9min read

9min read

Best Sector-Based PMS in India 2026: HNI Evaluation Guide

Best Sector-Based PMS in India 2026: HNI Evaluation Guide

Best Sector-Based PMS in India 2026: HNI Evaluation Guide

Sector PMS returns look strong until a cycle reverses. Learn how HNIs with ₹50 lakh+ evaluate drawdown, rotation discipline, and manager track record before investing.

Sector PMS returns look strong until a cycle reverses. Learn how HNIs with ₹50 lakh+ evaluate drawdown, rotation discipline, and manager track record before investing.

Sector PMS returns look strong until a cycle reverses. Learn how HNIs with ₹50 lakh+ evaluate drawdown, rotation discipline, and manager track record before investing.

Ckredence Wealth

Ckredence Wealth

|

India's PMS industry crossed ₹35 lakh crore in assets under management in early 2025, up from ₹32.1 lakh crore in January 2024, with manufacturing, defence, BFSI, and green energy themes driving the fastest inflows.

Sector-based PMS strategies have moved from niche allocations to mainstream HNI conversations, driven by concentrated return cycles that look compelling in marketing presentations but carry risks that 1-year CAGR figures do not capture.

For investors deploying ₹50 lakh or more, PMS client numbers grew 27% in 2025, reflecting genuine appetite for personalised, strategy-led wealth management. Choosing the best sector-based PMS in India is no longer about identifying which theme is performing now.

It is about understanding concentration risk, sector rotation discipline, drawdown control, and manager decision-making quality across full market cycles, including the ones that turn against the strategy.

Key Takeaways

Sector PMS concentrates capital within specific industries, unlike diversified or thematic mandates

Return data from sector PMS is structurally cycle-dependent and often compared at peak timing

Maximum historical drawdown matters more than 1-year CAGR in concentrated strategies

Sector rotation discipline, not stock selection alone, determines multi-cycle performance consistency

Manufacturing, BFSI, and defence dominated sector PMS inflows across 2024 and 2025

Fee structures in concentrated PMS strategies become more visible during weaker market phases

Investor suitability, risk tolerance, and liquidity needs must precede any sector allocation decision

What Is a Sector-Based PMS in India?

A sector-based PMS in India is a SEBI-regulated discretionary portfolio management strategy that concentrates investments within selected sectors or themes instead of spreading exposure across the broader market.

Unlike diversified PMS portfolios, sector PMS mandates take intentional concentrated positions in sectors where the manager sees long-term structural opportunity. For HNI investors, this creates the possibility of stronger returns during strong sector cycles, and sharper drawdowns when the sector turns.

Understanding the differences across our guide to types of portfolio management services helps investors select the mandate structure that fits their actual risk profile.

Sector PMS vs Diversified PMS vs Thematic PMS

Type | Focus | Portfolio Structure | Risk Level | Best Fit |

Sector-Based PMS | One or few sectors | Concentrated | High | Experienced HNIs |

Diversified PMS | Multi-sector allocation | Broad exposure | Moderate | Long-term investors |

Thematic PMS | Macro theme-based | Cross-sector thematic | Moderate to High | Theme-specific investors |

Sector PMS vs Thematic PMS: Is There a Difference?

Sector PMS focuses on industries like BFSI, manufacturing, or technology. Thematic PMS combines multiple sectors under one broader narrative such as digitisation, defence, or green energy.

The structural distinction matters because thematic PMS typically carries lower concentration risk by spreading across related but distinct industries.

Which Sectors Do PMS Managers Concentrate In?

Most sector-focused PMS managers in India currently allocate within manufacturing, BFSI, technology, defence, consumption, green energy, and specialty chemicals. Each carries its own return cycle, volatility pattern, and macro dependency.

Manufacturing strategies benefit from India's capex cycle and PLI growth. BFSI strategies focus on credit expansion and financialisation trends. Defence strategies target government spending and domestic production mandates.

Green energy and specialty chemicals strategies track global supply chain shifts and energy transition capital flows.

SEBI-regulated PMS managers operate under disclosure and reporting requirements, but sector PMS portfolios still carry considerably higher concentration risk compared to diversified mandates, regardless of platform or track record.

