success often means staying invested through uncertainty — achieving smoother compounding, maintaining liquidity, and securing wealth transfer to the next generation.

Why Should You Choose Ckredence?

Credence Wealth Management brings regulatory credibility, data-backed processes, and human expertise together to serve HNI and family-office investors.

A SEBI-registered PMS (Reg. No. INP000007164), the firm manages ₹ 610 Crore + AUM for 435 + clients across Gujarat and Maharashtra, combining a 35-year legacy with modern portfolio technology.

What Sets the Experience Apart:

1. Depth of Experience – Over three decades of PMS and wealth advisory experience provide practical insight into market behaviour and client psychology.

2. All-Weather Design Framework – Every portfolio integrates diversification, risk metrics, and rebalancing schedules tuned for Indian conditions.

3. Transparent Fee Policy – A structured, SEBI-compliant fee range (0.25 % – 2.50 % fixed + performance-linked) ensures clarity from the outset.

4. Client-First Process – Portfolios are personalised around liquidity, tax, and legacy priorities, supported by prompt digital reporting and WhatsApp-based access.

5. Proven Outcomes – Clients using the All-Weather PMS have demonstrated improved risk-adjusted consistency during volatile years (as per internal audited records; past performance is not indicative of future returns).

By blending human judgment with disciplined frameworks, Ckredence offers investors a way to pursue steady, compliant, and transparent wealth creation, year after year.

Conclusion

An all-weather investing framework offers Indian HNIs a way to balance capital preservation with growth, tailor their asset-mix for inflation, currency, interest-rate regimes, and still plan for legacy, taxes and liquidity.

By selecting a SEBI-registered PMS provider like Ckredence, you gain: customisation, transparency, regional understanding and reporting that aligns with HNI expectations.

The key is: build for multiple seasons, monitor consistently, stay disciplined, and work with a team that understands high-net-worth, business-owner and family-office needs.

Ready to take the next step?

Connect with us today and get a portfolio snapshot tailored to your wealth-goals.

FAQs

Q 1. What minimum investment is required for an all-weather PMS in India?

The minimum varies by PMS provider, but SEBI-registered discretionary PMS typically require investments of ₹ 50 Lakh or more.( Source:- The Times of India)

Q 2. Can a mutual fund serve as an all-weather portfolio instead of a PMS?

Mutual funds may offer diversified portfolios, but they lack customisation, liquidity flexibility and HNI-specific structuring found in PMS.

Q 3. How often should I rebalance my all-weather portfolio?

Typically every 6-12 months or after significant market events. Discipline in rebalancing ensures the asset-mix remains aligned.

Q 4. Will an all-weather portfolio guarantee no losses?

No investment approach guarantees zero losses. All-weather strategies aim to reduce volatility and drawdowns, but market risk remains. Full disclosure: past performance is not a guarantee of future results.

Disclaimer: This blog is for informational purposes only. It does not constitute investment advice. Investments in PMS are subject to market risk and regulatory norms of SEBI. Past performance is not necessarily indicative of future performance