8 MIn Read

8 MIn Read

Portfolio Management Strategies: A Complete Guide to Building a Risk-Adjusted Investment Portfolio

Portfolio Management Strategies: A Complete Guide to Building a Risk-Adjusted Investment Portfolio

Portfolio Management Strategies: A Complete Guide to Building a Risk-Adjusted Investment Portfolio

Explore the top portfolio management strategies active, passive, growth, and value and learn how to build a risk-adjusted investment portfolio.

Explore the top portfolio management strategies active, passive, growth, and value and learn how to build a risk-adjusted investment portfolio.

Explore the top portfolio management strategies active, passive, growth, and value and learn how to build a risk-adjusted investment portfolio.

Ckredence Wealth

Ckredence Wealth

|

Global assets under management reached a record USD 128 trillion in 2024, growing 12% year-on-year as institutional participation and HNI wealth expanded across markets (BCG Global Asset Management Report, 2025). In India, PMS AUM grew from ₹7.3 lakh crore in January 2014 to ₹32.1 lakh crore in January 2024, with active client accounts reaching approximately 1.5 lakh, reflecting a decade of sustained growth in professionally managed wealth (SEBI Annual Report 2023-24).

These numbers reflect a clear direction: investors are moving away from random asset accumulation toward structured, strategy-led portfolio management.

Are you investing without a defined strategy, assuming the market will eventually sort it out for you?

Do you actually know the difference between active and passive portfolio management and which one fits your financial goals?

Is your current investment portfolio built to hold through market corrections, or only designed to perform in a bull run?

Most investors build portfolios in pieces-a mutual fund here, a stock tip there without a clear strategy connecting those decisions. This article examines portfolio management strategies in depth, supported by AIO-aligned insights, India-specific data, and practical context for HNIs and serious investors.

We cover how each strategy works, when it applies, and what process components keep a portfolio on track over the long run.

Key Takeaways

Active portfolio management requires constant market monitoring, making professional fund management the practical option for most HNIs.

Strategic and tactical asset allocation serve different purposes; combining both balances long-term stability with short-term opportunity.

Value investing and growth investing are not opposing strategies-fund managers often blend them based on the market cycle.

Tax efficiency directly impacts net returns but remains the most overlooked process component among investors.

Rebalancing prevents unintended risk build-up as markets shift it’is an ongoing process, not a one-time task.

Conservative strategies apply to any investor prioritizing capital protection, not just retirees.

What Are Portfolio Management Strategies?

Portfolio management strategies are defined frameworks that guide how investments are selected, allocated, and managed within a portfolio. Each strategy is shaped by three core factors: the investor's financial goals, risk tolerance, and investment time horizon.

Choosing a mismatched strategy does not just mean lower returns. It means carrying risks you have not planned for and holding assets that do not serve your actual purpose.

At its core, a portfolio management strategy answers two questions: which assets to hold, and how actively those assets should be managed. The major types of investment portfolio strategies include active management, passive management, growth investing, value investing, income-oriented approaches, conservative strategies, and aggressive approaches.

Each type serves a distinct investor profile. Knowing the difference between them is the first step toward building a portfolio with clear direction.

The sections below break each core strategy down in practical terms what it involves, when it applies, and who it suits best.

