11min Read

11min Read

Capital Gains Tax on Property Sale: Where to Reinvest Before the Exemption Window Closes

Capital Gains Tax on Property Sale: Where to Reinvest Before the Exemption Window Closes

Capital Gains Tax on Property Sale: Where to Reinvest Before the Exemption Window Closes

Learn how to save capital gains tax on property sale through Section 54, 54F, 54EC bonds, and the Capital Gains Account Scheme.

Learn how to save capital gains tax on property sale through Section 54, 54F, 54EC bonds, and the Capital Gains Account Scheme.

Learn how to save capital gains tax on property sale through Section 54, 54F, 54EC bonds, and the Capital Gains Account Scheme.

Ckredence Wealth

Ckredence Wealth

|

A property sale can trigger one of the largest tax bills you will ever face in a single year. Under Section 54F, the maximum exemption you can claim by reinvesting in a new residential property is capped at Rs.10 crore, effective from Assessment Year 2024-25 onward. If your gain exceeds that cap, or you miss the reinvestment window entirely, the tax outcome can differ by lakhs of rupees.

Before you decide anything, ask yourself:

Do you know exactly how many months you have to reinvest before the exemption disappears?

If you cannot decide on a new property in time, do you know how to legally park the gains until you do?

Is a bank branch selling you a Capital Gains Account Scheme the same as getting unbiased advice on your full tax position?

We built this guide to walk through every legitimate route to save capital gains tax on property sale proceeds, in the order that matters for your timeline. It covers reinvestment in residential property, the Capital Gains Account Scheme, capital gain bonds, and the deductions most sellers miss.

TL;DR

Section 54 and 54F require reinvesting in a new residential property within 1 year before or 2 years after the sale, or 3 years if you construct.

If you have not identified a new property before filing your return, the Capital Gains Account Scheme lets you park the gain without losing the exemption.

Section 54EC bonds let you skip buying another property entirely, but the investment is capped and carries a 5 year lock in.

Indexation and deductible expenses reduce your taxable gain before you even consider reinvestment.

Missing any of these deadlines converts a plannable exemption into an immediate tax liability.

The right route depends on whether you already have a new property lined up, not just which section offers the biggest exemption.

Reinvest in Residential Property: The Direct Way to Save Capital Gains Tax on Property Sale

The most direct way to save capital gains tax on property sale proceeds is to reinvest in another residential property. Section 54 applies when you sell a residential house, and Section 54F applies when you sell any other capital asset, such as land, a plot, or listed shares.

Both sections need the new purchase to fit inside a strict window. Treat the reinvestment as part of your broader asset allocation, not an isolated tax move, since the new property becomes a real component of your net worth.

Time limits: buy within 1 year before or 2 years after the sale, or construct within 3 years.

Exemption cap: Section 54F exemption is capped at Rs.10 crore for gains from non-residential assets, effective from Assessment Year 2024-25.

One property rule: under Section 54F, you must not own more than one other residential house at the time of sale.

Full reinvestment under 54F: you must reinvest the entire net sale consideration, not just the gain, to claim the full exemption.

Reinvesting works well when you already know which property you want. If you are still deciding, the next option keeps your exemption alive without rushing the decision.

FOR LARGE PROPERTY SALE PROCEEDS |

When a sale nears or exceeds the exemption cap, the leftover proceeds need a structured plan, not a parking spot. Our HNI investment planning team builds that plan around your full tax position. |

Schedule a Consultation: ckredencewealth.com/contact-us |

Park Funds in a Capital Gains Account Scheme to Save Capital Gains Tax on Property Sale

If you have not identified or purchased a new property before filing your income tax return, the Capital Gains Account Scheme protects your exemption. You deposit the unutilised gain into a CGAS account with a public sector bank or a notified private bank, instead of losing the benefit by default.

The deposit must happen before your return filing deadline, not before the reinvestment deadline itself. Getting that sequence wrong is one of the more common mistakes we see, which is why advisory support around the filing calendar matters as much as the investment choice.

