11min Read

11min Read

Best Investment After 80C: Goal-Based Options to Build Wealth in 2026

Best Investment After 80C: Goal-Based Options to Build Wealth in 2026

Best Investment After 80C: Goal-Based Options to Build Wealth in 2026

Exhausted your Section 80C tax limit? Know the best investment options for wealth creation, capital safety, and retirement planning in India.

Exhausted your Section 80C tax limit? Know the best investment options for wealth creation, capital safety, and retirement planning in India.

Exhausted your Section 80C tax limit? Know the best investment options for wealth creation, capital safety, and retirement planning in India.

Ckredence Wealth

Ckredence Wealth

|

India's Section 80C of the Income Tax Act, 1961 allows a maximum tax deduction of Rs.1.5 lakh per financial year. For salaried professionals, this limit fills up before any active investment decision is made. Employee Provident Fund (EPF) contributions, home loan principal repayments, and life insurance premiums consume a large portion automatically. According to the Income Tax Department of India, over 8.09 crore ITR filings were recorded in FY2023-24, with the majority of salaried taxpayers exhausting their 80C ceiling before they allocate a single rupee toward wealth creation through mutual fund advisory or other active investment instruments.

If your Rs.1.5 lakh 80C limit is already filled, which investment will actually grow your wealth and still reduce your tax liability?

Are you leaving Rs.50,000 of additional tax deduction unused every year because you are not aware that Section 80CCD(1B) exists?

With equity markets, gold, fixed income, and retirement instruments all competing for your surplus, how do you decide what belongs in your portfolio after 80C?

The good news is that exhausting 80C is not the end of tax-efficient investing. It is the beginning of a more purposeful investment plan. This article examines each post-80C option in depth, organized by your financial goal, so you can pick what fits your situation rather than what is most marketed.

KEY STAT |

Section 80C gives a deduction of Rs.1.5 lakh. Add NPS under Section 80CCD(1B) and you unlock an extra Rs.50,000. That brings your total deduction to Rs.2 lakh per year, before health insurance, home loan interest, or education loan benefits even enter the picture. Most taxpayers only use the first half. |

Source: Income Tax Act, 1961, Chapter VI-A | NPS Trust |

TL;DR

NPS contributions under Section 80CCD(1B) give you an additional Rs.50,000 deduction, independent of 80C, making it the most direct tax-saving move after 80C

ELSS can be invested beyond the Rs.1.5 lakh 80C cap; the surplus amount grows in the same portfolio with the same 3-year lock-in

Sovereign Gold Bonds (SGBs) are the most tax-efficient gold investment; capital gains at maturity are fully tax-free, and they earn 2.5% annual interest on top

Combining 80C, NPS, Section 80D, and Section 24(b) can produce total annual deductions exceeding Rs.4.5 lakh for eligible taxpayers

Arbitrage mutual funds are classified as equity funds for tax purposes; for investors in the 30% slab, they offer better post-tax returns than bank FDs for 1-year holdings

Voluntary Provident Fund (VPF) interest grows entirely tax-free; salaried professionals with EPF accounts can increase contributions beyond the mandatory 12%

The best investment after 80C is not one product; it is a goal-matched combination of equity, fixed income, gold, and deduction-linked instruments

Table 1: Post-80C Investment Options at a Glance

Investment Option | Est. Returns | Risk | Tax Advantage | Lock-in | Best For |

NPS Tier-1 (80CCD 1B) | 10-12% CAGR | Medium | Rs.50,000 extra deduction | Till age 60 | 30-50 yr professionals |

ELSS beyond 80C cap | 12-15% CAGR | High | None on excess amount | 3 yrs/SIP | Equity, 5+ yr horizon |

Voluntary Provident Fund | 8.25% p.a. | Very Low | Tax-free growth | 5 years | Salaried, capital safety |

Sovereign Gold Bonds | 8-10%+ gold | Low | Tax-free at maturity | 8 years | Gold exposure seekers |

Arbitrage Mutual Funds | 6.5-7.5% | Very Low | 12.5% LTCG after 1 yr | None | 1-2 yr surplus parking |

Liquid / UST Debt Funds | 6-7% p.a. | Very Low | Taxed at slab rate | None | Emergency buffer, <1 yr |

Section 80D Premium | N/A | N/A | Up to Rs.1L deduction | Annual | Health insurance holders |

What Happens After You Exhaust Your Rs.1.5 Lakh 80C Limit?

Exhausting the 80C limit does not mean you have run out of ways to save tax or build wealth. Section 80C is just one provision under Chapter VI-A of the Income Tax Act, 1961. There are other provisions and investment instruments that operate completely outside this ceiling and work independently of it.