"Risk comes from not knowing what you're doing." Warren Buffett, Chairman and CEO, Berkshire Hathaway

Source: Berkshire Hathaway Shareholder Letters

Most Sector PMS Return Data Is Built to Mislead Investors

Most investors evaluating the best sector-based PMS in India are comparing peak-cycle numbers without knowing it. A manufacturing-focused PMS delivering 38-42% returns after a sector rally looks compelling on a presentation slide.

What rarely gets discussed is what happened before the rally began or after the cycle reversed.

Sector PMS returns are highly cycle-dependent. A strategy can look exceptional during one phase and underperform sharply once momentum weakens. Several BFSI and manufacturing-heavy strategies generated 40%+ returns during FY24-FY25.

Investors who entered near cycle peaks experienced meaningful drawdowns once sector momentum slowed. The problem was not stock selection. It was timing, entry point, and concentration.

The Right Metrics to Evaluate Instead

Weak Metric | Better Metric |

1-Year CAGR | Rolling 3-Year Return |

Peak Return Snapshot | Drawdown Recovery Speed |

Marketing CAGR | Risk-Adjusted Return |

Sector Momentum | Exit Discipline |

What a Sector PMS Should Show You Before You Invest

A transparent PMS manager should explain maximum historical drawdown, recovery period after sector corrections, rolling performance across full market cycles, and exit discipline during sector reversals.

Our guide to portfolio management strategies covers the framework used to evaluate these dimensions before any allocation decision. Without that information, the investor is evaluating returns without understanding the risk structure behind the strategy.

📊 India's PMS AUM crossed ₹35 lakh crore in early 2025, up from ₹32.1 lakh crore in January 2024: Manufacturing, defence, and BFSI sector strategies attracted the highest concentrated inflows across this period. Source: Storifynews citing SEBI Data, October 2025

💼 If a sector PMS manager cannot show you maximum drawdown history and exit discipline from a previous correction cycle, the evaluation is incomplete. Talk to a Ckredence advisor for a risk-adjusted sector PMS review covering drawdown history, rolling returns, and investor suitability.