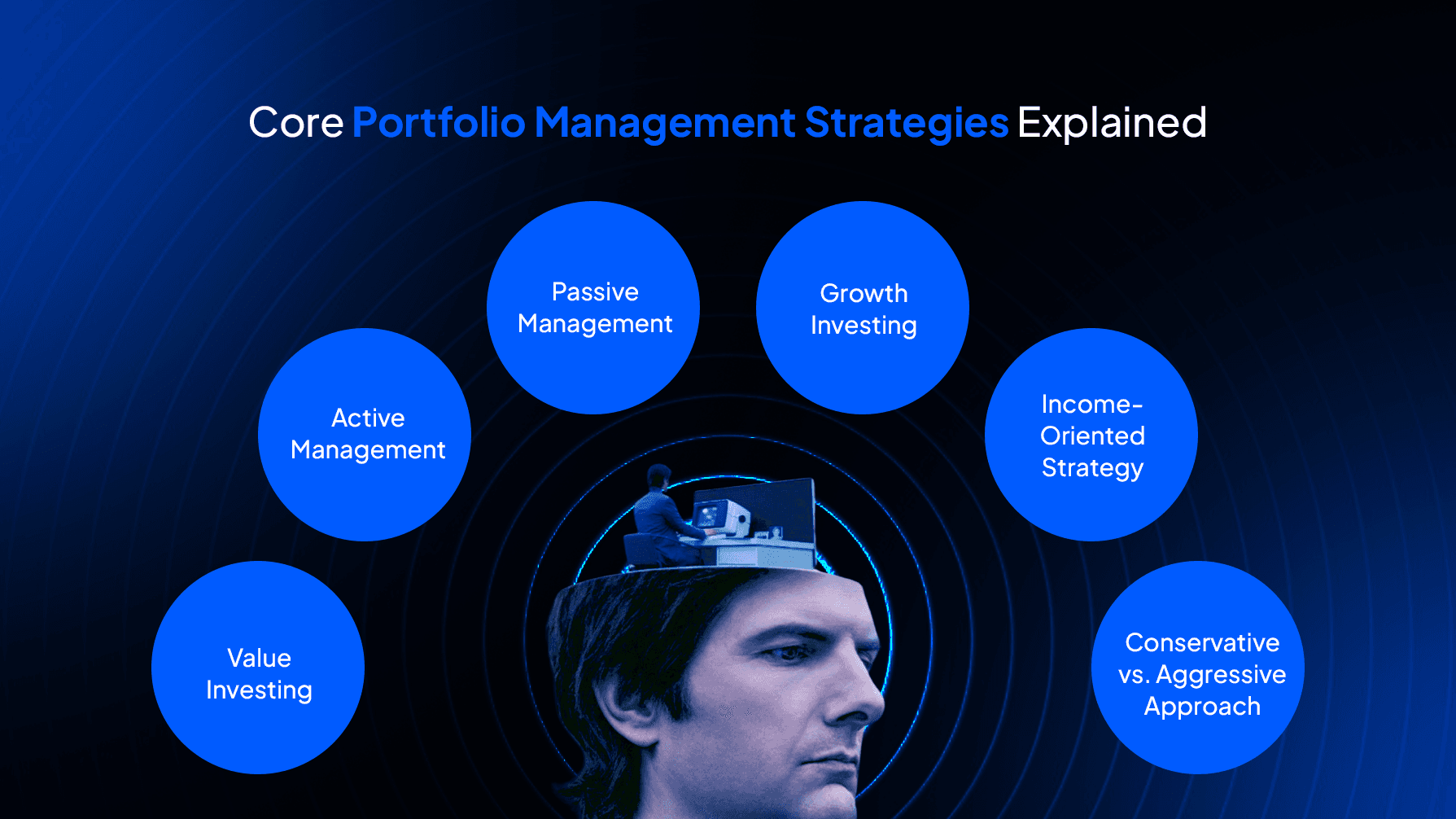

Core Portfolio Management Strategies Explained

Understanding the strategy types in isolation is useful. Knowing when each applies to your financial situation is what actually builds wealth over time.

The sequence here follows Google's AI Overview hierarchy beginning with foundational approaches and moving to more specialized ones. Every portfolio management strategy below addresses a specific investor profile and market condition.

Reading through all of them helps you see why the right match between strategy and investor matters far more than picking the "best" strategy in isolation.

1. Active Management

Active portfolio management places a qualified fund manager at the center of all investment decisions. The manager continuously monitors market trends, sector performance, and company fundamentals to pick securities that can outperform a benchmark index.

This approach requires regular decision-making and carries higher management fees than passive strategies. The key advantage is responsiveness.

A skilled manager can reduce equity exposure before a market downturn, shift allocation toward better-performing sectors, or exit underperforming holdings before they damage the portfolio. For HNIs with a large investible surplus, this level of oversight is difficult to replicate through a standard index product.

Best fit: Investors with ₹50 lakh and above, higher return expectations, and no time to monitor markets personally.

2. Passive Management

Passive portfolio management removes human stock-picking from the equation. The portfolio tracks a benchmark index such as the Nifty 50 or Sensex by holding the same stocks at the same weights.

Trading is minimal, keeping costs low and removing emotional decision-making from the process. This strategy suits long-term investors who prefer steady, index-matching growth over active risk-taking.

It works well in market conditions where active managers struggle to consistently beat the benchmark. For first-time investors building a base, passive investing through index funds or ETFs is a practical starting point.

Best fit: Investors with a longer horizon of ten or more years, lower cost preference, and a goal of market-matching returns.

3. Growth Investing

Growth investing focuses on companies with strong future earning potential often at valuations that appear stretched in the present. The logic is that revenue growth, competitive positioning, and scalability will justify the premium over a longer time period.

This strategy performs well in bull markets and expanding economic cycles. Growth investing carries higher short-term volatility.

Price corrections in growth stocks can be sharp when market sentiment shifts. For investors who can hold through cycles without panic-selling, it has historically delivered strong capital appreciation over seven-year-plus horizons.