Deadline: deposit before you file your income tax return for the year of sale, not before the full reinvestment window closes.

Withdrawal: funds can be withdrawn later, within the 2 to 3 year construction or purchase window, to complete the property purchase.

Interest treatment: interest earned on the CGAS deposit is taxed as income from other sources, not as capital gains.

A CGAS account only holds the gain in place. It does not grow it, so most sellers still want a clear investment plan for the money once it comes out.

CGAS TIMELINE PLANNING |

Missing the ITR filing deadline for your CGAS deposit can undo the exemption entirely. Our RIA team tracks the filing calendar and reinvestment window together so nothing slips. |

Schedule a Consultation: ckredencewealth.com/contact-us |

Invest in Capital Gain Bonds Under Section 54EC to Save Capital Gains Tax on Property Sale

If you do not want to buy another property at all, Section 54EC lets you save capital gains tax on property sale proceeds by investing in specified bonds instead. NHAI and REC are the two most commonly issued bonds under this section.

These bonds function like a fixed income allocation inside your portfolio, except the primary purpose is the tax exemption rather than the coupon.

Investment window: you must invest within 6 months of the property sale date.

Cap: the maximum investment eligible for exemption is Rs.50 lakh in a financial year.

Lock in: these bonds carry a mandatory 5 year lock in and cannot be sold or transferred before maturity.

Applicability: the exemption applies only to long term capital gains from land or a building, not from other capital assets.

Section 54EC suits sellers who want a clean exit from real estate altogether. For gains that exceed what any of these three routes can shelter, the remaining lever is reducing the taxable gain itself.

BOND SELECTION, VETTED |

Choosing between NHAI, REC, or other notified bonds is easier once you see how they sit alongside your other fixed income holdings, not just the exemption they unlock. |

Schedule a Consultation: ckredencewealth.com/contact-us |

Deduct Expenses and Apply Indexation to Save Capital Gains Tax on Property Sale

Before you reinvest a single rupee, check whether you have reduced the taxable gain itself. Transfer expenses such as brokerage, legal fees, and documented home improvement costs are deductible from the sale price.

Indexation adjusts your original purchase price for inflation on eligible long term holdings, which lowers the gain before any exemption is even calculated. The same logic applies when you compare how different investments are taxed once the sale proceeds are reinvested elsewhere.

Deductible expenses: brokerage, legal fees, and renovation costs reduce the sale price used to calculate your gain.

Indexation benefit: available on eligible long term property holdings to adjust the purchase price for inflation.

Combined effect: a lower calculated gain means a smaller amount needs an exemption route at all.

These deductions do not replace Sections 54, 54F, or 54EC. They simply shrink the number those sections need to shelter.

FULL TAX POSITION REVIEW |

Expense deductions, indexation, and exemption sections interact with each other. A single miscalculation can cost lakhs. Our financial advisory team reviews the full position before you file. |

Schedule a Consultation: ckredencewealth.com/contact-us |

How to Save Capital Gains Tax on Property Sale: Comparing Your Options

A side by side view makes the trade off clear.

Table: how each route to save capital gains tax on property sale compares on window, cap, and lock in.

