6 min read

6 min read

Investment Planning Services for HNIs in India: A Complete 2026 Guide

Investment Planning Services for HNIs in India: A Complete 2026 Guide

Investment Planning Services for HNIs in India: A Complete 2026 Guide

HNI investment planning in India covers PMS, AIFs, tax optimisation, and succession planning. Learn the core services, asset allocation, and wealth management process for 2026.

HNI investment planning in India covers PMS, AIFs, tax optimisation, and succession planning. Learn the core services, asset allocation, and wealth management process for 2026.

HNI investment planning in India covers PMS, AIFs, tax optimisation, and succession planning. Learn the core services, asset allocation, and wealth management process for 2026.

Ckredenced Wealth

Ckredenced Wealth

|

Introduction

Investment planning services for High Net Worth Individuals (HNIs) in India focus on tailored strategies to preserve and grow wealth, featuring customised portfolios, tax optimisation, and access to exclusive products like Alternative Investment Funds (AIFs) and Portfolio Management Services (PMS).

These services are designed to protect wealth, enhance returns via exclusive opportunities, and manage complex, multi-generational financial goals.

India's HNI population has crossed 850,000 individuals with assets above USD 1 million and is set to nearly double to 1.65 million by 2027, while the UHNI population grew 6% annually to 13,600 in 2024 and is projected to increase by 50% by 2028, according to Waterfield Advisors.

A Deloitte India report from January 2025 estimates a USD 1.6 trillion AUM growth opportunity for wealth management providers between FY24 and FY29, with demand expected to nearly double from USD 1.1 trillion to USD 2.3 trillion.

Yet a significant portion of this wealth remains self-managed or informally managed, leaving meaningful value on the table.

Do you know which investment products are exclusively available to HNIs in India and how they differ from retail options?

Are you clear on how a professional wealth management process works, from assessment to rebalancing?

Do you understand how tax optimisation, estate planning, and global diversification fit into a complete HNI investment strategy?

This guide breaks down every aspect of HNI investment planning in India for 2026, from core services and asset allocation to wealth management firms and key considerations.

Key Takeaways

HNI investment planning goes beyond mutual funds, including PMS, AIFs, global equity, structured debt, and estate planning

A typical allocation includes 40–50% equities, 20–30% debt, 10–20% alternatives, and 5–10% gold or commodities

PMS requires a minimum investment of ₹50 lakh, while Category II and III AIFs need at least ₹1 crore per investor

Tax optimisation, succession planning, and global diversification are key pillars of HNI wealth strategies

Active management and dedicated relationship managers are important for handling complex, multi-asset portfolios

What Is HNI Investment Planning in India?

HNI investment planning in India is a customised financial strategy designed for individuals with substantial investable surplus, typically ₹5 crore and above.

Unlike retail investors who primarily rely on mutual funds and fixed deposits, HNIs focus on capital preservation, consistent long-term growth, tax optimisation, and legacy planning across multiple asset classes.

This goes beyond basic products. A complete HNI investment plan in India includes direct equity management through PMS, access to private markets via AIFs, global exposure through international funds and ETFs, structured debt instruments, and estate planning structures like trusts and wills.

Wealth management for HNIs in India is about strategy and structure, not just product selection.

Core Services for Indian HNIs

HNI investment planning covers a range of specialised services that are either unavailable to or unsuitable for retail investors. Here are the six core services that form the foundation of a complete HNI wealth plan:

Customised Portfolio Management (PMS): Professional, active management of a direct equity portfolio built specifically for the investor's goals, risk profile, and market outlook.

SEBI-regulated PMS requires a minimum investment of ₹50 lakhs with each security held directly in the investor's Demat account, offering full transparency and personalised strategy.

Learn about Ckredence Wealth's PMS investment approaches across four strategies built for different market conditions

Alternative Investment Funds (AIFs): Access to private equity, venture capital, real estate funds, and structured credit opportunities that provide diversification beyond public markets.

Category II AIFs are the most common vehicle for HNI investors seeking private market exposure. Minimum investment is ₹1 crore per investor. For a detailed comparison, read our guide on PMS vs AIF

Tax Planning and Optimisation: Proactive tax-saving strategies including tax-loss harvesting, capital gains management, strategic profit booking, and using investment structures that maximise post-tax returns.