Best fit: Long investment horizon, higher risk appetite, professional monitoring by an active fund manager.

4. Value Investing

Value investing identifies stocks trading below their intrinsic worth companies the market has temporarily mispriced or overlooked due to short-term sentiment. The strategy requires research-heavy fundamental analysis and, above all, patience.

Market recognition of an undervalued stock can take months or years to materialize. This approach is less reactive to short-term market noise.

It builds a natural margin of safety into portfolio construction. For investors who are risk-conscious but still want equity exposure, value investing offers a more measured path to capital appreciation than pure growth strategies.

Best fit: Moderate risk tolerance, sideways or correction phases in markets, fund manager with strong fundamental research capability.

5. Income-Oriented Strategy

This strategy focuses on generating regular cash flow rather than capital appreciation. It targets dividend-paying stocks, corporate bonds, non-convertible debentures, and fixed-income mutual fund categories.

In India, this includes high-yield PSU stocks, banking sector dividends, and structured monthly income plans. Income-oriented portfolio management suits investors who need predictable returns from their corpus.

It pairs naturally with a conservative or moderate risk profile and works well as a complement within a broader, diversified investment portfolio strategy.

6. Conservative vs. Aggressive Approach

A conservative approach places capital preservation at the top. It allocates the majority of the portfolio to debt instruments, sovereign bonds, large-cap equities, and gold.

Returns are lower, but downside protection is strong. This is not only a retiree strategy it applies to any investor whose primary concern is protecting what they have already built.

An aggressive approach targets maximum growth through high-risk assets: small-cap equities, sector-specific funds, and alternative investments. It suits investors with a long enough runway to absorb volatility without disrupting near-term financial needs.

Most investor portfolios sit between these two ends. A professional PMS builds the right blend based on actual risk assessment not assumptions and adjusts it as goals and market conditions shift.

The next section covers the process components that hold whichever strategy you choose firmly in place.