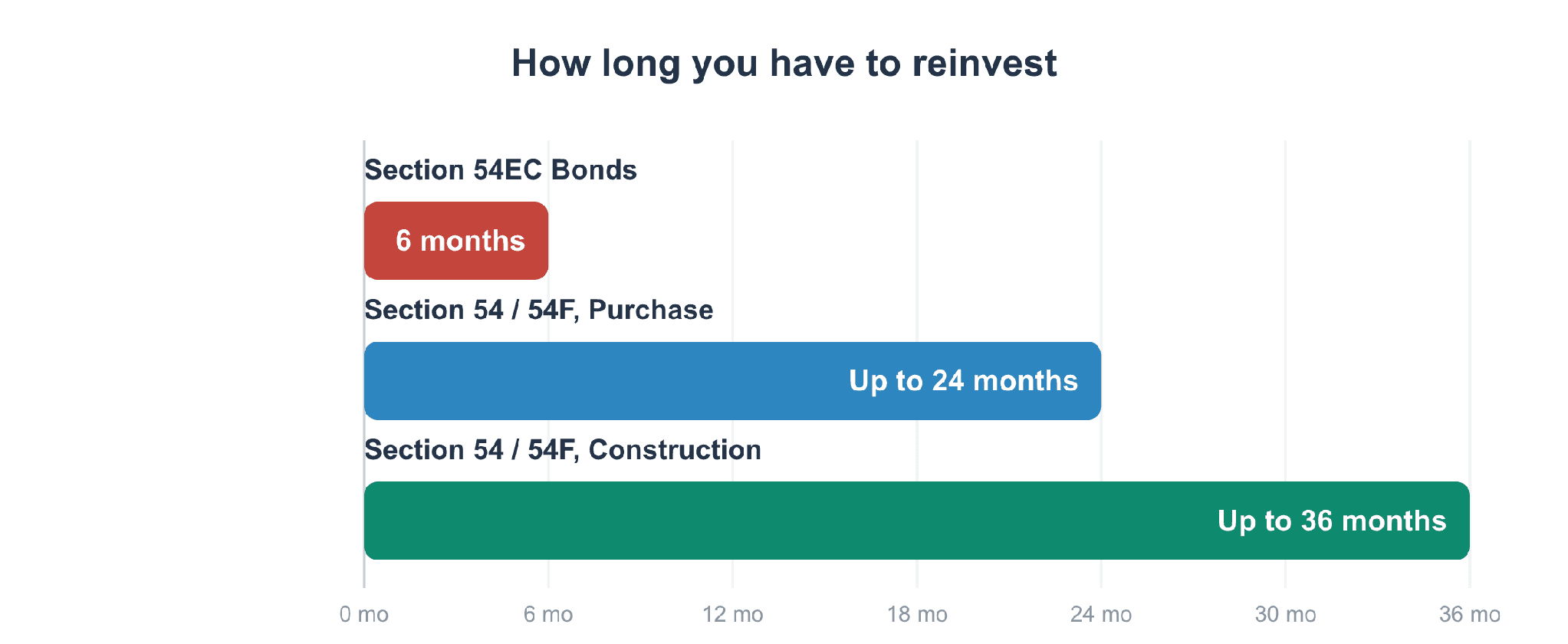

Deadlines are the real constraint here, more than the exemption amount itself. The chart below places the three fixed windows next to each other.

Investment window length, in months, for each reinvestment route.

The Capital Gains Account Scheme is not on this chart because its deadline tracks your income tax return filing date, not a fixed number of months. Use the goal map below to place it correctly against your own situation.