Every investment decision at the HNI level must account for tax implications, particularly for investors in the 30% tax bracket. For a full breakdown, read our guide on taxation on mutual funds and PMS

Succession and Estate Planning: Ensuring seamless wealth transfer to future generations through trust creation, estate structuring, wills, and family governance frameworks.

This is particularly critical for first-generation entrepreneurs and business families managing multi-generational wealth

Global Diversification and NRI Services: Options for international investments including foreign equity funds, US market ETFs, and feeder funds, along with tailored services for Non-Resident Indians managing cross-border portfolios within FEMA and SEBI guidelines.

Our dedicated NRI desk provides specialised guidance for NRI investors

Risk Management: Identifying potential financial threats including market concentration risk, liquidity risk, currency risk, and economic shocks, and recommending insurance, diversification strategies, and hedging approaches to safeguard the client's asset base

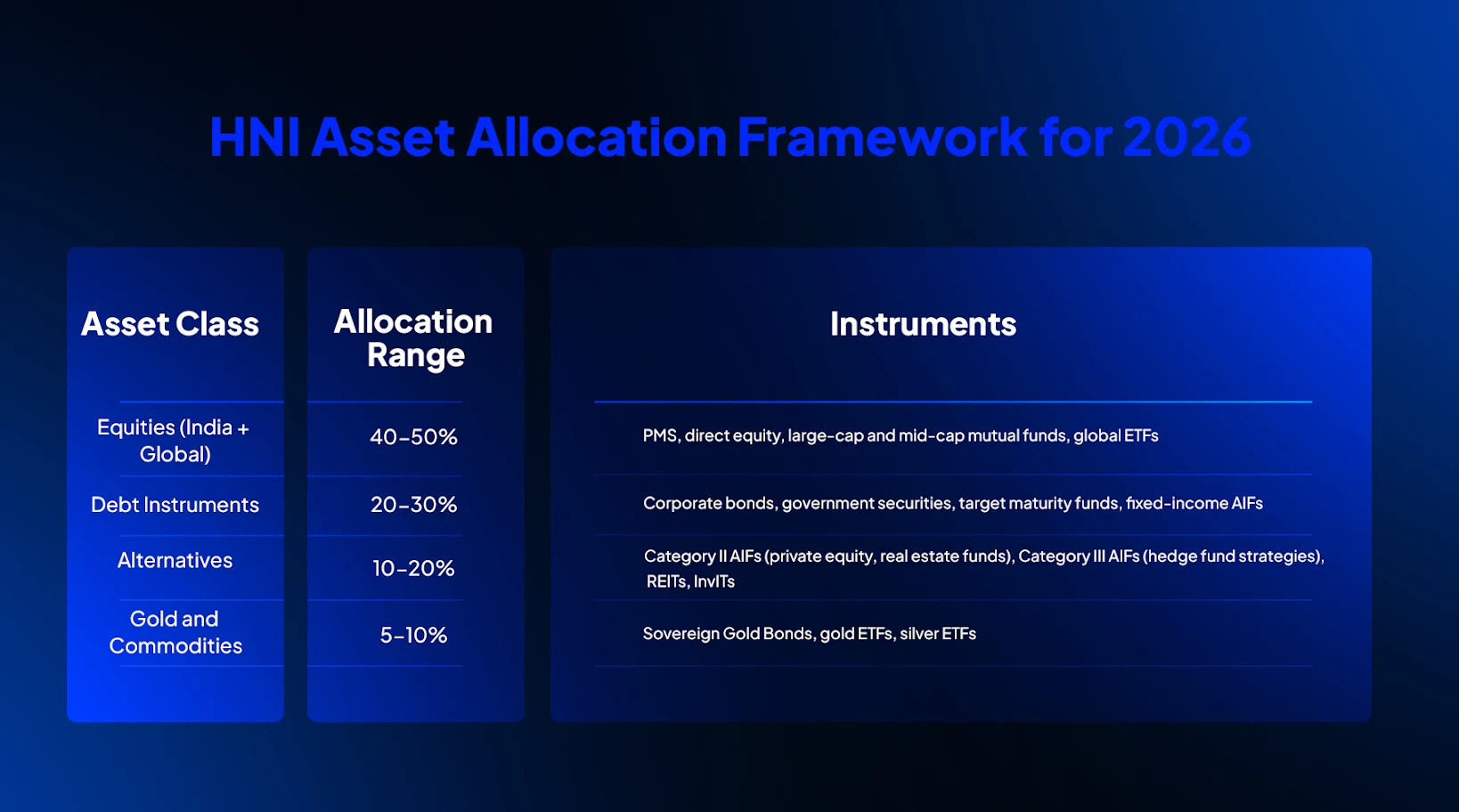

HNI Asset Allocation Framework for 2026

A well-structured HNI portfolio in India balances growth, stability, and diversification across multiple asset classes. Here is the standard allocation framework used by professional wealth managers for HNI clients in 2026:

This allocation provides a balance of long-term capital appreciation through equities, portfolio stability through debt, higher-return potential through alternatives, and inflation protection through gold and commodities.