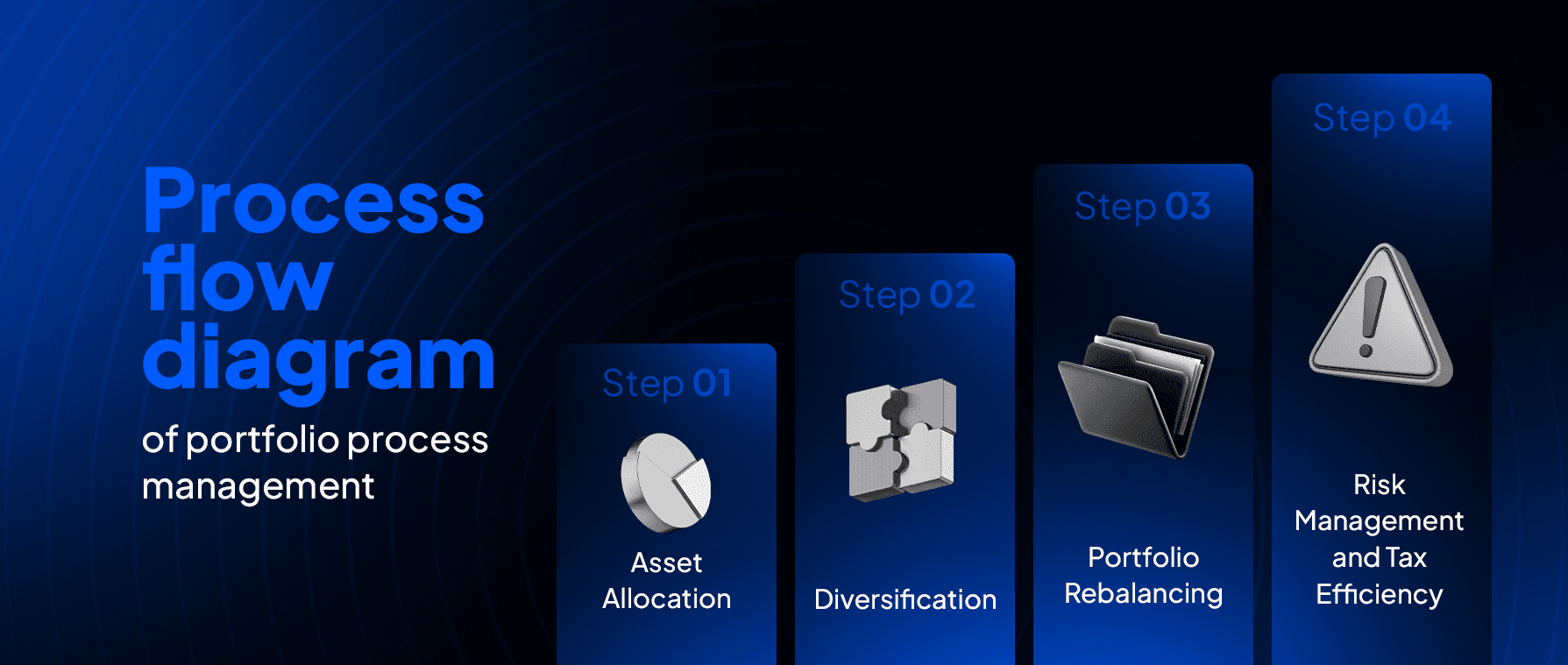

Key Process Components That Drive Long-Term Portfolio Performance

Strategy selection draws the most attention from investors. What actually determines real, long-term portfolio performance is the execution process behind the strategy.

These four components come directly from Google's AI Overview results. They are the operational backbone of every serious investment portfolio strategy.

Getting these right is what separates a professionally managed portfolio from one that is informally assembled and periodically forgotten. Even the best portfolio management strategy produces inconsistent results without a disciplined process behind it.

The key steps involved in portfolio process management are:

Step 1 - Asset Allocation Distribute capital across asset classes: equities, debt, gold, and alternative investments. This limits the damage any single underperforming asset class can do to the overall portfolio.

The right mix depends entirely on the investor's risk profile and time horizon. No two investors should hold the same allocation.

Step 2 - Diversification Diversification goes beyond spreading across asset classes. Within equities alone, concentration in a single sector creates hidden risk.

A well-diversified investment portfolio holds assets with low or negative correlation. When one declines, others provide a counterbalance.

Step 3 - Portfolio Rebalancing Markets shift asset allocations over time without any conscious decision being made. A 60/40 equity-debt split can drift to 75/25 after a sustained equity rally, exposing the investor to more risk than originally planned.

Rebalancing corrects that drift. Annual or semi-annual reviews are standard practice for professionally managed portfolios.

Step 4 - Risk Management and Tax Efficiency Risk management means aligning every investment decision with the investor's risk tolerance and time horizon. It covers sector concentration, liquidity buffers, and rebalancing thresholds.

Tax efficiency structuring investments to reduce capital gains liabilities directly affects net returns. A well-run PMS addresses tax efficiency at the portfolio construction stage, not just at exit.

These four steps work as a connected system. A strong strategy without disciplined process execution produces inconsistent results.

This is the clearest operational difference between professional portfolio management and self-directed investing. The next section adds a practical framework that ties these components together.

The 70:20:10 Rule and Modern Tools in Portfolio Management

The 70:20:10 portfolio framework is one of the most widely referenced allocation rules in investment management. It divides a portfolio into three risk tiers low, medium, and high giving investors a disciplined starting point when distributing capital across asset classes.

It is not rigid. It adjusts based on age, goals, and current market conditions.

As a base framework, it reduces arbitrary allocation and brings structure to portfolio construction from day one. This rule is particularly useful for first-time PMS clients and HNIs reviewing an existing portfolio with a professional fund manager for the first time.

It provides a shared reference point for conversations about risk exposure, rebalancing targets, and the right blend of instruments.

AI and Data Tools in Modern Portfolio Management

Modern portfolio management extends well beyond spreadsheets and annual reviews. Professional fund managers now use real-time data monitoring platforms, AI-driven risk assessment tools, and scenario simulation software to analyse market patterns across asset classes.

These systems improve decision accuracy and reduce response time during periods of market volatility. For individual investors, the practical implication is clear.

Fund managers backed by technology platforms are better placed to manage complex portfolios than those relying on manual tracking. This is a key reason why institutional-grade PMS services have become the preferred choice for HNIs managing large investible surpluses.

Technology does not replace judgment it gives the fund manager better inputs to act on faster. The next section brings all of this together into a decision framework for choosing the right approach for your own financial goals.

How to Choose the Right Portfolio Management Strategy

Not every portfolio management strategy suits every investor. The right one depends on specific answers to a few core questions each of which must connect to your actual financial situation, not just your preferences.

Investors often choose a strategy based on what performed well in the recent past. That is a risk.

The right strategy is the one that fits your current financial capacity and long-term goals regardless of what is trending in the market right now.

What Is Your Investment Time Horizon?

Investors with a ten-year or longer horizon can absorb short-term market swings without impact on their final corpus. This makes growth investing and active management viable options.

Shorter horizons call for income-oriented or conservative strategies that limit downside and protect accumulated wealth. The time horizon also determines how much rebalancing flexibility the portfolio has.

A longer runway allows a fund manager to hold through market corrections without being forced into early exits. A shorter one requires a more defensive structure from the start.