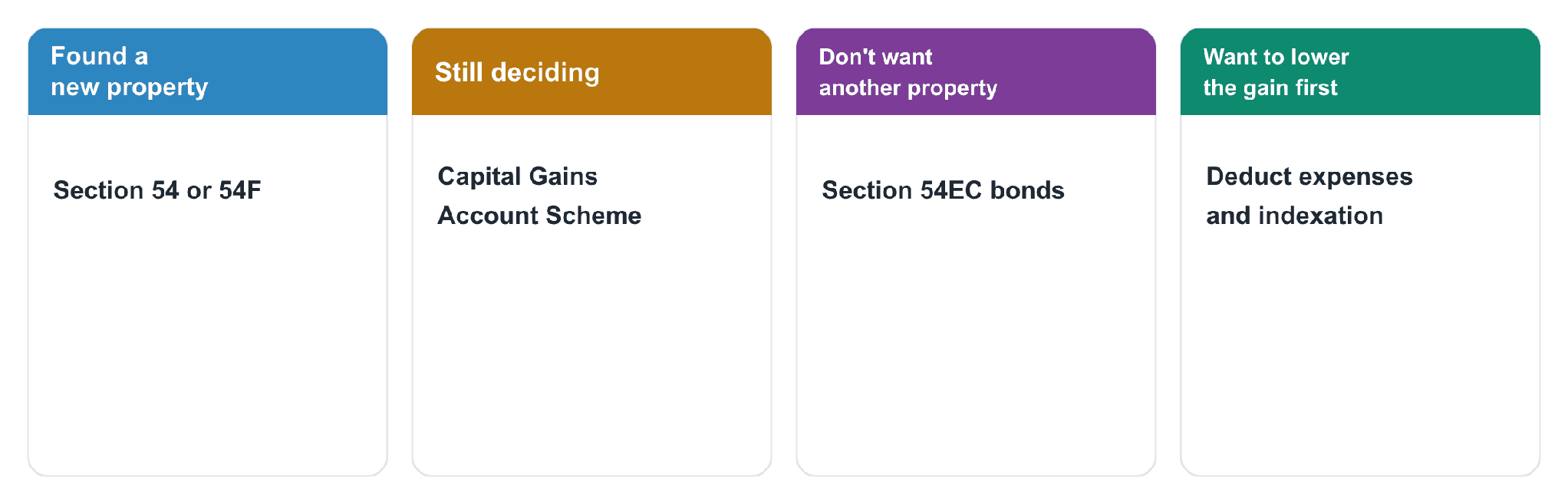

Match your situation to the right route to save capital gains tax on property sale.

Why Should You Choose Ckredence Wealth?

A large property sale changes your financial position in a single transaction. Ckredence Wealth is a SEBI registered investment advisor (INA000020846) and portfolio manager (INP000007164), built on a 37 year legacy since 1987.

Solutions That Matter:

Fee only advice on how to save capital gains tax on property sale proceeds, through our RIA services.

Structured reinvestment of the surplus once your exemption is secured, across our investment approaches.

Portfolio management for proceeds above the exemption cap, starting at our minimum PMS investment threshold.

Ready to transform your investment approach? Schedule a Consultation!

Conclusion

Saving capital gains tax on property sale proceeds almost always comes down to timing. Section 54 and 54F reward sellers who already have a new residential property lined up, while the Capital Gains Account Scheme protects the exemption for those who need more time to decide. Section 54EC bonds offer a clean exit from real estate entirely, within a tighter six month window and a lower cap.

None of these routes work if you miss the deadline that applies to your situation. Reduce the gain first through documented expenses and indexation, then choose the reinvestment route that matches your timeline rather than the one with the biggest headline exemption. A plan built around your actual deadline protects more of the sale proceeds than any single section can on its own.

FAQs

01.

What is the time limit to reinvest capital gains from a property sale?

Under Section 54 and 54F, you must buy within 1 year before or 2 years after the sale, or construct a new house within 3 years.

02.

Can I claim exemption if I have not bought a new property before filing my return?

Yes. Deposit the gain in a Capital Gains Account Scheme before your filing deadline to keep the exemption available while you decide.

03.

How much can I invest in Section 54EC bonds to save tax?

p to Rs.50 lakh in a financial year, invested within 6 months of the sale, with a mandatory 5 year lock in.

04.

Is indexation still available on property sold today?

Indexation generally applies to eligible long term holdings, though recent Finance Act changes affect how it interacts with the applicable tax rate, so confirm the current rule for your sale year before filing.

A property sale can trigger one of the largest tax bills you will ever face in a single year. Under Section 54F, the maximum exemption you can claim by reinvesting in a new residential property is capped at Rs.10 crore, effective from Assessment Year 2024-25 onward. If your gain exceeds that cap, or you miss the reinvestment window entirely, the tax outcome can differ by lakhs of rupees.

Before you decide anything, ask yourself:

Do you know exactly how many months you have to reinvest before the exemption disappears?

If you cannot decide on a new property in time, do you know how to legally park the gains until you do?

Is a bank branch selling you a Capital Gains Account Scheme the same as getting unbiased advice on your full tax position?