The exact split is personalised based on the investor's age, liquidity needs, risk tolerance, and tax position.

Wealth Management Process for HNIs

Professional HNI wealth management in India follows a structured, repeatable process that evolves with the client's financial life:

Assessment: A thorough review of current financial position, income sources, existing investments, liabilities, risk appetite, and short, medium, and long-term goals.

This forms the foundation of every investment decision going forward

Asset Allocation: Designing a personalised multi-asset portfolio based on the assessment.

For HNIs, this goes beyond the standard equity-debt split to include alternatives, global exposure, and tax-efficient instruments aligned with the client's specific objectives

Execution and Tracking: Coordinating investments across multiple asset classes and product types, setting up portfolio accounts, completing onboarding across PMS or AIF structures, and providing regular performance reporting with complete transparency on every holding and transaction

Review and Rebalancing: Regular monitoring and rebalancing of the portfolio to align with changing market conditions, evolving financial goals, and tax optimisation opportunities.

For active HNI portfolios, quarterly reviews are the minimum standard

Top HNI Wealth Management Firms in India

HNI investors in India typically choose between institutional private bankers, specialised wealth boutiques, and SEBI-registered investment advisors (RIAs) based on their need for bespoke, fee-based advisory.

Firm | Specialisation |

Dezerv | Tech-enabled portfolio tracking and active management |

WealthMunshi | Tailored comprehensive wealth management and succession planning |

Waterfield Advisors | Fee-based, transparent holistic wealth advisory for UHNIs |

Anand Rathi Wealth | Personalised investment and insurance planning |

Ckredence Wealth | SEBI-registered PMS and RIA advisory for HNIs with ₹50L+ corpus |

At Ckredence Wealth, we offer both SEBI-registered PMS and RIA services under one roof, with 37 years of wealth management experience and ₹805+ crores in AUM across 376+ active clients. Visit our RIA advisory page for goal-based, conflict-free financial planning.

Key Considerations for HNI Investing in 2026

The investment environment in 2026 presents specific opportunities and risks that HNI investors must account for in their planning:

Active Management: Despite a record bull run from 2020 to 2024, 40% of HNI respondents expressed dissatisfaction with their investment returns, according to the Marcellus India Wealth Survey 2025, underscoring the gap between wealth accumulation and strategic wealth management.

HNIs need proactive portfolio management, not passive tracking. Due to the complexity of multi-asset portfolios and limited time, most HNIs benefit significantly from dedicated professional management

Risk Management: With global geopolitical uncertainty, currency volatility, and potential rate changes in FY27, protecting wealth against market volatility requires deliberate diversification across asset classes, geographies, and time horizons.

A concentrated portfolio in a single asset class or sector is one of the most common and costly mistakes HNI investors make

Digital Integration: Modern wealth management firms utilise AI-powered analytics, real-time portfolio reporting apps, and digital dashboards to keep HNI clients fully informed about every aspect of their portfolio.

Technology-driven transparency is now a baseline expectation, not a differentiator

Succession Planning: With 20% of millionaires in India now under 40 and wealth increasingly spreading to Tier-II and Tier-III cities, according to Waterfield Advisors, timely succession planning and estate structuring are more important than ever.

Delaying this planning is one of the most significant risks to long-term family wealth preservation

Why Should You Choose Ckredence Wealth for HNI Investment Planning?

At Ckredence Wealth, we bring 37 years of HNI wealth management experience to every client relationship, with SEBI-registered services across both PMS and investment advisory.

What We Offer:

Four active PMS strategies — All Weather, Diversified, Business Cycle, and ICE Growth — for investors with ₹50 lakhs or more, with direct equity ownership and full portfolio transparency

SEBI-registered RIA services for comprehensive financial planning covering tax optimisation, goal-based allocation, and estate planning

₹805+ Crores in AUM managed across 376+ active clients in Gujarat and Maharashtra

Dedicated relationship managers, quarterly portfolio reviews, and personalised onboarding via our direct PMS onboarding process

Offices in Surat, Mumbai, and Vadodara with transparent, conflict-free fee structures

Ready to build a structured, tax-efficient HNI investment plan for 2026? Schedule a consultation with our team.