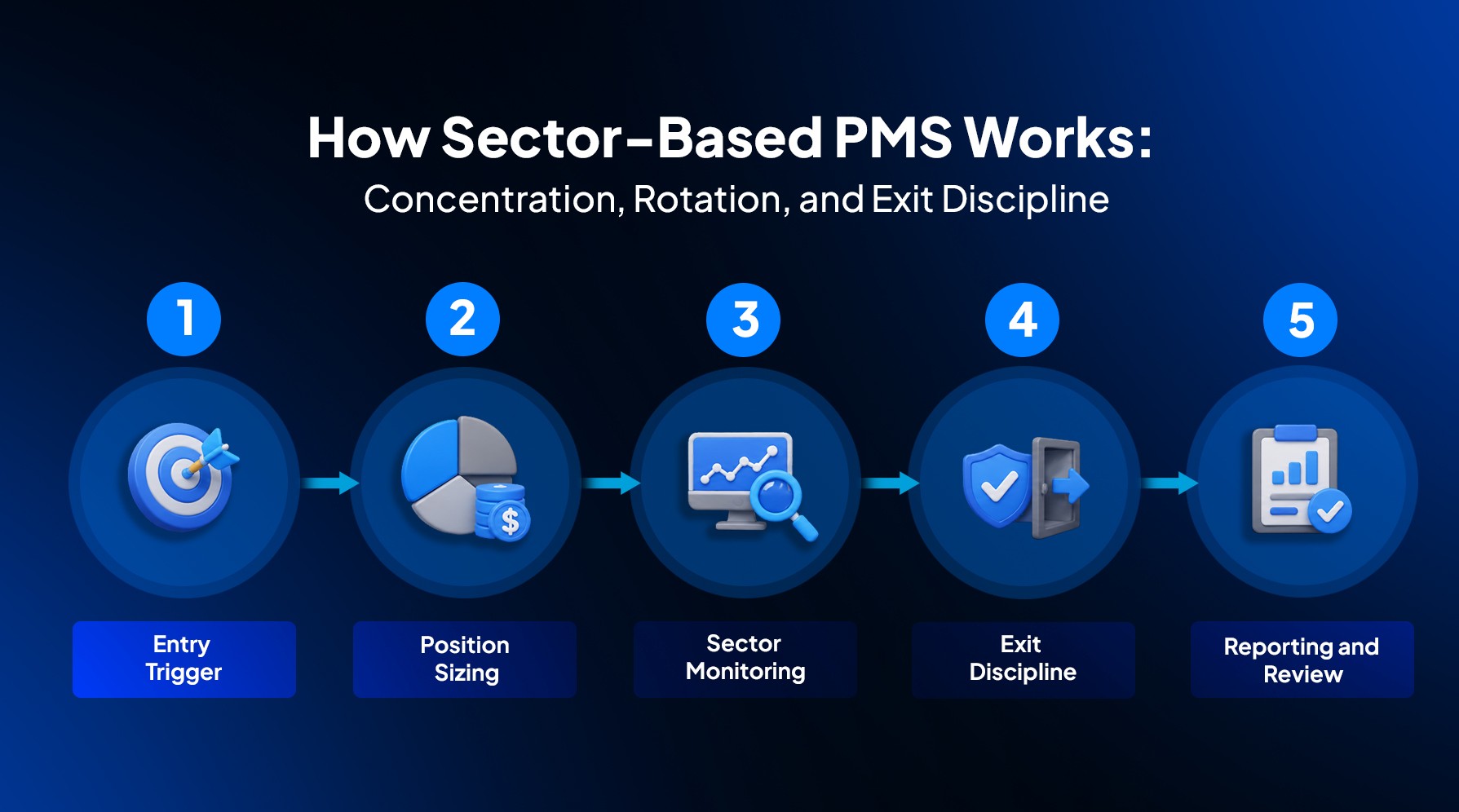

How Sector-Based PMS Works: Concentration, Rotation, and Exit Discipline

Sector PMS works differently from diversified mandates because allocation decisions concentrate capital around sector conviction rather than spreading risk across industries.

Understanding the process behind that concentration separates an informed allocation from a return-chasing decision. Our guide to the 5 phases of portfolio management explains how each phase applies to concentrated sector mandates specifically.

1. Entry Trigger

Managers identify sectors where valuations, earnings growth, policy support, or economic cycles create a clear opportunity.

Entry should come before momentum becomes crowded, not after trailing returns have already attracted flows.

2. Position Sizing

Capital is allocated aggressively toward high-conviction sectors rather than spreading exposure evenly.

This is where concentration risk becomes a structural feature of the strategy, not a temporary condition.

3. Sector Monitoring

Managers continuously review earnings, policy changes, valuations, and institutional flows.

The monitoring phase determines whether the sector thesis remains intact or whether rotation is warranted.

4. Exit Discipline

Positions are reduced or exited when valuations become excessive or sector momentum weakens.

Strong sector PMS managers define exit thresholds before volatility appears. Weak managers react after drawdowns have already compounded.

5. Reporting and Review

Investors receive portfolio statements, sector allocation visibility, and periodic commentary.

Reporting quality is a direct signal of manager transparency and is worth evaluating before any capital is deployed.

The Role of Drawdown Limits in Sector PMS Mandates

Strong sector PMS managers define exit discipline before volatility appears. If the advisor presenting a sector PMS cannot explain the drawdown trigger or exit logic from a previous cycle, the evaluation is looking at a return history, not a strategy.

"The intelligent investor is a realist who sells to optimists and buys from pessimists." Benjamin Graham, Author, The Intelligent Investor

Source: The Intelligent Investor, Revised Edition, HarperCollins

What Has Changed in Sector-Based PMS in India in 2026

Sector leadership shifted sharply between FY25 and FY26. Manufacturing and capital expenditure themes dominated PMS conversations in FY25, while IT-focused strategies struggled through parts of FY26 due to slower earnings momentum and delayed sector rotation.

Sector | FY25 Return Trend | FY26 Trend | Manager Positioning |

Manufacturing | Strong outperformance | Stable | Aggressive overweight |

BFSI | Consistent | Positive | Broad allocation |

Technology | Mixed | Underperformance | Rotation challenges |

Defence | Strong momentum | High volatility | Tactical exposure |

Green Energy | Momentum-driven | Selective | Theme-based allocation |

The IT Correction Revealed Manager Skill Differences

Some PMS managers remained overweight technology even after earnings momentum weakened. Others rotated earlier into manufacturing, BFSI, or defence-linked themes.

This difference in sector rotation discipline became visible quickly in portfolio performance across the year. The divergence confirmed that sector PMS outcomes depend heavily on rotation logic, not just initial theme selection.