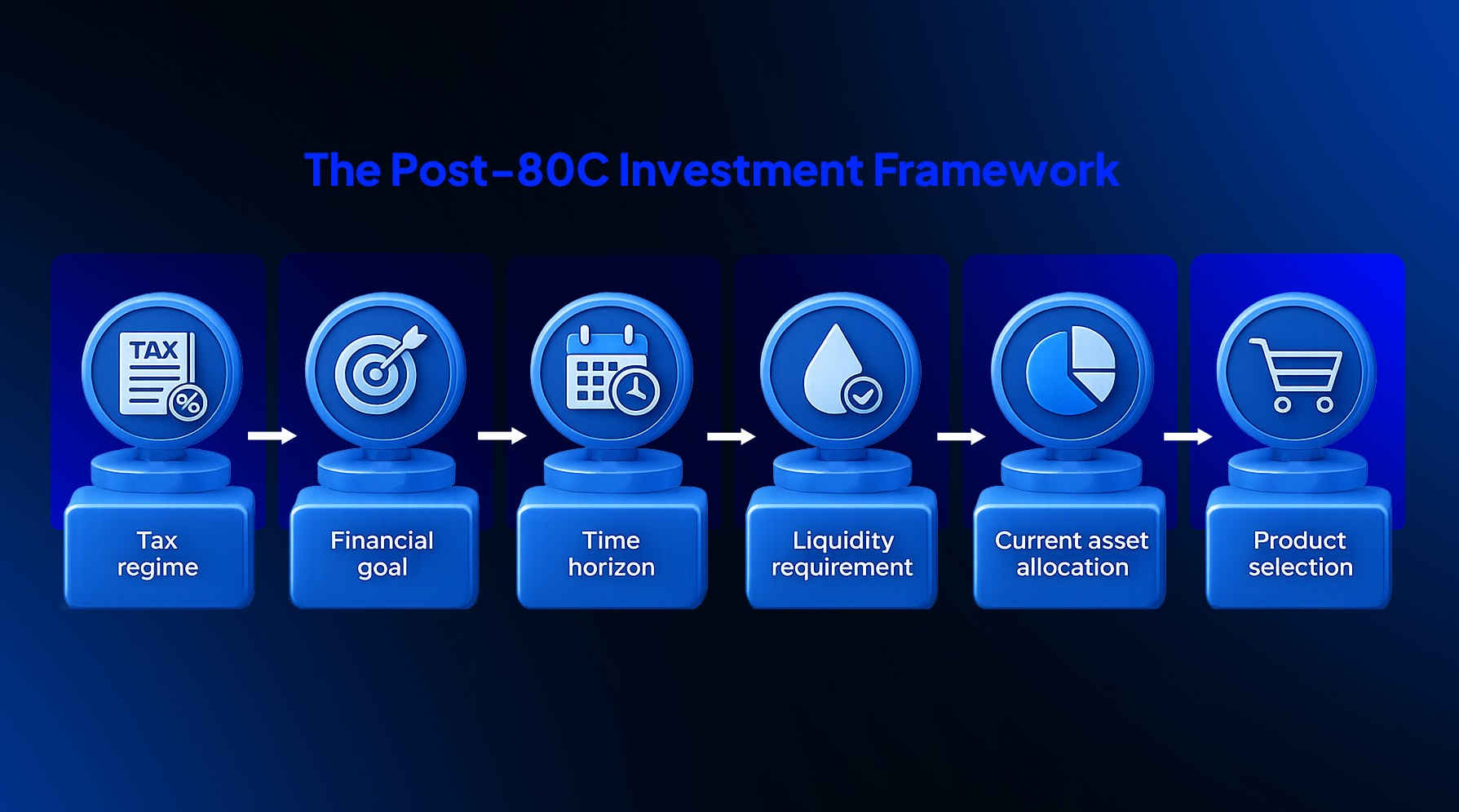

The key to making the right decision is goal alignment. Your post-80C decisions are fundamentally about asset allocation — matching the right instrument to your financial goal, investment horizon, and risk tolerance.

The five goal-based categories for the best investment after 80C are:

High Returns and Wealth Creation — Equity Mutual Funds, ELSS beyond 80C

Fixed, Tax-Free Returns and Capital Safety — VPF/PPF, Sovereign Gold Bonds

Retirement Planning with Extra Tax Deductions — NPS under Section 80CCD(1B)

Short to Medium Term Goals — Arbitrage Funds, Liquid and Ultra-Short Debt Funds

Additional Deduction Avenues — Section 80D, 80E, Section 24(b), 80G

Table 2: Match Your Goal to the Right Post-80C Investment

Your Goal | Best Investment | Horizon | Risk | Tax Benefit |

Extra tax deduction | NPS Tier-1 | Long (till 60) | Medium | Rs.50,000 deduction under 80CCD(1B) |

Wealth creation | ELSS / Flexi-cap MF | 5+ years | High | LTCG at 12.5% above Rs.1.25L threshold |

Capital safety | Voluntary Provident Fund | 5+ years | Very Low | Tax-free growth and full withdrawal |

Gold allocation | Sovereign Gold Bonds | 8 years | Low | Fully tax-free capital gains at maturity |

1-2 yr parking | Arbitrage Mutual Funds | 1-2 years | Very Low | Equity taxation — 12.5% LTCG after 1 yr |

Emergency buffer | Liquid Debt Funds | 3-12 months | Very Low | Taxed at income slab rate, no lock-in |

Health cover + savings | Health Insurance (80D) | Annual | None | Up to Rs.1 lakh deduction — 80D |

The 80C Exhaustion Reality for Salaried Professionals

For a salaried professional earning Rs.10 lakh annually, EPF deductions at 12% of basic salary account for Rs.60,000 to Rs.80,000 per year alone. Add a life insurance premium and home loan principal, and the Rs.1.5 lakh ceiling is breached before any voluntary investment is made. Planning beyond 80C is not optional for anyone earning above Rs.8 lakh in India. It is the natural and necessary next step.

Once the 80C limit is accounted for, the focus shifts to where the real investment opportunity sits. Each of the five categories below addresses a different need.

For High Returns: Best Investment After 80C Through Equity

Equity-based investments offer the strongest long-term wealth creation potential among all post-80C options. After exhausting the 80C limit, two equity routes stand out: diversified Equity Mutual Funds through SIPs, and ELSS funds invested beyond the 80C ceiling.

ELSS (Equity Linked Savings Scheme) qualifies under Section 80C for the first Rs.1.5 lakh you invest. But you can invest more than that ceiling. The portion above Rs.1.5 lakh does not get a deduction, but it grows in the same portfolio with identical market-linked returns. The 3-year lock-in applies per installment, making ELSS one of the more flexible equity options for systematic investing.