We built this guide to walk through every legitimate route to save capital gains tax on property sale proceeds, in the order that matters for your timeline. It covers reinvestment in residential property, the Capital Gains Account Scheme, capital gain bonds, and the deductions most sellers miss.

TL;DR

Section 54 and 54F require reinvesting in a new residential property within 1 year before or 2 years after the sale, or 3 years if you construct.

If you have not identified a new property before filing your return, the Capital Gains Account Scheme lets you park the gain without losing the exemption.

Section 54EC bonds let you skip buying another property entirely, but the investment is capped and carries a 5 year lock in.

Indexation and deductible expenses reduce your taxable gain before you even consider reinvestment.

Missing any of these deadlines converts a plannable exemption into an immediate tax liability.

The right route depends on whether you already have a new property lined up, not just which section offers the biggest exemption.

Reinvest in Residential Property: The Direct Way to Save Capital Gains Tax on Property Sale

The most direct way to save capital gains tax on property sale proceeds is to reinvest in another residential property. Section 54 applies when you sell a residential house, and Section 54F applies when you sell any other capital asset, such as land, a plot, or listed shares.

Both sections need the new purchase to fit inside a strict window. Treat the reinvestment as part of your broader asset allocation, not an isolated tax move, since the new property becomes a real component of your net worth.

Time limits: buy within 1 year before or 2 years after the sale, or construct within 3 years.

Exemption cap: Section 54F exemption is capped at Rs.10 crore for gains from non-residential assets, effective from Assessment Year 2024-25.

One property rule: under Section 54F, you must not own more than one other residential house at the time of sale.

Full reinvestment under 54F: you must reinvest the entire net sale consideration, not just the gain, to claim the full exemption.

Reinvesting works well when you already know which property you want. If you are still deciding, the next option keeps your exemption alive without rushing the decision.

FOR LARGE PROPERTY SALE PROCEEDS |

When a sale nears or exceeds the exemption cap, the leftover proceeds need a structured plan, not a parking spot. Our HNI investment planning team builds that plan around your full tax position. |

Schedule a Consultation: ckredencewealth.com/contact-us |

Park Funds in a Capital Gains Account Scheme to Save Capital Gains Tax on Property Sale

If you have not identified or purchased a new property before filing your income tax return, the Capital Gains Account Scheme protects your exemption. You deposit the unutilised gain into a CGAS account with a public sector bank or a notified private bank, instead of losing the benefit by default.

The deposit must happen before your return filing deadline, not before the reinvestment deadline itself. Getting that sequence wrong is one of the more common mistakes we see, which is why advisory support around the filing calendar matters as much as the investment choice.

Deadline: deposit before you file your income tax return for the year of sale, not before the full reinvestment window closes.

Withdrawal: funds can be withdrawn later, within the 2 to 3 year construction or purchase window, to complete the property purchase.

Interest treatment: interest earned on the CGAS deposit is taxed as income from other sources, not as capital gains.

A CGAS account only holds the gain in place. It does not grow it, so most sellers still want a clear investment plan for the money once it comes out.

CGAS TIMELINE PLANNING |

Missing the ITR filing deadline for your CGAS deposit can undo the exemption entirely. Our RIA team tracks the filing calendar and reinvestment window together so nothing slips. |

Schedule a Consultation: ckredencewealth.com/contact-us |

Invest in Capital Gain Bonds Under Section 54EC to Save Capital Gains Tax on Property Sale

If you do not want to buy another property at all, Section 54EC lets you save capital gains tax on property sale proceeds by investing in specified bonds instead. NHAI and REC are the two most commonly issued bonds under this section.

These bonds function like a fixed income allocation inside your portfolio, except the primary purpose is the tax exemption rather than the coupon.

Investment window: you must invest within 6 months of the property sale date.

Cap: the maximum investment eligible for exemption is Rs.50 lakh in a financial year.

Lock in: these bonds carry a mandatory 5 year lock in and cannot be sold or transferred before maturity.

Applicability: the exemption applies only to long term capital gains from land or a building, not from other capital assets.

