13min Read

13min Read

ESOP Proceeds in India: Where to Invest Once the Tax Is Paid

ESOP Proceeds in India: Where to Invest Once the Tax Is Paid

ESOP Proceeds in India: Where to Invest Once the Tax Is Paid

Learn where to invest ESOP proceeds in India after tax, from Section 54F real estate to mutual funds and fixed income options.

Learn where to invest ESOP proceeds in India after tax, from Section 54F real estate to mutual funds and fixed income options.

Learn where to invest ESOP proceeds in India after tax, from Section 54F real estate to mutual funds and fixed income options.

Ckredence Wealth

Ckredence Wealth

|

ESOP proceeds rarely arrive as clean cash. Before you sell a single share, the gap between the fair market value and your exercise price is taxed as a perquisite at your income tax slab rate, often years before the shares are liquid enough to sell. Groww’s own worked example shows a Rs.65 per share gap on a Rs.150 fair market value against an Rs.85 exercise price, taxed immediately, well before you have sold anything. By the time money actually reaches your bank account, a meaningful share of it is already gone to tax, twice.

Before you decide where that money goes, ask yourself:

Do you know how much of your ESOP payout is already spoken for by perquisite tax and capital gains tax combined?

Is most of your net worth still sitting in your employer’s stock, even after the sale?

Are you deciding where to invest the proceeds under pressure, before you have compared your actual options?

We built this guide to walk through where to invest ESOP proceeds in India once the tax is accounted for, covering real estate reinvestment, diversified mutual funds, and fixed income, in the order that matches how most ESOP sellers actually decide.

TL;DR

ESOP gains are taxed twice, once as a perquisite at exercise and again as capital gains at sale, before you decide where to invest what remains.

Section 54F lets you reinvest ESOP sale proceeds into a residential property and defer tax, but only if the shares were held long enough to qualify as long term.

If you have not identified a property yet, the Capital Gains Account Scheme keeps that exemption available while you decide.

Diversifying into mutual funds reduces the concentration risk of holding both your salary and your net worth in one company.

A Systematic Transfer Plan spreads a lump sum into the market over time instead of investing it all on one day.

Once net proceeds cross a meaningful threshold, portfolio management becomes a realistic option, not just mutual funds.

Real Estate to Save Tax on ESOP Proceeds Under Section 54F

If you want to save tax on ESOP proceeds rather than simply invest what is left after tax, Section 54F is usually the first route considered. It lets you reinvest the net sale consideration from your ESOP shares into a residential property in India and claim an exemption on the capital gains.

This route only works for long term gains. ClearTax confirms that Section 54F applies to capital assets held for more than 24 months, so short term ESOP sales do not qualify. Treat the new property as part of your broader asset allocation, not an isolated tax move.

Time limits: buy within 1 year before or 2 years after the sale, or construct within 3 years.

Exemption cap: the maximum exemption under Section 54F is capped at Rs.10 crore, effective from Assessment Year 2024-25.

One property rule: you must not own more than one other residential house at the time of sale.

Not ready yet: if you have not identified a property before filing your return, deposit the unutilised gain in a Capital Gains Account Scheme (CGAS) with an authorised bank to keep the exemption alive.

Real estate suits ESOP sellers who already want another property and can accept an illiquid asset. If your priority is growth without locking money into property, the next option fits better.

FOR LARGE ESOP PAYOUTS |

When ESOP proceeds run into crores, tax deferral alone is not a plan. Our HNI investment planning team structures the full payout, not just the exemption. |

Schedule a Consultation: ckredencewealth.com/contact-us |

Mutual Funds and Diversified Equity: Where to Invest ESOP Proceeds Beyond One Stock

If real estate does not fit your goals, the next place to invest ESOP proceeds is diversified equity. Most ESOP holders already carry concentration risk, since their salary and a large part of their net worth sit inside the same company.

Moving post-tax proceeds into mutual fund advisory spreads that risk across sectors and companies. How the gains get taxed once reinvested depends on the fund category, which is worth understanding through how mutual fund and PMS taxation works before you commit the full amount.

Large-cap and multi-cap equity funds: balance risk and growth for post-tax ESOP proceeds.