The key advantages of equity investments after 80C:

Equity Mutual Funds via SIPs: No lock-in for regular diversified or Flexi-cap funds. Gains above Rs.1.25 lakh per year attract 12.5% Long-Term Capital Gains tax (Union Budget 2024), as amended in Union Budget 2024.

ELSS Beyond the 80C Cap: The fund continues to grow even for the non-deductible portion. Shortest lock-in among all equity instruments at 3 years per installment.

Flexi-cap and Multi-cap Funds: Offer sector-agnostic exposure across large, mid, and small caps, reducing concentration risk over long investment periods.

Who Benefits Most from Equity After 80C

Investors with a 5-year-plus horizon and moderate-to-high risk tolerance benefit most from this route. Younger investors between 28 and 45 in higher tax slabs get the combined benefit of compounding returns and relatively tax-efficient LTCG treatment. For higher-ticket investors managing portfolios above Rs.50 lakh, Portfolio Management Services (PMS) offer a more personalized equity allocation with direct stock ownership and defined strategy mandates, compared to pooled mutual funds.

Equity investments build wealth over time, but not every investor wants to take on market risk with their post-80C surplus. For those who prefer capital safety with tax-free growth, the next category addresses exactly that need.

FOR PORTFOLIOS Rs.50L+ |

Managing surplus beyond mutual funds? Ckredence Wealth PMS delivered consistent alpha across 7 market disruption events. |

+14.58% Alpha over BSE 500 TRI (1-year period ending June 2026) |

Rs.805 Cr+ AUM across 376+ active clients |

37 Years of legacy since 1987 |

SEBI Registered | INP000007164 |

Schedule a Consultation: ckredencewealth.com/contact-us |

For Capital Safety: Tax-Free Returns Beyond Section 80C

Not every investor wants equity exposure after 80C. For those who prioritize capital protection and tax-free growth, two instruments stand out: the Voluntary Provident Fund (VPF) and Sovereign Gold Bonds (SGBs). Both are backed by the Government of India and deliver returns with defined tax advantages.

VPF is an extension of EPF that salaried employees can opt into voluntarily. For investors who have already consumed their 80C ceiling through mandatory EPF, VPF contributions add to their corpus without generating additional tax deductions. But the interest growth on the entire corpus remains tax-free, which is a meaningful advantage for anyone in the 30% bracket.

Voluntary Provident Fund (VPF)

VPF allows salaried individuals to contribute beyond the mandatory 12% EPF contribution, up to 100% of basic salary. The interest rate is set by the government at par with EPF. As per the EPFO circular for FY2024-25, this rate stands at 8.25% per annum. The entire withdrawal, including accumulated interest, is tax-free after 5 years of continuous contribution. No market volatility, no credit risk, and government-backed — VPF is the purest fixed-income instrument for salaried professionals after 80C.

Sovereign Gold Bonds (SGBs)

SGBs are government securities issued by the Reserve Bank of India, denominated in grams of gold. They pay a fixed 2.5% per annum interest semi-annually, on top of which investors get gold price appreciation. The most important tax feature: capital gains on SGBs held until maturity (8 years) are completely tax-free under the Income Tax Act. For investors seeking gold exposure without physical storage costs or making charges, SGBs are the most tax-efficient route available.

VPF and SGBs protect capital while delivering consistent, largely tax-free growth. For investors specifically focused on building a retirement corpus with an additional tax deduction benefit, the next provision is one most salaried professionals overlook.

For Retirement: How NPS Gives You Extra Tax Benefits After 80C

The National Pension System (NPS) offers something unique among all post-80C investment options: an additional tax deduction of Rs.50,000 under Section 80CCD(1B) (NPS Trust). This deduction is entirely separate from the Rs.1.5 lakh Section 80C limit. An investor who uses both provisions can claim a combined deduction of Rs.2 lakh per year.

NPS invests in a mix of equity, corporate bonds, and government securities. Allocation is guided by your age and risk preference through the Auto Choice lifecycle fund or Active Choice mode. The pension corpus at maturity is partially tax-free: 60% can be withdrawn as a lump sum tax-free, while the remaining 40% must be used to buy an annuity.

Key NPS parameters at a glance:

Additional Deduction: Rs.50,000 under Section 80CCD(1B) (NPS Trust), independent of 80C

Asset Allocation: Up to 75% equity under Active Choice for Tier-1 accounts

Withdrawal: 60% lump sum at age 60 (tax-free); 40% mandatory annuity purchase

Employer Contribution: Section 80CCD(2) (Income Tax Department) allows deduction on employer NPS contribution up to 10% of basic salary, with no upper cap

NPS Tier-1 vs Tier-2 Accounts

NPS Tier-1 is the locked pension account where the 80CCD(1B) deduction applies. Tier-2 is a voluntary, flexible account with no lock-in but also no tax deduction. For post-80C tax planning, only Tier-1 contributions under 80CCD(1B) generate the additional benefit. Tier-2 functions more like a short-term investment vehicle.

The Right Investor Profile for NPS

NPS works best for professionals aged 30 to 50 who are actively building a retirement corpus. At the 30% tax slab, the Rs.50,000 annual deduction under Section 80CCD(1B) translates to roughly Rs.15,000 in direct tax savings per year. Over a 25-year investment period, the compounding effect on both the tax saved and the NPS corpus itself is substantial.

NPS solves the retirement and deduction problem simultaneously. For investors with shorter time horizons who need liquidity and better post-tax returns, the next category addresses that need directly.