Section 54EC suits sellers who want a clean exit from real estate altogether. For gains that exceed what any of these three routes can shelter, the remaining lever is reducing the taxable gain itself.

BOND SELECTION, VETTED |

Choosing between NHAI, REC, or other notified bonds is easier once you see how they sit alongside your other fixed income holdings, not just the exemption they unlock. |

Schedule a Consultation: ckredencewealth.com/contact-us |

Deduct Expenses and Apply Indexation to Save Capital Gains Tax on Property Sale

Before you reinvest a single rupee, check whether you have reduced the taxable gain itself. Transfer expenses such as brokerage, legal fees, and documented home improvement costs are deductible from the sale price.

Indexation adjusts your original purchase price for inflation on eligible long term holdings, which lowers the gain before any exemption is even calculated. The same logic applies when you compare how different investments are taxed once the sale proceeds are reinvested elsewhere.

Deductible expenses: brokerage, legal fees, and renovation costs reduce the sale price used to calculate your gain.

Indexation benefit: available on eligible long term property holdings to adjust the purchase price for inflation.

Combined effect: a lower calculated gain means a smaller amount needs an exemption route at all.

These deductions do not replace Sections 54, 54F, or 54EC. They simply shrink the number those sections need to shelter.

FULL TAX POSITION REVIEW |

Expense deductions, indexation, and exemption sections interact with each other. A single miscalculation can cost lakhs. Our financial advisory team reviews the full position before you file. |

Schedule a Consultation: ckredencewealth.com/contact-us |

How to Save Capital Gains Tax on Property Sale: Comparing Your Options

A side by side view makes the trade off clear.

Table: how each route to save capital gains tax on property sale compares on window, cap, and lock in.

Deadlines are the real constraint here, more than the exemption amount itself. The chart below places the three fixed windows next to each other.

Investment window length, in months, for each reinvestment route.

The Capital Gains Account Scheme is not on this chart because its deadline tracks your income tax return filing date, not a fixed number of months. Use the goal map below to place it correctly against your own situation.

Match your situation to the right route to save capital gains tax on property sale.

Why Should You Choose Ckredence Wealth?

A large property sale changes your financial position in a single transaction. Ckredence Wealth is a SEBI registered investment advisor (INA000020846) and portfolio manager (INP000007164), built on a 37 year legacy since 1987.

Solutions That Matter:

Fee only advice on how to save capital gains tax on property sale proceeds, through our RIA services.

Structured reinvestment of the surplus once your exemption is secured, across our investment approaches.

Portfolio management for proceeds above the exemption cap, starting at our minimum PMS investment threshold.

Ready to transform your investment approach? Schedule a Consultation!

Conclusion

Saving capital gains tax on property sale proceeds almost always comes down to timing. Section 54 and 54F reward sellers who already have a new residential property lined up, while the Capital Gains Account Scheme protects the exemption for those who need more time to decide. Section 54EC bonds offer a clean exit from real estate entirely, within a tighter six month window and a lower cap.

None of these routes work if you miss the deadline that applies to your situation. Reduce the gain first through documented expenses and indexation, then choose the reinvestment route that matches your timeline rather than the one with the biggest headline exemption. A plan built around your actual deadline protects more of the sale proceeds than any single section can on its own.

FAQs

01.

What is the time limit to reinvest capital gains from a property sale?

Under Section 54 and 54F, you must buy within 1 year before or 2 years after the sale, or construct a new house within 3 years.

02.

Can I claim exemption if I have not bought a new property before filing my return?

Yes. Deposit the gain in a Capital Gains Account Scheme before your filing deadline to keep the exemption available while you decide.

03.

How much can I invest in Section 54EC bonds to save tax?

p to Rs.50 lakh in a financial year, invested within 6 months of the sale, with a mandatory 5 year lock in.

04.

Is indexation still available on property sold today?

Indexation generally applies to eligible long term holdings, though recent Finance Act changes affect how it interacts with the applicable tax rate, so confirm the current rule for your sale year before filing.