Avoid a single lump sum: use a Systematic Transfer Plan to move money into the market over several months, not one day.

LTCG on listed equity: gains above Rs.1.25 lakh in a year are taxed at 12.5 percent under current rules.

Equity exposure grows the portion of your wealth that is no longer tied to your employer. For the portion you want to protect rather than grow, fixed income plays a different role.

REDUCE CONCENTRATION RISK |

Selling ESOP shares does not automatically fix concentration risk if the proceeds sit uninvested or go into a handful of similar stocks. We build a diversification plan around what you already hold. |

Schedule a Consultation: ckredencewealth.com/contact-us |

Fixed Income Instruments for ESOP Proceeds: Capital Preservation and Steady Income

Not every rupee from an ESOP sale needs to chase growth. For the portion meant to preserve capital and generate regular income, fixed income instruments are where to invest ESOP proceeds that you cannot afford to lose.

Corporate fixed deposits from highly rated banks function similarly to a bond allocation inside a portfolio, offering a fixed, predictable return in exchange for lower growth potential.

Public Provident Fund (PPF): long term, tax free interest, government backed.

Senior Citizen Savings Scheme (SCSS): applicable only if you or a family member qualifies by age.

Corporate fixed deposits: choose highly rated banks and NBFCs to limit credit risk.

Whether the goal is an early retirement plan funded partly by this windfall or simply protecting what you have built, fixed income anchors that plan while equity and real estate do the growing.

CAPITAL PRESERVATION, STRUCTURED |

Blending fixed income correctly with the rest of your portfolio takes more than picking the highest rate on offer. Our team sizes the fixed income allocation against your full financial picture. |

Schedule a Consultation: ckredencewealth.com/contact-us |

Where to Invest ESOP Proceeds in India: Comparing Your Options

A side by side view makes the trade off clear.

Option | Time Window / Condition | Tax Treatment | Liquidity | Best For |

Real Estate (Section 54F) | 1 yr before to 2 yr after sale, or 3 yr if constructed | Exemption up to Rs.10 crore on reinvested LTCG | Low, property is illiquid | Large gains, deferring tax long term |

Capital Gains Account Scheme | Deposit before your ITR filing deadline | Preserves the Section 54F exemption while undecided | Locked until used within the window | Sellers still deciding on a property |

Equity Mutual Funds / SIP-STP | No fixed window | LTCG taxed per fund category after 12 months | High, redeem in a few days | Reducing single stock concentration |

Fixed Income (PPF, SCSS, Corporate FD) | Varies by instrument | Interest taxed at slab rate; PPF is exempt | Low to moderate | Capital preservation, steady income |

Table: how each place to invest ESOP proceeds compares on window, tax treatment, and liquidity.