NPS — THE NUMBERS |

Rs.15,000: Direct tax saved per year at 30% slab via NPS 80CCD(1B) |

Rs.3.75 Lakh: Total tax saved over 25 years (before compounding) |

Rs.50,000: Additional deduction under Section 80CCD(1B), independent of 80C |

That is the impact of the Rs.50,000 NPS deduction alone — before accounting for what the invested corpus compounds to by retirement. |

Source: NPS Trust | Income Tax Department of India |

For Short-to-Medium Term Goals: Smart Parking Options After 80C

If your investment horizon is 1 to 3 years, the earlier categories are too restrictive. For short-to-medium-term goals such as a business expansion, a planned property purchase, or an emergency buffer, there are two specific instruments that deliver better post-tax returns than traditional savings accounts or fixed deposits.

The two most relevant options are Arbitrage Mutual Funds and Liquid or Ultra-Short Term Debt Funds. Both are designed for investors who want to park surplus money productively without committing to long lock-in periods.

The key steps to understanding how each option works:

Arbitrage Mutual Funds: These funds generate returns by exploiting price differences between the cash and derivatives markets. They are classified as equity funds for tax purposes. Understanding how mutual fund and PMS taxation works helps you calculate your actual post-tax returns before committing. Gains held for more than 12 months attract only 12.5% LTCG tax (Finance Act 2024). For investors in the 30% bracket holding for over a year, arbitrage funds are more tax-efficient than most bank fixed deposits.

Liquid and Ultra-Short Term Debt Funds: Best suited for parking money for 3 months to 2 years. These funds invest in high-quality, short-duration debt instruments including commercial paper, treasury bills, and AAA-rated corporate bonds. Returns are stable, typically between 6 to 7% per annum, and are taxed as per the investor's income slab for short-term holdings.

Choosing Between the Two

For holding periods above 1 year, arbitrage funds are typically more tax-efficient due to equity fund classification. For very short durations under 3 months, liquid funds are more predictable and carry lower market-related risk. The choice depends on your withdrawal timeline and tax bracket. Once you have the short-term allocation sorted, the next section addresses provisions that reduce your tax liability without requiring any investment product at all.

Beyond Investments: Additional Tax Deductions After 80C

The best investment after 80C is not always a financial product. Several provisions under the Income Tax Act allow you to claim deductions for expenses you are already incurring. These work independently of Section 80C and can add Rs.1 lakh or more in annual deductions without any new capital outflow.

Most salaried professionals and business owners are not using these sections to their full potential. Together with 80C and NPS, they form a complete tax deduction framework that significantly changes net tax liability.

The key additional deduction avenues beyond 80C:

Section 80D (Income Tax Dept.): Up to Rs.25,000 for health insurance premiums for self and family; Rs.50,000 if any insured member is 60 years or above. An additional Rs.25,000 to Rs.50,000 for parents' health insurance, completely separate from the Rs.25,000 for self.

Section 80E (Income Tax Dept.): Deduction on education loan interest with no upper limit, claimable for up to 8 consecutive years from the year repayment begins.

Section 24(b) (Income Tax Dept.): Up to Rs.2 lakh per year on home loan interest for self-occupied property, one of the largest single deductions available outside 80C.

Section 80G (Income Tax Dept.): Contributions to approved charitable institutions are partially or fully deductible depending on the fund category.

Section 80TTA / 80TTB (Income Tax Dept.): Rs.10,000 deduction on savings account interest for individuals; Rs.50,000 on all deposit interest for senior citizens.

Stacking Deductions: The Full Picture

A salaried investor in the 30% tax bracket who uses 80C (Rs.1.5 lakh), NPS 80CCD(1B) (Rs.50,000), Section 80D (Rs.50,000), and Section 24(b) (Rs.2 lakh) can claim Rs.4.5 lakh in total annual deductions. Add Section 80E for an education loan or 80G for a donation and the total goes higher. For HNIs and senior executives, a structured investment planning approach brings the clarity that individual product decisions alone cannot provide.

Chart 1: How Rs.4.5 Lakh Annual Deduction Breaks Down

Section 80C 33.3% | NPS 80CCD(1B) 11.1% | Section 80D 11.1% | Section 24(b) 44.4% |

Rs.1,50,000 | Rs.50,000 | Rs.50,000 | Rs.2,00,000 |

TOTAL ANNUAL DEDUCTION: Rs.4,50,000 | |||

"A salaried investor who stacks Section 80C, NPS 80CCD(1B), Section 80D, and Section 24(b) can reduce their taxable income by Rs.4.5 lakh or more every year, before a single market return factors in. Most investors know 80C. Almost none are using all four provisions together." |

- Ckredence Wealth Advisory Team | SEBI Registered Portfolio Management | INP000007164 |

Why Should You Choose Ckredence Wealth?

When you have exhausted your 80C limit and are ready to build wealth beyond it, the choices you make next determine how much your money actually grows. At Ckredence Wealth, we work with HNIs, senior executives, and business owners to build investment portfolios that go beyond standard tax-saving instruments.

Solutions that match your profile:

SEBI-registered portfolio management (INP000007164) with 37 years of wealth management experience

4 distinct investment approaches covering All Weather, Diversified, Business Cycle, and ICE Growth for structured equity allocation beyond mutual funds

Our All Weather Investment Approach delivered +14.58% alpha over BSE 500 TRI in the 1-year period ending June 2026, across 7 market disruption events

Rs.805+ Crores managed across 376+ active clients with consistent focus on capital preservation and risk-adjusted returns

Whether you are a first-time PMS investor moving beyond ELSS or an experienced HNI looking to allocate post-80C surplus into active equity strategies, Ckredence Wealth provides research-backed, personalized guidance. Our team, led by CIO Kartik Mehta with 20+ years of equity experience, builds portfolios that work across market cycles.