New Themes Emerging in 2026

Thematic allocation conversations are now expanding toward defence manufacturing, green energy infrastructure, specialty chemicals, domestic manufacturing, and financialisation themes. The challenge is no longer identifying the theme.

It is identifying which managers rotate out before the cycle weakens.

📊 Defence-focused PMS strategies saw 30-35% inflows growth in the first half of 2025 alone: Government defence spending and the Make in India push drove concentrated sector allocation into listed defence companies.

Source: Storifynews citing SEBI and APMI Data, October 2025

📋 High inflows into a sector PMS after a strong return cycle often signals late entry risk, not opportunity. Request a structured sector allocation review from Ckredence Wealth before adding concentration to any sector theme.

How to Choose the Best Sector-Based PMS in India: 5 Criteria Most Investors Never Check

Most investors compare sector PMS strategies using CAGR alone. Choosing the right sector PMS requires evaluating drawdown discipline, rolling returns, rotation logic, manager transparency, and full fee structures across market cycles, not just the headline return from the strongest phase.

Criterion | What Good Looks Like | Red Flag | Question to Ask |

Drawdown Control | Controlled corrections | Deep unrecovered losses | What was the maximum drawdown? |

Rolling Returns | Consistent multi-cycle performance | One-cycle dependence | How did returns behave across 3Y rolling periods? |

Sector Rotation Discipline | Early exits during reversals | Late-cycle holding | How do you decide exits? |

Manager Transparency | Clear reporting across cycles | Performance-only communication | How often are portfolio reviews shared? |

Fee Structure | Transparent total cost model | Hidden cost layering | What is the total cost structure? |

What a Good Sector PMS Track Record Looks Like

A strong sector PMS track record should show manageable drawdowns, reasonable recovery speed after market downturns, consistent performance across different market environments, and disciplined communication during both strong and weak market periods.

Our guide to how to invest in portfolio management services covers the 8-step evaluation process HNIs should follow before deploying capital into any PMS strategy, including sector-concentrated mandates.

Fee Structures Matter More Than Most Investors Realise

In concentrated PMS strategies, fees become more visible during weaker market cycles. A 2025 investor review found that fewer than 20% of HNI investors asked about maximum drawdown before deploying capital into IT-heavy sector strategies.

Those who ignored drawdown analysis experienced meaningful portfolio erosion during the correction phase.

🔍 Most sector PMS comparisons stop at the 3-year return table without asking what the drawdown looked like before the rally began. Book a structured sector PMS evaluation with Ckredence Wealth and compare your shortlist on risk-adjusted terms before deploying.

Best Sector-Based PMS in India 2026

The best sector-based PMS in India depends less on recent returns and more on investor suitability, concentration tolerance, and manager discipline across full market cycles.

PMS Strategy | Investment Philosophy | Return Profile | Drawdown Profile | Best-Fit Investor |

Aditya Birla Select Sector Portfolio | Sector rotation focus | Moderate | Moderate | Tactical allocation seekers |

Ckredence Wealth PMS Strategies | Risk-adjusted sector allocation with active monitoring | Balanced to Growth-Oriented | Controlled | HNIs seeking advisor-led sector allocation |

Green Portfolio Super 30 Dynamic | High-conviction thematic allocation | Strong | Moderate to High | Aggressive HNIs |

ICICI Prudential Growth Leaders | Sector-leading companies | Balanced | Moderate | Long-term HNIs |

Negen Capital Special Situations and Technology | Technology and special situations | Volatile | High | High-risk tolerance investors |

Aditya Birla Select Sector Portfolio focuses on tactical sector opportunities while maintaining broader institutional portfolio discipline.

Green Portfolio Super 30 Dynamic is known for concentrated thematic exposure and aggressive sector positioning during manufacturing and growth cycles.

ICICI Prudential Growth Leaders follows a relatively balanced quality-growth approach compared to more concentrated thematic strategies.

Negen Capital Special Situations and Technology attracts investors seeking higher-growth technology and thematic opportunities with higher volatility tolerance.

Ckredence Wealth PMS Strategies approach sector allocation as a risk-management decision first and a return opportunity second.

An investor who entered Green Portfolio Super 30 Dynamic in early 2023 with ₹75 lakh saw appreciation through the manufacturing cycle.