What Is Your Actual Risk Capacity?

Risk tolerance is not just psychological comfort with volatility it is the financial capacity to absorb losses without disrupting real life. An HNI with a large investible surplus carries a different risk capacity than a professional managing a tighter savings pool.

Portfolio management strategies must match both the comfort level and the real financial buffer of the investor. Confusing risk preference with risk capacity is one of the most common mistakes in portfolio construction.

A fund manager's first task is to separate the two and build accordingly.

Do You Have the Time and Expertise to Monitor Your Portfolio?

Active investment portfolio strategies require regular market attention weekly at minimum. If that commitment is not realistic, professional management through a SEBI-registered PMS provider is the practical answer.

It places monitoring responsibility with a dedicated fund manager and removes emotion-driven decisions during market corrections. The right strategy is the one that gets executed consistently over years not just the one that sounds best in a good market.

Choosing well and maintaining discipline are what separate investors who build lasting wealth from those who don't. The next section shows how Ckredence Wealth puts all of this into practice for its clients.

Why Should You Choose Ckredence Wealth for Portfolio Management?

HNIs and UHNIs need portfolio management strategies that go well beyond general advice. Your investment portfolio deserves decisions built on 37 years of market experience, SEBI-regulated expertise, and a research-backed approach to every market cycle.

Solutions That Matter:

Four distinct PMS strategies-All Weather, Diversified, Business Cycle, and ICE Growth-each built for different market conditions and investor goals

SEBI-registered professional management (INP000007164) with transparent, performance-aligned fee structures

Risk-adjusted portfolio construction across equity, debt, and alternative asset classes

Proven Performance in Wealth Management:

₹805+ Crores in AUM managed across 376 active clients

CIO-led investment decisions backed by deep sector research and fundamental analysis

Branch offices in Surat, Mumbai, and Vadodara for direct, relationship-based advisory

Every portfolio management strategy at Ckredence Wealth is matched to the individual investor's financial profile, risk capacity, and long-term goals from first-time PMS clients to multi-generational family offices. Your wealth deserves that level of attention.

Ready to build a portfolio strategy that works through every market cycle? Schedule a Consultation with Ckredence Wealth.

Conclusion

Portfolio management strategies are not interchangeable products they are structured approaches matched to specific investor goals, risk profiles, and time horizons.

Active and growth-oriented strategies serve investors seeking market-beating returns with professional oversight.

Conservative and income-oriented strategies protect capital and generate steady returns for risk-aware investors.

Process components-asset allocation, diversification, rebalancing, and tax efficienc-drive long-term outcomes more than strategy selection alone.

Professional PMS management through a SEBI-registered firm gives HNIs access to institutional-grade portfolio construction without the burden of daily monitoring.

A strong investment portfolio is not built in a single decision. It is built through a disciplined strategy, executed consistently, reviewed regularly, and adjusted with clear purpose.

FAQs

Q1: What is the best portfolio management strategy for long-term wealth creation?

The best portfolio management strategy for long-term wealth creation among HNIs is Active management with strategic asset allocation. A SEBI-registered PMS provider builds a strategy around your specific financial goals. The best approach depends on your time horizon and comfort with market volatility.

Q2: What is the difference between active and passive portfolio management strategies?

Active portfolio management involves fund managers making regular decisions to outperform a benchmark index. Passive management tracks an index like the Nifty 50 with minimal trading and lower costs. Active management suits investors with specific goals that a passive product cannot address.

Q3: What is the 70:20:10 rule in investment portfolio management? The 70:20:10 rule in investment portfolio management is to divides a portfolio into three risk tiers: low, medium, and high risk. It helps investors distribute capital across asset classes in a disciplined, structured way. The exact split adjusts based on individual risk tolerance, goals, and market conditions.

Q4: How often should you rebalance your investment portfolio? Portfolio rebalancing should happen at least once a year or when allocation drifts notably from the original target. Market movements can shift your equity-debt ratio beyond your intended risk level. Regular rebalancing keeps portfolio management strategies aligned with your long-term financial plan.

Global assets under management reached a record USD 128 trillion in 2024, growing 12% year-on-year as institutional participation and HNI wealth expanded across markets (BCG Global Asset Management Report, 2025). In India, PMS AUM grew from ₹7.3 lakh crore in January 2014 to ₹32.1 lakh crore in January 2024, with active client accounts reaching approximately 1.5 lakh, reflecting a decade of sustained growth in professionally managed wealth (SEBI Annual Report 2023-24).

These numbers reflect a clear direction: investors are moving away from random asset accumulation toward structured, strategy-led portfolio management.

Are you investing without a defined strategy, assuming the market will eventually sort it out for you?