Ready to make your post-80C investment decisions count? Schedule a Consultation with Ckredence Wealth.

Conclusion

When your Section 80C limit is exhausted, the investment decisions you make next define your actual wealth trajectory. NPS delivers an extra Rs.50,000 deduction that most salaried professionals leave unused every year. Equity mutual funds and ELSS drive long-term portfolio growth through compounding, while VPF and Sovereign Gold Bonds protect capital with tax-free returns. For short-term surplus, arbitrage and liquid funds beat bank fixed deposits on a post-tax basis for investors in the 30% bracket.

Beyond investment products, Sections 80D, 80E, and 24(b) reduce your taxable income without any new capital commitment. Combining all four deduction provisions can bring total annual tax savings to Rs.4.5 lakh or more. The best post-80C approach is not one product but a goal-matched combination built around your income, risk profile, and investment horizon. For investors with surplus above Rs.50 lakh, working with a SEBI-registered portfolio manager brings the structure and active oversight that index-based instruments cannot provide.

FAQs

01.

What is the best investment after 80C for tax saving?

NPS under Section 80CCD(1B) is the most direct answer — it gives an additional Rs.50,000 deduction independent of the 80C ceiling. For wealth creation alongside tax saving, equity mutual funds and ELSS are the most widely used options after 80C.

02.

Q: Can I invest in ELSS beyond the Rs.1.5 lakh 80C limit?

Yes, ELSS investments above Rs.1.5 lakh do not qualify for the Section 80C deduction. The surplus amount still grows in the same fund with the same 3-year lock-in and market-linked returns.

03.

Are Sovereign Gold Bonds tax-free at maturity?

Yes, capital gains on SGBs held until maturity (8 years) are fully tax-free under the Income Tax Act. The 2.5% annual interest paid semi-annually is taxable as per your applicable income slab.

04.

How much total tax deduction can I claim after 80C?

Beyond 80C's Rs.1.5 lakh, you can claim Rs.50,000 via NPS (80CCD 1B), up to Rs.50,000 via health insurance (80D), and Rs.2 lakh via home loan interest (Section 24b). Total annual deductions can reach Rs.4.5 lakh or more depending on individual eligibility.

India's Section 80C of the Income Tax Act, 1961 allows a maximum tax deduction of Rs.1.5 lakh per financial year. For salaried professionals, this limit fills up before any active investment decision is made. Employee Provident Fund (EPF) contributions, home loan principal repayments, and life insurance premiums consume a large portion automatically. According to the Income Tax Department of India, over 8.09 crore ITR filings were recorded in FY2023-24, with the majority of salaried taxpayers exhausting their 80C ceiling before they allocate a single rupee toward wealth creation through mutual fund advisory or other active investment instruments.

If your Rs.1.5 lakh 80C limit is already filled, which investment will actually grow your wealth and still reduce your tax liability?

Are you leaving Rs.50,000 of additional tax deduction unused every year because you are not aware that Section 80CCD(1B) exists?

With equity markets, gold, fixed income, and retirement instruments all competing for your surplus, how do you decide what belongs in your portfolio after 80C?

The good news is that exhausting 80C is not the end of tax-efficient investing. It is the beginning of a more purposeful investment plan. This article examines each post-80C option in depth, organized by your financial goal, so you can pick what fits your situation rather than what is most marketed.

KEY STAT |

Section 80C gives a deduction of Rs.1.5 lakh. Add NPS under Section 80CCD(1B) and you unlock an extra Rs.50,000. That brings your total deduction to Rs.2 lakh per year, before health insurance, home loan interest, or education loan benefits even enter the picture. Most taxpayers only use the first half. |

Source: Income Tax Act, 1961, Chapter VI-A | NPS Trust |

TL;DR

NPS contributions under Section 80CCD(1B) give you an additional Rs.50,000 deduction, independent of 80C, making it the most direct tax-saving move after 80C

ELSS can be invested beyond the Rs.1.5 lakh 80C cap; the surplus amount grows in the same portfolio with the same 3-year lock-in

Sovereign Gold Bonds (SGBs) are the most tax-efficient gold investment; capital gains at maturity are fully tax-free, and they earn 2.5% annual interest on top

Combining 80C, NPS, Section 80D, and Section 24(b) can produce total annual deductions exceeding Rs.4.5 lakh for eligible taxpayers

Arbitrage mutual funds are classified as equity funds for tax purposes; for investors in the 30% slab, they offer better post-tax returns than bank FDs for 1-year holdings

Voluntary Provident Fund (VPF) interest grows entirely tax-free; salaried professionals with EPF accounts can increase contributions beyond the mandatory 12%

The best investment after 80C is not one product; it is a goal-matched combination of equity, fixed income, gold, and deduction-linked instruments

Table 1: Post-80C Investment Options at a Glance

Investment Option | Est. Returns | Risk | Tax Advantage | Lock-in | Best For |

NPS Tier-1 (80CCD 1B) | 10-12% CAGR | Medium | Rs.50,000 extra deduction | Till age 60 | 30-50 yr professionals |

ELSS beyond 80C cap | 12-15% CAGR | High | None on excess amount | 3 yrs/SIP | Equity, 5+ yr horizon |

Voluntary Provident Fund | 8.25% p.a. | Very Low | Tax-free growth | 5 years | Salaried, capital safety |

Sovereign Gold Bonds | 8-10%+ gold | Low | Tax-free at maturity | 8 years | Gold exposure seekers |

Arbitrage Mutual Funds | 6.5-7.5% | Very Low | 12.5% LTCG after 1 yr | None | 1-2 yr surplus parking |

Liquid / UST Debt Funds | 6-7% p.a. | Very Low | Taxed at slab rate | None | Emergency buffer, <1 yr |

Section 80D Premium | N/A | N/A | Up to Rs.1L deduction | Annual | Health insurance holders |

What Happens After You Exhaust Your Rs.1.5 Lakh 80C Limit?