Conclusion

HNI investment planning in India in 2026 demands a fundamentally different approach from retail investing. It requires customised asset allocation across equities, debt, alternatives, and global instruments, combined with active tax planning, estate structuring, and risk management. The HNIs who build lasting wealth are not those who chase the highest returns but those who build a resilient, professionally managed strategy that works across market cycles and evolves with their financial life.

The rapid growth of India's HNI and UHNI population, combined with the expansion of product options through PMS and AIFs, means the gap between informed and uninformed investors is widening. Choosing the right wealth management partner, one who operates on a transparent, fee-based model with genuine fiduciary commitment, is the single most important investment decision an HNI can make.

Investments are subject to market risks. Please read all scheme-related documents carefully before investing. Past performance is not indicative of future returns.

FAQs

What are the best investment options for HNIs in India in 2026?

The best investment options for HNIs in India include PMS for direct equity management, Category II and III AIFs for private market exposure, Sovereign Gold Bonds for inflation hedging, global equity funds for international diversification, and structured debt instruments for portfolio stability. The right mix depends on the investor's corpus size, risk profile, and time horizon.

What is the minimum investment for PMS and AIFs in India?

PMS requires a minimum investment of ₹50 lakhs per SEBI regulations, with securities held directly in the investor's Demat account. Category I, II, and III AIFs require a minimum of ₹1 crore per investor, making both categories exclusively suited for HNIs and institutional investors.

Why do HNIs need a different investment strategy from retail investors?

HNIs have different needs including capital preservation across generations, complex tax situations, succession planning requirements, and access to exclusive investment products not available to retail investors. Their portfolio complexity and scale require active professional management, not passive index-based strategies.

How do I verify a wealth manager's credentials before investing as an HNI?

Always confirm that the wealth manager holds SEBI registration as a Portfolio Manager under PM Regulations 2020 or as a Registered Investment Adviser under IA Regulations 2013. Verify their registration number on the SEBI Intermediaries portal, review their fee structure for any conflicts of interest, and check their track record and client testimonials before committing capital.

Introduction

Investment planning services for High Net Worth Individuals (HNIs) in India focus on tailored strategies to preserve and grow wealth, featuring customised portfolios, tax optimisation, and access to exclusive products like Alternative Investment Funds (AIFs) and Portfolio Management Services (PMS).

These services are designed to protect wealth, enhance returns via exclusive opportunities, and manage complex, multi-generational financial goals.

India's HNI population has crossed 850,000 individuals with assets above USD 1 million and is set to nearly double to 1.65 million by 2027, while the UHNI population grew 6% annually to 13,600 in 2024 and is projected to increase by 50% by 2028, according to Waterfield Advisors.

A Deloitte India report from January 2025 estimates a USD 1.6 trillion AUM growth opportunity for wealth management providers between FY24 and FY29, with demand expected to nearly double from USD 1.1 trillion to USD 2.3 trillion.

Yet a significant portion of this wealth remains self-managed or informally managed, leaving meaningful value on the table.

Do you know which investment products are exclusively available to HNIs in India and how they differ from retail options?

Are you clear on how a professional wealth management process works, from assessment to rebalancing?

Do you understand how tax optimisation, estate planning, and global diversification fit into a complete HNI investment strategy?

This guide breaks down every aspect of HNI investment planning in India for 2026, from core services and asset allocation to wealth management firms and key considerations.

Key Takeaways

HNI investment planning goes beyond mutual funds, including PMS, AIFs, global equity, structured debt, and estate planning

A typical allocation includes 40–50% equities, 20–30% debt, 10–20% alternatives, and 5–10% gold or commodities

PMS requires a minimum investment of ₹50 lakh, while Category II and III AIFs need at least ₹1 crore per investor

Tax optimisation, succession planning, and global diversification are key pillars of HNI wealth strategies

Active management and dedicated relationship managers are important for handling complex, multi-asset portfolios

What Is HNI Investment Planning in India?

HNI investment planning in India is a customised financial strategy designed for individuals with substantial investable surplus, typically ₹5 crore and above.

Unlike retail investors who primarily rely on mutual funds and fixed deposits, HNIs focus on capital preservation, consistent long-term growth, tax optimisation, and legacy planning across multiple asset classes.