Do you actually know the difference between active and passive portfolio management and which one fits your financial goals?

Is your current investment portfolio built to hold through market corrections, or only designed to perform in a bull run?

Most investors build portfolios in pieces-a mutual fund here, a stock tip there without a clear strategy connecting those decisions. This article examines portfolio management strategies in depth, supported by AIO-aligned insights, India-specific data, and practical context for HNIs and serious investors.

We cover how each strategy works, when it applies, and what process components keep a portfolio on track over the long run.

Key Takeaways

Active portfolio management requires constant market monitoring, making professional fund management the practical option for most HNIs.

Strategic and tactical asset allocation serve different purposes; combining both balances long-term stability with short-term opportunity.

Value investing and growth investing are not opposing strategies-fund managers often blend them based on the market cycle.

Tax efficiency directly impacts net returns but remains the most overlooked process component among investors.

Rebalancing prevents unintended risk build-up as markets shift it’is an ongoing process, not a one-time task.

Conservative strategies apply to any investor prioritizing capital protection, not just retirees.

What Are Portfolio Management Strategies?

Portfolio management strategies are defined frameworks that guide how investments are selected, allocated, and managed within a portfolio. Each strategy is shaped by three core factors: the investor's financial goals, risk tolerance, and investment time horizon.

Choosing a mismatched strategy does not just mean lower returns. It means carrying risks you have not planned for and holding assets that do not serve your actual purpose.

At its core, a portfolio management strategy answers two questions: which assets to hold, and how actively those assets should be managed. The major types of investment portfolio strategies include active management, passive management, growth investing, value investing, income-oriented approaches, conservative strategies, and aggressive approaches.

Each type serves a distinct investor profile. Knowing the difference between them is the first step toward building a portfolio with clear direction.

The sections below break each core strategy down in practical terms what it involves, when it applies, and who it suits best.

Core Portfolio Management Strategies Explained

Understanding the strategy types in isolation is useful. Knowing when each applies to your financial situation is what actually builds wealth over time.

The sequence here follows Google's AI Overview hierarchy beginning with foundational approaches and moving to more specialized ones. Every portfolio management strategy below addresses a specific investor profile and market condition.

Reading through all of them helps you see why the right match between strategy and investor matters far more than picking the "best" strategy in isolation.

1. Active Management

Active portfolio management places a qualified fund manager at the center of all investment decisions. The manager continuously monitors market trends, sector performance, and company fundamentals to pick securities that can outperform a benchmark index.

This approach requires regular decision-making and carries higher management fees than passive strategies. The key advantage is responsiveness.

A skilled manager can reduce equity exposure before a market downturn, shift allocation toward better-performing sectors, or exit underperforming holdings before they damage the portfolio. For HNIs with a large investible surplus, this level of oversight is difficult to replicate through a standard index product.

Best fit: Investors with ₹50 lakh and above, higher return expectations, and no time to monitor markets personally.

2. Passive Management

Passive portfolio management removes human stock-picking from the equation. The portfolio tracks a benchmark index such as the Nifty 50 or Sensex by holding the same stocks at the same weights.

Trading is minimal, keeping costs low and removing emotional decision-making from the process. This strategy suits long-term investors who prefer steady, index-matching growth over active risk-taking.

It works well in market conditions where active managers struggle to consistently beat the benchmark. For first-time investors building a base, passive investing through index funds or ETFs is a practical starting point.

Best fit: Investors with a longer horizon of ten or more years, lower cost preference, and a goal of market-matching returns.

3. Growth Investing

Growth investing focuses on companies with strong future earning potential often at valuations that appear stretched in the present. The logic is that revenue growth, competitive positioning, and scalability will justify the premium over a longer time period.

This strategy performs well in bull markets and expanding economic cycles. Growth investing carries higher short-term volatility.

Price corrections in growth stocks can be sharp when market sentiment shifts. For investors who can hold through cycles without panic-selling, it has historically delivered strong capital appreciation over seven-year-plus horizons.

Best fit: Long investment horizon, higher risk appetite, professional monitoring by an active fund manager.

4. Value Investing

Value investing identifies stocks trading below their intrinsic worth companies the market has temporarily mispriced or overlooked due to short-term sentiment. The strategy requires research-heavy fundamental analysis and, above all, patience.

Market recognition of an undervalued stock can take months or years to materialize. This approach is less reactive to short-term market noise.

It builds a natural margin of safety into portfolio construction. For investors who are risk-conscious but still want equity exposure, value investing offers a more measured path to capital appreciation than pure growth strategies.

Best fit: Moderate risk tolerance, sideways or correction phases in markets, fund manager with strong fundamental research capability.