Exhausting the 80C limit does not mean you have run out of ways to save tax or build wealth. Section 80C is just one provision under Chapter VI-A of the Income Tax Act, 1961. There are other provisions and investment instruments that operate completely outside this ceiling and work independently of it.

The key to making the right decision is goal alignment. Your post-80C decisions are fundamentally about asset allocation — matching the right instrument to your financial goal, investment horizon, and risk tolerance.

The five goal-based categories for the best investment after 80C are:

High Returns and Wealth Creation — Equity Mutual Funds, ELSS beyond 80C

Fixed, Tax-Free Returns and Capital Safety — VPF/PPF, Sovereign Gold Bonds

Retirement Planning with Extra Tax Deductions — NPS under Section 80CCD(1B)

Short to Medium Term Goals — Arbitrage Funds, Liquid and Ultra-Short Debt Funds

Additional Deduction Avenues — Section 80D, 80E, Section 24(b), 80G

Table 2: Match Your Goal to the Right Post-80C Investment

Your Goal | Best Investment | Horizon | Risk | Tax Benefit |

Extra tax deduction | NPS Tier-1 | Long (till 60) | Medium | Rs.50,000 deduction under 80CCD(1B) |

Wealth creation | ELSS / Flexi-cap MF | 5+ years | High | LTCG at 12.5% above Rs.1.25L threshold |

Capital safety | Voluntary Provident Fund | 5+ years | Very Low | Tax-free growth and full withdrawal |

Gold allocation | Sovereign Gold Bonds | 8 years | Low | Fully tax-free capital gains at maturity |

1-2 yr parking | Arbitrage Mutual Funds | 1-2 years | Very Low | Equity taxation — 12.5% LTCG after 1 yr |

Emergency buffer | Liquid Debt Funds | 3-12 months | Very Low | Taxed at income slab rate, no lock-in |

Health cover + savings | Health Insurance (80D) | Annual | None | Up to Rs.1 lakh deduction — 80D |

The 80C Exhaustion Reality for Salaried Professionals

For a salaried professional earning Rs.10 lakh annually, EPF deductions at 12% of basic salary account for Rs.60,000 to Rs.80,000 per year alone. Add a life insurance premium and home loan principal, and the Rs.1.5 lakh ceiling is breached before any voluntary investment is made. Planning beyond 80C is not optional for anyone earning above Rs.8 lakh in India. It is the natural and necessary next step.

Once the 80C limit is accounted for, the focus shifts to where the real investment opportunity sits. Each of the five categories below addresses a different need.

For High Returns: Best Investment After 80C Through Equity

Equity-based investments offer the strongest long-term wealth creation potential among all post-80C options. After exhausting the 80C limit, two equity routes stand out: diversified Equity Mutual Funds through SIPs, and ELSS funds invested beyond the 80C ceiling.

ELSS (Equity Linked Savings Scheme) qualifies under Section 80C for the first Rs.1.5 lakh you invest. But you can invest more than that ceiling. The portion above Rs.1.5 lakh does not get a deduction, but it grows in the same portfolio with identical market-linked returns. The 3-year lock-in applies per installment, making ELSS one of the more flexible equity options for systematic investing.

The key advantages of equity investments after 80C:

Equity Mutual Funds via SIPs: No lock-in for regular diversified or Flexi-cap funds. Gains above Rs.1.25 lakh per year attract 12.5% Long-Term Capital Gains tax (Union Budget 2024), as amended in Union Budget 2024.

ELSS Beyond the 80C Cap: The fund continues to grow even for the non-deductible portion. Shortest lock-in among all equity instruments at 3 years per installment.

Flexi-cap and Multi-cap Funds: Offer sector-agnostic exposure across large, mid, and small caps, reducing concentration risk over long investment periods.

Who Benefits Most from Equity After 80C

Investors with a 5-year-plus horizon and moderate-to-high risk tolerance benefit most from this route. Younger investors between 28 and 45 in higher tax slabs get the combined benefit of compounding returns and relatively tax-efficient LTCG treatment. For higher-ticket investors managing portfolios above Rs.50 lakh, Portfolio Management Services (PMS) offer a more personalized equity allocation with direct stock ownership and defined strategy mandates, compared to pooled mutual funds.

Equity investments build wealth over time, but not every investor wants to take on market risk with their post-80C surplus. For those who prefer capital safety with tax-free growth, the next category addresses exactly that need.

FOR PORTFOLIOS Rs.50L+ |

Managing surplus beyond mutual funds? Ckredence Wealth PMS delivered consistent alpha across 7 market disruption events. |

+14.58% Alpha over BSE 500 TRI (1-year period ending June 2026) |

Rs.805 Cr+ AUM across 376+ active clients |

37 Years of legacy since 1987 |

SEBI Registered | INP000007164 |

Schedule a Consultation: ckredencewealth.com/contact-us |

For Capital Safety: Tax-Free Returns Beyond Section 80C

Not every investor wants equity exposure after 80C. For those who prioritize capital protection and tax-free growth, two instruments stand out: the Voluntary Provident Fund (VPF) and Sovereign Gold Bonds (SGBs). Both are backed by the Government of India and deliver returns with defined tax advantages.