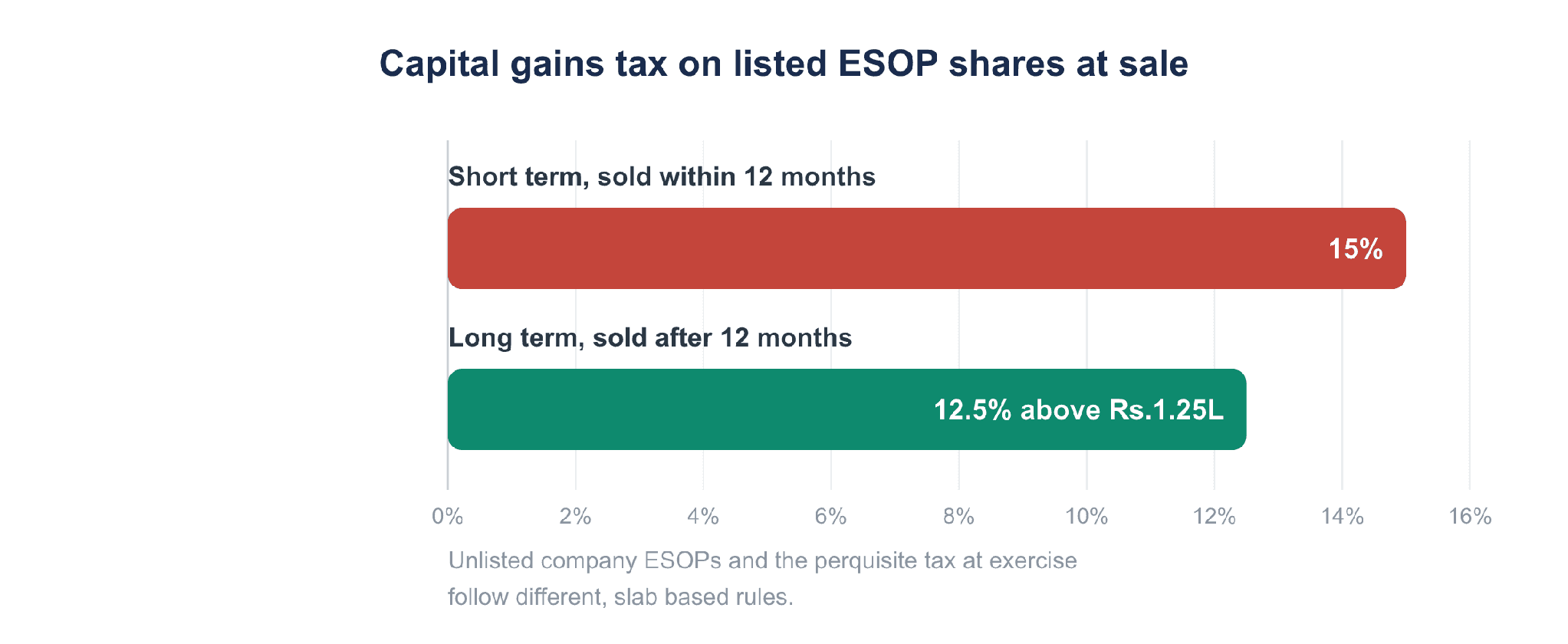

Tax treatment often decides the outcome more than the return itself. The chart below shows what listed ESOP shares owe at sale, depending on how long you held them.

Short term and long term capital gains rates on listed ESOP shares at sale.

Once the tax position is clear, the remaining decision is where the after tax proceeds should go. Use the goal map below to match your situation to the right option.

Match your goal to where to invest ESOP proceeds in India.

Why Should You Choose Ckredence Wealth?

An ESOP payout changes your financial position in a single event, and the decisions made in the first few months often matter more than the ones made later. Ckredence Wealth is a SEBI registered investment advisor (INA000020846) and portfolio manager (INP000007164), built on a 37 year legacy since 1987.

Solutions That Matter:

Fee only advice on where to invest ESOP proceeds in India, through our RIA services.

Structured diversification away from single stock exposure, across our investment approaches.

Portfolio management once proceeds cross our minimum PMS investment threshold of Rs.50 lakh.

Ready to transform your investment approach? Schedule a Consultation!

Conclusion

Where to invest ESOP proceeds in India depends on what the tax has already taken and what you are trying to protect next. Section 54F rewards sellers who want another property and can accept an illiquid asset, while mutual funds and equity reduce the concentration risk of holding your net worth in one company. Fixed income anchors the portion you cannot afford to lose.

None of these choices work well if you make them under pressure. Confirm your actual tax position first, since perquisite tax and capital gains tax already reduced what you have to invest. Then split the remainder across tax deferral, growth, and preservation, matched to your own timeline rather than a single headline option.

FAQs

01.

Where should I invest ESOP proceeds after paying tax?

Split the proceeds by goal. Use real estate under Section 54F to defer tax, mutual funds to reduce concentration risk, and fixed income for capital you cannot afford to lose.

02.

Is ESOP income taxed twice in India?

Yes. The gap between fair market value and exercise price is taxed as a perquisite at exercise, and any further gain is taxed as capital gains when you sell.

03.

Can I use Section 54F to save tax on ESOP share sale proceeds?

Yes, if the shares qualify as a long term capital asset and you reinvest the net sale consideration into a residential property within the prescribed window.

04.

How much ESOP proceeds should go into fixed income versus equity?

There is no fixed ratio. It depends on your existing concentration in employer stock, your time horizon, and how much capital you need to preserve versus grow.