5. Income-Oriented Strategy

This strategy focuses on generating regular cash flow rather than capital appreciation. It targets dividend-paying stocks, corporate bonds, non-convertible debentures, and fixed-income mutual fund categories.

In India, this includes high-yield PSU stocks, banking sector dividends, and structured monthly income plans. Income-oriented portfolio management suits investors who need predictable returns from their corpus.

It pairs naturally with a conservative or moderate risk profile and works well as a complement within a broader, diversified investment portfolio strategy.

6. Conservative vs. Aggressive Approach

A conservative approach places capital preservation at the top. It allocates the majority of the portfolio to debt instruments, sovereign bonds, large-cap equities, and gold.

Returns are lower, but downside protection is strong. This is not only a retiree strategy it applies to any investor whose primary concern is protecting what they have already built.

An aggressive approach targets maximum growth through high-risk assets: small-cap equities, sector-specific funds, and alternative investments. It suits investors with a long enough runway to absorb volatility without disrupting near-term financial needs.

Most investor portfolios sit between these two ends. A professional PMS builds the right blend based on actual risk assessment not assumptions and adjusts it as goals and market conditions shift.

The next section covers the process components that hold whichever strategy you choose firmly in place.

Key Process Components That Drive Long-Term Portfolio Performance

Strategy selection draws the most attention from investors. What actually determines real, long-term portfolio performance is the execution process behind the strategy.

These four components come directly from Google's AI Overview results. They are the operational backbone of every serious investment portfolio strategy.

Getting these right is what separates a professionally managed portfolio from one that is informally assembled and periodically forgotten. Even the best portfolio management strategy produces inconsistent results without a disciplined process behind it.

The key steps involved in portfolio process management are:

Step 1 - Asset Allocation Distribute capital across asset classes: equities, debt, gold, and alternative investments. This limits the damage any single underperforming asset class can do to the overall portfolio.

The right mix depends entirely on the investor's risk profile and time horizon. No two investors should hold the same allocation.

Step 2 - Diversification Diversification goes beyond spreading across asset classes. Within equities alone, concentration in a single sector creates hidden risk.

A well-diversified investment portfolio holds assets with low or negative correlation. When one declines, others provide a counterbalance.

Step 3 - Portfolio Rebalancing Markets shift asset allocations over time without any conscious decision being made. A 60/40 equity-debt split can drift to 75/25 after a sustained equity rally, exposing the investor to more risk than originally planned.

Rebalancing corrects that drift. Annual or semi-annual reviews are standard practice for professionally managed portfolios.

Step 4 - Risk Management and Tax Efficiency Risk management means aligning every investment decision with the investor's risk tolerance and time horizon. It covers sector concentration, liquidity buffers, and rebalancing thresholds.

Tax efficiency structuring investments to reduce capital gains liabilities directly affects net returns. A well-run PMS addresses tax efficiency at the portfolio construction stage, not just at exit.

These four steps work as a connected system. A strong strategy without disciplined process execution produces inconsistent results.

This is the clearest operational difference between professional portfolio management and self-directed investing. The next section adds a practical framework that ties these components together.

The 70:20:10 Rule and Modern Tools in Portfolio Management

The 70:20:10 portfolio framework is one of the most widely referenced allocation rules in investment management. It divides a portfolio into three risk tiers low, medium, and high giving investors a disciplined starting point when distributing capital across asset classes.

It is not rigid. It adjusts based on age, goals, and current market conditions.

As a base framework, it reduces arbitrary allocation and brings structure to portfolio construction from day one. This rule is particularly useful for first-time PMS clients and HNIs reviewing an existing portfolio with a professional fund manager for the first time.

It provides a shared reference point for conversations about risk exposure, rebalancing targets, and the right blend of instruments.

AI and Data Tools in Modern Portfolio Management

Modern portfolio management extends well beyond spreadsheets and annual reviews. Professional fund managers now use real-time data monitoring platforms, AI-driven risk assessment tools, and scenario simulation software to analyse market patterns across asset classes.

These systems improve decision accuracy and reduce response time during periods of market volatility. For individual investors, the practical implication is clear.

Fund managers backed by technology platforms are better placed to manage complex portfolios than those relying on manual tracking. This is a key reason why institutional-grade PMS services have become the preferred choice for HNIs managing large investible surpluses.

Technology does not replace judgment it gives the fund manager better inputs to act on faster. The next section brings all of this together into a decision framework for choosing the right approach for your own financial goals.

How to Choose the Right Portfolio Management Strategy

Not every portfolio management strategy suits every investor. The right one depends on specific answers to a few core questions each of which must connect to your actual financial situation, not just your preferences.