VPF is an extension of EPF that salaried employees can opt into voluntarily. For investors who have already consumed their 80C ceiling through mandatory EPF, VPF contributions add to their corpus without generating additional tax deductions. But the interest growth on the entire corpus remains tax-free, which is a meaningful advantage for anyone in the 30% bracket.

Voluntary Provident Fund (VPF)

VPF allows salaried individuals to contribute beyond the mandatory 12% EPF contribution, up to 100% of basic salary. The interest rate is set by the government at par with EPF. As per the EPFO circular for FY2024-25, this rate stands at 8.25% per annum. The entire withdrawal, including accumulated interest, is tax-free after 5 years of continuous contribution. No market volatility, no credit risk, and government-backed — VPF is the purest fixed-income instrument for salaried professionals after 80C.

Sovereign Gold Bonds (SGBs)

SGBs are government securities issued by the Reserve Bank of India, denominated in grams of gold. They pay a fixed 2.5% per annum interest semi-annually, on top of which investors get gold price appreciation. The most important tax feature: capital gains on SGBs held until maturity (8 years) are completely tax-free under the Income Tax Act. For investors seeking gold exposure without physical storage costs or making charges, SGBs are the most tax-efficient route available.

VPF and SGBs protect capital while delivering consistent, largely tax-free growth. For investors specifically focused on building a retirement corpus with an additional tax deduction benefit, the next provision is one most salaried professionals overlook.

For Retirement: How NPS Gives You Extra Tax Benefits After 80C

The National Pension System (NPS) offers something unique among all post-80C investment options: an additional tax deduction of Rs.50,000 under Section 80CCD(1B) (NPS Trust). This deduction is entirely separate from the Rs.1.5 lakh Section 80C limit. An investor who uses both provisions can claim a combined deduction of Rs.2 lakh per year.

NPS invests in a mix of equity, corporate bonds, and government securities. Allocation is guided by your age and risk preference through the Auto Choice lifecycle fund or Active Choice mode. The pension corpus at maturity is partially tax-free: 60% can be withdrawn as a lump sum tax-free, while the remaining 40% must be used to buy an annuity.

Key NPS parameters at a glance:

Additional Deduction: Rs.50,000 under Section 80CCD(1B) (NPS Trust), independent of 80C

Asset Allocation: Up to 75% equity under Active Choice for Tier-1 accounts

Withdrawal: 60% lump sum at age 60 (tax-free); 40% mandatory annuity purchase

Employer Contribution: Section 80CCD(2) (Income Tax Department) allows deduction on employer NPS contribution up to 10% of basic salary, with no upper cap

NPS Tier-1 vs Tier-2 Accounts

NPS Tier-1 is the locked pension account where the 80CCD(1B) deduction applies. Tier-2 is a voluntary, flexible account with no lock-in but also no tax deduction. For post-80C tax planning, only Tier-1 contributions under 80CCD(1B) generate the additional benefit. Tier-2 functions more like a short-term investment vehicle.

The Right Investor Profile for NPS

NPS works best for professionals aged 30 to 50 who are actively building a retirement corpus. At the 30% tax slab, the Rs.50,000 annual deduction under Section 80CCD(1B) translates to roughly Rs.15,000 in direct tax savings per year. Over a 25-year investment period, the compounding effect on both the tax saved and the NPS corpus itself is substantial.

NPS solves the retirement and deduction problem simultaneously. For investors with shorter time horizons who need liquidity and better post-tax returns, the next category addresses that need directly.

NPS — THE NUMBERS |

Rs.15,000: Direct tax saved per year at 30% slab via NPS 80CCD(1B) |

Rs.3.75 Lakh: Total tax saved over 25 years (before compounding) |

Rs.50,000: Additional deduction under Section 80CCD(1B), independent of 80C |

That is the impact of the Rs.50,000 NPS deduction alone — before accounting for what the invested corpus compounds to by retirement. |

Source: NPS Trust | Income Tax Department of India |

For Short-to-Medium Term Goals: Smart Parking Options After 80C

If your investment horizon is 1 to 3 years, the earlier categories are too restrictive. For short-to-medium-term goals such as a business expansion, a planned property purchase, or an emergency buffer, there are two specific instruments that deliver better post-tax returns than traditional savings accounts or fixed deposits.

The two most relevant options are Arbitrage Mutual Funds and Liquid or Ultra-Short Term Debt Funds. Both are designed for investors who want to park surplus money productively without committing to long lock-in periods.

The key steps to understanding how each option works:

Arbitrage Mutual Funds: These funds generate returns by exploiting price differences between the cash and derivatives markets. They are classified as equity funds for tax purposes. Understanding how mutual fund and PMS taxation works helps you calculate your actual post-tax returns before committing. Gains held for more than 12 months attract only 12.5% LTCG tax (Finance Act 2024). For investors in the 30% bracket holding for over a year, arbitrage funds are more tax-efficient than most bank fixed deposits.

Liquid and Ultra-Short Term Debt Funds: Best suited for parking money for 3 months to 2 years. These funds invest in high-quality, short-duration debt instruments including commercial paper, treasury bills, and AAA-rated corporate bonds. Returns are stable, typically between 6 to 7% per annum, and are taxed as per the investor's income slab for short-term holdings.

Choosing Between the Two

For holding periods above 1 year, arbitrage funds are typically more tax-efficient due to equity fund classification. For very short durations under 3 months, liquid funds are more predictable and carry lower market-related risk. The choice depends on your withdrawal timeline and tax bracket. Once you have the short-term allocation sorted, the next section addresses provisions that reduce your tax liability without requiring any investment product at all.

Beyond Investments: Additional Tax Deductions After 80C

The best investment after 80C is not always a financial product. Several provisions under the Income Tax Act allow you to claim deductions for expenses you are already incurring. These work independently of Section 80C and can add Rs.1 lakh or more in annual deductions without any new capital outflow.