ESOP proceeds rarely arrive as clean cash. Before you sell a single share, the gap between the fair market value and your exercise price is taxed as a perquisite at your income tax slab rate, often years before the shares are liquid enough to sell. Groww’s own worked example shows a Rs.65 per share gap on a Rs.150 fair market value against an Rs.85 exercise price, taxed immediately, well before you have sold anything. By the time money actually reaches your bank account, a meaningful share of it is already gone to tax, twice.

Before you decide where that money goes, ask yourself:

Do you know how much of your ESOP payout is already spoken for by perquisite tax and capital gains tax combined?

Is most of your net worth still sitting in your employer’s stock, even after the sale?

Are you deciding where to invest the proceeds under pressure, before you have compared your actual options?

We built this guide to walk through where to invest ESOP proceeds in India once the tax is accounted for, covering real estate reinvestment, diversified mutual funds, and fixed income, in the order that matches how most ESOP sellers actually decide.

TL;DR

ESOP gains are taxed twice, once as a perquisite at exercise and again as capital gains at sale, before you decide where to invest what remains.

Section 54F lets you reinvest ESOP sale proceeds into a residential property and defer tax, but only if the shares were held long enough to qualify as long term.

If you have not identified a property yet, the Capital Gains Account Scheme keeps that exemption available while you decide.

Diversifying into mutual funds reduces the concentration risk of holding both your salary and your net worth in one company.

A Systematic Transfer Plan spreads a lump sum into the market over time instead of investing it all on one day.

Once net proceeds cross a meaningful threshold, portfolio management becomes a realistic option, not just mutual funds.

Real Estate to Save Tax on ESOP Proceeds Under Section 54F

If you want to save tax on ESOP proceeds rather than simply invest what is left after tax, Section 54F is usually the first route considered. It lets you reinvest the net sale consideration from your ESOP shares into a residential property in India and claim an exemption on the capital gains.

This route only works for long term gains. ClearTax confirms that Section 54F applies to capital assets held for more than 24 months, so short term ESOP sales do not qualify. Treat the new property as part of your broader asset allocation, not an isolated tax move.

Time limits: buy within 1 year before or 2 years after the sale, or construct within 3 years.

Exemption cap: the maximum exemption under Section 54F is capped at Rs.10 crore, effective from Assessment Year 2024-25.

One property rule: you must not own more than one other residential house at the time of sale.

Not ready yet: if you have not identified a property before filing your return, deposit the unutilised gain in a Capital Gains Account Scheme (CGAS) with an authorised bank to keep the exemption alive.

Real estate suits ESOP sellers who already want another property and can accept an illiquid asset. If your priority is growth without locking money into property, the next option fits better.

FOR LARGE ESOP PAYOUTS |

When ESOP proceeds run into crores, tax deferral alone is not a plan. Our HNI investment planning team structures the full payout, not just the exemption. |

Schedule a Consultation: ckredencewealth.com/contact-us |

Mutual Funds and Diversified Equity: Where to Invest ESOP Proceeds Beyond One Stock

If real estate does not fit your goals, the next place to invest ESOP proceeds is diversified equity. Most ESOP holders already carry concentration risk, since their salary and a large part of their net worth sit inside the same company.

Moving post-tax proceeds into mutual fund advisory spreads that risk across sectors and companies. How the gains get taxed once reinvested depends on the fund category, which is worth understanding through how mutual fund and PMS taxation works before you commit the full amount.

Large-cap and multi-cap equity funds: balance risk and growth for post-tax ESOP proceeds.

Avoid a single lump sum: use a Systematic Transfer Plan to move money into the market over several months, not one day.

LTCG on listed equity: gains above Rs.1.25 lakh in a year are taxed at 12.5 percent under current rules.

Equity exposure grows the portion of your wealth that is no longer tied to your employer. For the portion you want to protect rather than grow, fixed income plays a different role.

REDUCE CONCENTRATION RISK |

Selling ESOP shares does not automatically fix concentration risk if the proceeds sit uninvested or go into a handful of similar stocks. We build a diversification plan around what you already hold. |

Schedule a Consultation: ckredencewealth.com/contact-us |

Fixed Income Instruments for ESOP Proceeds: Capital Preservation and Steady Income

Not every rupee from an ESOP sale needs to chase growth. For the portion meant to preserve capital and generate regular income, fixed income instruments are where to invest ESOP proceeds that you cannot afford to lose.