Investors often choose a strategy based on what performed well in the recent past. That is a risk.

The right strategy is the one that fits your current financial capacity and long-term goals regardless of what is trending in the market right now.

What Is Your Investment Time Horizon?

Investors with a ten-year or longer horizon can absorb short-term market swings without impact on their final corpus. This makes growth investing and active management viable options.

Shorter horizons call for income-oriented or conservative strategies that limit downside and protect accumulated wealth. The time horizon also determines how much rebalancing flexibility the portfolio has.

A longer runway allows a fund manager to hold through market corrections without being forced into early exits. A shorter one requires a more defensive structure from the start.

What Is Your Actual Risk Capacity?

Risk tolerance is not just psychological comfort with volatility it is the financial capacity to absorb losses without disrupting real life. An HNI with a large investible surplus carries a different risk capacity than a professional managing a tighter savings pool.

Portfolio management strategies must match both the comfort level and the real financial buffer of the investor. Confusing risk preference with risk capacity is one of the most common mistakes in portfolio construction.

A fund manager's first task is to separate the two and build accordingly.

Do You Have the Time and Expertise to Monitor Your Portfolio?

Active investment portfolio strategies require regular market attention weekly at minimum. If that commitment is not realistic, professional management through a SEBI-registered PMS provider is the practical answer.

It places monitoring responsibility with a dedicated fund manager and removes emotion-driven decisions during market corrections. The right strategy is the one that gets executed consistently over years not just the one that sounds best in a good market.

Choosing well and maintaining discipline are what separate investors who build lasting wealth from those who don't. The next section shows how Ckredence Wealth puts all of this into practice for its clients.

Why Should You Choose Ckredence Wealth for Portfolio Management?

HNIs and UHNIs need portfolio management strategies that go well beyond general advice. Your investment portfolio deserves decisions built on 37 years of market experience, SEBI-regulated expertise, and a research-backed approach to every market cycle.

Solutions That Matter:

Four distinct PMS strategies-All Weather, Diversified, Business Cycle, and ICE Growth-each built for different market conditions and investor goals

SEBI-registered professional management (INP000007164) with transparent, performance-aligned fee structures

Risk-adjusted portfolio construction across equity, debt, and alternative asset classes

Proven Performance in Wealth Management:

₹805+ Crores in AUM managed across 376 active clients

CIO-led investment decisions backed by deep sector research and fundamental analysis

Branch offices in Surat, Mumbai, and Vadodara for direct, relationship-based advisory

Every portfolio management strategy at Ckredence Wealth is matched to the individual investor's financial profile, risk capacity, and long-term goals from first-time PMS clients to multi-generational family offices. Your wealth deserves that level of attention.

Ready to build a portfolio strategy that works through every market cycle? Schedule a Consultation with Ckredence Wealth.

Conclusion

Portfolio management strategies are not interchangeable products they are structured approaches matched to specific investor goals, risk profiles, and time horizons.

Active and growth-oriented strategies serve investors seeking market-beating returns with professional oversight.

Conservative and income-oriented strategies protect capital and generate steady returns for risk-aware investors.

Process components-asset allocation, diversification, rebalancing, and tax efficienc-drive long-term outcomes more than strategy selection alone.

Professional PMS management through a SEBI-registered firm gives HNIs access to institutional-grade portfolio construction without the burden of daily monitoring.

A strong investment portfolio is not built in a single decision. It is built through a disciplined strategy, executed consistently, reviewed regularly, and adjusted with clear purpose.

FAQs

Q1: What is the best portfolio management strategy for long-term wealth creation?

The best portfolio management strategy for long-term wealth creation among HNIs is Active management with strategic asset allocation. A SEBI-registered PMS provider builds a strategy around your specific financial goals. The best approach depends on your time horizon and comfort with market volatility.

Q2: What is the difference between active and passive portfolio management strategies?

Active portfolio management involves fund managers making regular decisions to outperform a benchmark index. Passive management tracks an index like the Nifty 50 with minimal trading and lower costs. Active management suits investors with specific goals that a passive product cannot address.

Q3: What is the 70:20:10 rule in investment portfolio management? The 70:20:10 rule in investment portfolio management is to divides a portfolio into three risk tiers: low, medium, and high risk. It helps investors distribute capital across asset classes in a disciplined, structured way. The exact split adjusts based on individual risk tolerance, goals, and market conditions.

Q4: How often should you rebalance your investment portfolio? Portfolio rebalancing should happen at least once a year or when allocation drifts notably from the original target. Market movements can shift your equity-debt ratio beyond your intended risk level. Regular rebalancing keeps portfolio management strategies aligned with your long-term financial plan.