Most salaried professionals and business owners are not using these sections to their full potential. Together with 80C and NPS, they form a complete tax deduction framework that significantly changes net tax liability.

The key additional deduction avenues beyond 80C:

Section 80D (Income Tax Dept.): Up to Rs.25,000 for health insurance premiums for self and family; Rs.50,000 if any insured member is 60 years or above. An additional Rs.25,000 to Rs.50,000 for parents' health insurance, completely separate from the Rs.25,000 for self.

Section 80E (Income Tax Dept.): Deduction on education loan interest with no upper limit, claimable for up to 8 consecutive years from the year repayment begins.

Section 24(b) (Income Tax Dept.): Up to Rs.2 lakh per year on home loan interest for self-occupied property, one of the largest single deductions available outside 80C.

Section 80G (Income Tax Dept.): Contributions to approved charitable institutions are partially or fully deductible depending on the fund category.

Section 80TTA / 80TTB (Income Tax Dept.): Rs.10,000 deduction on savings account interest for individuals; Rs.50,000 on all deposit interest for senior citizens.

Stacking Deductions: The Full Picture

A salaried investor in the 30% tax bracket who uses 80C (Rs.1.5 lakh), NPS 80CCD(1B) (Rs.50,000), Section 80D (Rs.50,000), and Section 24(b) (Rs.2 lakh) can claim Rs.4.5 lakh in total annual deductions. Add Section 80E for an education loan or 80G for a donation and the total goes higher. For HNIs and senior executives, a structured investment planning approach brings the clarity that individual product decisions alone cannot provide.

Chart 1: How Rs.4.5 Lakh Annual Deduction Breaks Down

Section 80C 33.3% | NPS 80CCD(1B) 11.1% | Section 80D 11.1% | Section 24(b) 44.4% |

Rs.1,50,000 | Rs.50,000 | Rs.50,000 | Rs.2,00,000 |

TOTAL ANNUAL DEDUCTION: Rs.4,50,000 | |||

"A salaried investor who stacks Section 80C, NPS 80CCD(1B), Section 80D, and Section 24(b) can reduce their taxable income by Rs.4.5 lakh or more every year, before a single market return factors in. Most investors know 80C. Almost none are using all four provisions together." |

- Ckredence Wealth Advisory Team | SEBI Registered Portfolio Management | INP000007164 |

Why Should You Choose Ckredence Wealth?

When you have exhausted your 80C limit and are ready to build wealth beyond it, the choices you make next determine how much your money actually grows. At Ckredence Wealth, we work with HNIs, senior executives, and business owners to build investment portfolios that go beyond standard tax-saving instruments.

Solutions that match your profile:

SEBI-registered portfolio management (INP000007164) with 37 years of wealth management experience

4 distinct investment approaches covering All Weather, Diversified, Business Cycle, and ICE Growth for structured equity allocation beyond mutual funds

Our All Weather Investment Approach delivered +14.58% alpha over BSE 500 TRI in the 1-year period ending June 2026, across 7 market disruption events

Rs.805+ Crores managed across 376+ active clients with consistent focus on capital preservation and risk-adjusted returns

Whether you are a first-time PMS investor moving beyond ELSS or an experienced HNI looking to allocate post-80C surplus into active equity strategies, Ckredence Wealth provides research-backed, personalized guidance. Our team, led by CIO Kartik Mehta with 20+ years of equity experience, builds portfolios that work across market cycles.

Ready to make your post-80C investment decisions count? Schedule a Consultation with Ckredence Wealth.

Conclusion

When your Section 80C limit is exhausted, the investment decisions you make next define your actual wealth trajectory. NPS delivers an extra Rs.50,000 deduction that most salaried professionals leave unused every year. Equity mutual funds and ELSS drive long-term portfolio growth through compounding, while VPF and Sovereign Gold Bonds protect capital with tax-free returns. For short-term surplus, arbitrage and liquid funds beat bank fixed deposits on a post-tax basis for investors in the 30% bracket.

Beyond investment products, Sections 80D, 80E, and 24(b) reduce your taxable income without any new capital commitment. Combining all four deduction provisions can bring total annual tax savings to Rs.4.5 lakh or more. The best post-80C approach is not one product but a goal-matched combination built around your income, risk profile, and investment horizon. For investors with surplus above Rs.50 lakh, working with a SEBI-registered portfolio manager brings the structure and active oversight that index-based instruments cannot provide.

FAQs

01.

What is the best investment after 80C for tax saving?

NPS under Section 80CCD(1B) is the most direct answer — it gives an additional Rs.50,000 deduction independent of the 80C ceiling. For wealth creation alongside tax saving, equity mutual funds and ELSS are the most widely used options after 80C.

02.

Q: Can I invest in ELSS beyond the Rs.1.5 lakh 80C limit?

Yes, ELSS investments above Rs.1.5 lakh do not qualify for the Section 80C deduction. The surplus amount still grows in the same fund with the same 3-year lock-in and market-linked returns.

03.

Are Sovereign Gold Bonds tax-free at maturity?

Yes, capital gains on SGBs held until maturity (8 years) are fully tax-free under the Income Tax Act. The 2.5% annual interest paid semi-annually is taxable as per your applicable income slab.

04.

How much total tax deduction can I claim after 80C?

Beyond 80C's Rs.1.5 lakh, you can claim Rs.50,000 via NPS (80CCD 1B), up to Rs.50,000 via health insurance (80D), and Rs.2 lakh via home loan interest (Section 24b). Total annual deductions can reach Rs.4.5 lakh or more depending on individual eligibility.