This goes beyond basic products. A complete HNI investment plan in India includes direct equity management through PMS, access to private markets via AIFs, global exposure through international funds and ETFs, structured debt instruments, and estate planning structures like trusts and wills.

Wealth management for HNIs in India is about strategy and structure, not just product selection.

Core Services for Indian HNIs

HNI investment planning covers a range of specialised services that are either unavailable to or unsuitable for retail investors. Here are the six core services that form the foundation of a complete HNI wealth plan:

Customised Portfolio Management (PMS): Professional, active management of a direct equity portfolio built specifically for the investor's goals, risk profile, and market outlook.

SEBI-regulated PMS requires a minimum investment of ₹50 lakhs with each security held directly in the investor's Demat account, offering full transparency and personalised strategy.

Learn about Ckredence Wealth's PMS investment approaches across four strategies built for different market conditions

Alternative Investment Funds (AIFs): Access to private equity, venture capital, real estate funds, and structured credit opportunities that provide diversification beyond public markets.

Category II AIFs are the most common vehicle for HNI investors seeking private market exposure. Minimum investment is ₹1 crore per investor. For a detailed comparison, read our guide on PMS vs AIF

Tax Planning and Optimisation: Proactive tax-saving strategies including tax-loss harvesting, capital gains management, strategic profit booking, and using investment structures that maximise post-tax returns.

Every investment decision at the HNI level must account for tax implications, particularly for investors in the 30% tax bracket. For a full breakdown, read our guide on taxation on mutual funds and PMS

Succession and Estate Planning: Ensuring seamless wealth transfer to future generations through trust creation, estate structuring, wills, and family governance frameworks.

This is particularly critical for first-generation entrepreneurs and business families managing multi-generational wealth

Global Diversification and NRI Services: Options for international investments including foreign equity funds, US market ETFs, and feeder funds, along with tailored services for Non-Resident Indians managing cross-border portfolios within FEMA and SEBI guidelines.

Our dedicated NRI desk provides specialised guidance for NRI investors

Risk Management: Identifying potential financial threats including market concentration risk, liquidity risk, currency risk, and economic shocks, and recommending insurance, diversification strategies, and hedging approaches to safeguard the client's asset base

HNI Asset Allocation Framework for 2026

A well-structured HNI portfolio in India balances growth, stability, and diversification across multiple asset classes. Here is the standard allocation framework used by professional wealth managers for HNI clients in 2026:

This allocation provides a balance of long-term capital appreciation through equities, portfolio stability through debt, higher-return potential through alternatives, and inflation protection through gold and commodities.

The exact split is personalised based on the investor's age, liquidity needs, risk tolerance, and tax position.

Wealth Management Process for HNIs

Professional HNI wealth management in India follows a structured, repeatable process that evolves with the client's financial life:

Assessment: A thorough review of current financial position, income sources, existing investments, liabilities, risk appetite, and short, medium, and long-term goals.

This forms the foundation of every investment decision going forward

Asset Allocation: Designing a personalised multi-asset portfolio based on the assessment.

For HNIs, this goes beyond the standard equity-debt split to include alternatives, global exposure, and tax-efficient instruments aligned with the client's specific objectives

Execution and Tracking: Coordinating investments across multiple asset classes and product types, setting up portfolio accounts, completing onboarding across PMS or AIF structures, and providing regular performance reporting with complete transparency on every holding and transaction

Review and Rebalancing: Regular monitoring and rebalancing of the portfolio to align with changing market conditions, evolving financial goals, and tax optimisation opportunities.

For active HNI portfolios, quarterly reviews are the minimum standard

Top HNI Wealth Management Firms in India

HNI investors in India typically choose between institutional private bankers, specialised wealth boutiques, and SEBI-registered investment advisors (RIAs) based on their need for bespoke, fee-based advisory.

Firm | Specialisation |

Dezerv | Tech-enabled portfolio tracking and active management |

WealthMunshi | Tailored comprehensive wealth management and succession planning |

Waterfield Advisors | Fee-based, transparent holistic wealth advisory for UHNIs |

Anand Rathi Wealth | Personalised investment and insurance planning |

Ckredence Wealth | SEBI-registered PMS and RIA advisory for HNIs with ₹50L+ corpus |

At Ckredence Wealth, we offer both SEBI-registered PMS and RIA services under one roof, with 37 years of wealth management experience and ₹805+ crores in AUM across 376+ active clients. Visit our RIA advisory page for goal-based, conflict-free financial planning.