Corporate fixed deposits from highly rated banks function similarly to a bond allocation inside a portfolio, offering a fixed, predictable return in exchange for lower growth potential.

Public Provident Fund (PPF): long term, tax free interest, government backed.

Senior Citizen Savings Scheme (SCSS): applicable only if you or a family member qualifies by age.

Corporate fixed deposits: choose highly rated banks and NBFCs to limit credit risk.

Whether the goal is an early retirement plan funded partly by this windfall or simply protecting what you have built, fixed income anchors that plan while equity and real estate do the growing.

CAPITAL PRESERVATION, STRUCTURED |

Blending fixed income correctly with the rest of your portfolio takes more than picking the highest rate on offer. Our team sizes the fixed income allocation against your full financial picture. |

Schedule a Consultation: ckredencewealth.com/contact-us |

Where to Invest ESOP Proceeds in India: Comparing Your Options

A side by side view makes the trade off clear.

Option | Time Window / Condition | Tax Treatment | Liquidity | Best For |

Real Estate (Section 54F) | 1 yr before to 2 yr after sale, or 3 yr if constructed | Exemption up to Rs.10 crore on reinvested LTCG | Low, property is illiquid | Large gains, deferring tax long term |

Capital Gains Account Scheme | Deposit before your ITR filing deadline | Preserves the Section 54F exemption while undecided | Locked until used within the window | Sellers still deciding on a property |

Equity Mutual Funds / SIP-STP | No fixed window | LTCG taxed per fund category after 12 months | High, redeem in a few days | Reducing single stock concentration |

Fixed Income (PPF, SCSS, Corporate FD) | Varies by instrument | Interest taxed at slab rate; PPF is exempt | Low to moderate | Capital preservation, steady income |

Table: how each place to invest ESOP proceeds compares on window, tax treatment, and liquidity.

Tax treatment often decides the outcome more than the return itself. The chart below shows what listed ESOP shares owe at sale, depending on how long you held them.

Short term and long term capital gains rates on listed ESOP shares at sale.

Once the tax position is clear, the remaining decision is where the after tax proceeds should go. Use the goal map below to match your situation to the right option.

Match your goal to where to invest ESOP proceeds in India.

Why Should You Choose Ckredence Wealth?

An ESOP payout changes your financial position in a single event, and the decisions made in the first few months often matter more than the ones made later. Ckredence Wealth is a SEBI registered investment advisor (INA000020846) and portfolio manager (INP000007164), built on a 37 year legacy since 1987.

Solutions That Matter:

Fee only advice on where to invest ESOP proceeds in India, through our RIA services.

Structured diversification away from single stock exposure, across our investment approaches.

Portfolio management once proceeds cross our minimum PMS investment threshold of Rs.50 lakh.

Ready to transform your investment approach? Schedule a Consultation!

Conclusion

Where to invest ESOP proceeds in India depends on what the tax has already taken and what you are trying to protect next. Section 54F rewards sellers who want another property and can accept an illiquid asset, while mutual funds and equity reduce the concentration risk of holding your net worth in one company. Fixed income anchors the portion you cannot afford to lose.

None of these choices work well if you make them under pressure. Confirm your actual tax position first, since perquisite tax and capital gains tax already reduced what you have to invest. Then split the remainder across tax deferral, growth, and preservation, matched to your own timeline rather than a single headline option.

FAQs

01.

Where should I invest ESOP proceeds after paying tax?

Split the proceeds by goal. Use real estate under Section 54F to defer tax, mutual funds to reduce concentration risk, and fixed income for capital you cannot afford to lose.

02.

Is ESOP income taxed twice in India?

Yes. The gap between fair market value and exercise price is taxed as a perquisite at exercise, and any further gain is taxed as capital gains when you sell.

03.

Can I use Section 54F to save tax on ESOP share sale proceeds?

Yes, if the shares qualify as a long term capital asset and you reinvest the net sale consideration into a residential property within the prescribed window.

04.

How much ESOP proceeds should go into fixed income versus equity?

There is no fixed ratio. It depends on your existing concentration in employer stock, your time horizon, and how much capital you need to preserve versus grow.