Key Considerations for HNI Investing in 2026

The investment environment in 2026 presents specific opportunities and risks that HNI investors must account for in their planning:

Active Management: Despite a record bull run from 2020 to 2024, 40% of HNI respondents expressed dissatisfaction with their investment returns, according to the Marcellus India Wealth Survey 2025, underscoring the gap between wealth accumulation and strategic wealth management.

HNIs need proactive portfolio management, not passive tracking. Due to the complexity of multi-asset portfolios and limited time, most HNIs benefit significantly from dedicated professional management

Risk Management: With global geopolitical uncertainty, currency volatility, and potential rate changes in FY27, protecting wealth against market volatility requires deliberate diversification across asset classes, geographies, and time horizons.

A concentrated portfolio in a single asset class or sector is one of the most common and costly mistakes HNI investors make

Digital Integration: Modern wealth management firms utilise AI-powered analytics, real-time portfolio reporting apps, and digital dashboards to keep HNI clients fully informed about every aspect of their portfolio.

Technology-driven transparency is now a baseline expectation, not a differentiator

Succession Planning: With 20% of millionaires in India now under 40 and wealth increasingly spreading to Tier-II and Tier-III cities, according to Waterfield Advisors, timely succession planning and estate structuring are more important than ever.

Delaying this planning is one of the most significant risks to long-term family wealth preservation

Why Should You Choose Ckredence Wealth for HNI Investment Planning?

At Ckredence Wealth, we bring 37 years of HNI wealth management experience to every client relationship, with SEBI-registered services across both PMS and investment advisory.

What We Offer:

Four active PMS strategies — All Weather, Diversified, Business Cycle, and ICE Growth — for investors with ₹50 lakhs or more, with direct equity ownership and full portfolio transparency

SEBI-registered RIA services for comprehensive financial planning covering tax optimisation, goal-based allocation, and estate planning

₹805+ Crores in AUM managed across 376+ active clients in Gujarat and Maharashtra

Dedicated relationship managers, quarterly portfolio reviews, and personalised onboarding via our direct PMS onboarding process

Offices in Surat, Mumbai, and Vadodara with transparent, conflict-free fee structures

Ready to build a structured, tax-efficient HNI investment plan for 2026? Schedule a consultation with our team.

Conclusion

HNI investment planning in India in 2026 demands a fundamentally different approach from retail investing. It requires customised asset allocation across equities, debt, alternatives, and global instruments, combined with active tax planning, estate structuring, and risk management. The HNIs who build lasting wealth are not those who chase the highest returns but those who build a resilient, professionally managed strategy that works across market cycles and evolves with their financial life.

The rapid growth of India's HNI and UHNI population, combined with the expansion of product options through PMS and AIFs, means the gap between informed and uninformed investors is widening. Choosing the right wealth management partner, one who operates on a transparent, fee-based model with genuine fiduciary commitment, is the single most important investment decision an HNI can make.

Investments are subject to market risks. Please read all scheme-related documents carefully before investing. Past performance is not indicative of future returns.

FAQs

What are the best investment options for HNIs in India in 2026?

The best investment options for HNIs in India include PMS for direct equity management, Category II and III AIFs for private market exposure, Sovereign Gold Bonds for inflation hedging, global equity funds for international diversification, and structured debt instruments for portfolio stability. The right mix depends on the investor's corpus size, risk profile, and time horizon.

What is the minimum investment for PMS and AIFs in India?

PMS requires a minimum investment of ₹50 lakhs per SEBI regulations, with securities held directly in the investor's Demat account. Category I, II, and III AIFs require a minimum of ₹1 crore per investor, making both categories exclusively suited for HNIs and institutional investors.

Why do HNIs need a different investment strategy from retail investors?

HNIs have different needs including capital preservation across generations, complex tax situations, succession planning requirements, and access to exclusive investment products not available to retail investors. Their portfolio complexity and scale require active professional management, not passive index-based strategies.

How do I verify a wealth manager's credentials before investing as an HNI?

Always confirm that the wealth manager holds SEBI registration as a Portfolio Manager under PM Regulations 2020 or as a Registered Investment Adviser under IA Regulations 2013. Verify their registration number on the SEBI Intermediaries portal, review their fee structure for any conflicts of interest, and check their track record and client testimonials before committing capital.