A comparable investor concentrated heavily in weaker IT-sector exposure experienced lower returns with deeper interim volatility. The difference was not stock selection alone. It was sector rotation discipline and entry timing relative to the cycle.

Who Should Not Invest in a Sector-Based PMS in India

Sector PMS is not suitable for every investor.

Investor Profile | Sector PMS Suitability | Reason |

First-time PMS investor | Not recommended | Concentration risk may feel excessive before building experience |

Investor below ₹50 lakh deployable surplus | Not recommended | Allocation risk becomes disproportionately high at smaller corpus |

Long-term HNI with diversified wealth base | Suitable | Better ability to absorb sector volatility across a full portfolio |

Investor seeking stable moderate returns | Not recommended | Diversified PMS structures may be more appropriate |

When Diversified PMS Makes More Sense

Investors who prefer smoother volatility, lack sector-specific understanding, cannot absorb sharp drawdowns, or prefer broader market participation may find that diversified PMS structures suit their profile better than concentrated sector mandates.

Our overview of types of portfolio management services covers how discretionary, non-discretionary, and diversified structures differ in practice.

Why Ckredence Wealth for Sector-Based PMS Allocation in India

Choosing a sector PMS manager is not just about selecting the highest-return strategy.

The real challenge is understanding how the manager behaves when the sector cycle weakens, how risk is controlled during volatility, and whether the allocation matches the investor's financial profile.

At Ckredence Wealth, our PMS advisory approach treats sector allocation as a risk-management decision first and a return opportunity second.

The focus is on building sustainable long-term allocation structures for HNI investors, not chasing whichever sector performed best last year.

Drawdown Discipline Evaluation: Many PMS presentations highlight only peak returns. We evaluate how the manager handled difficult phases, corrections, and sector reversals before considering allocation suitability.

Entry Timing and Allocation Logic: Sector allocation timing matters as much as sector selection itself. We review whether the manager identified the opportunity early or entered after momentum had already become crowded.

Ongoing Portfolio Monitoring: Sector cycles can shift because of policy changes, valuation expansion, global events, or earnings slowdowns. Allocation review at Ckredence does not stop after deployment.

Investor Suitability Alignment: Allocation sizing, liquidity needs, risk tolerance, and investment horizon matter before any sector PMS selection. A ₹50 lakh aggressive allocation may suit one investor and create excessive concentration for another.

What Ckredence Evaluates | Why It Matters for Sector PMS |

Maximum historical drawdown | Reveals strategy behaviour during sector corrections, not just rallies |

Rolling 3-year returns | Removes single-cycle dependency from the comparison |

Exit discipline documentation | Confirms the manager has a trigger, not just a trailing return story |

Entry timing analysis | Identifies whether past returns came from skill or late-cycle momentum |

Investor suitability mapping | Aligns concentration level with the investor's actual risk capacity |

Ckredence Wealth is SEBI Registered (INP000007164) with ₹805 crore-plus in Assets Under Management, 376 active HNI clients, and a 37-year advisory legacy since 1987, with offices in Surat, Mumbai, and Vadodara.

If you are managing ₹50 lakh or above and want a sector allocation built around your risk profile and tax situation, schedule a structured advisory conversation with Ckredence Wealth.

Conclusion

Sector-based PMS strategies can deliver strong returns during the right market cycle. The problem is that most investors evaluate them at the wrong point in that cycle, using return data that reflects peak performance rather than full-cycle risk.

The best sector-based PMS in India for any HNI is the one that fits their risk tolerance, entry timing, concentration comfort, and long-term financial structure, not the one with the highest recent trailing return. If the manager cannot explain drawdown history, exit discipline, and investor suitability in clear terms, the strategy is not ready for evaluation.

01.

What does SEBI registration mean for investors choosing a sector PMS in India?

SEBI registration confirms that the PMS manager operates under regulated disclosure, reporting, and compliance requirements. It does not protect investors from concentration risk or poor sector timing. Investors should verify registration status and then evaluate drawdown history and rotation discipline separately.

02.

How is sector PMS different from thematic PMS and diversified PMS?

Sector PMS concentrates capital within one or two specific industries such as BFSI or manufacturing. Thematic PMS combines multiple sectors under a broader macro narrative. Diversified PMS allocates across a wider range of industries with lower concentration risk per sector.

03.

Who should not invest in a sector-based PMS in India?

Investors below ₹50 lakh deployable surplus, first-time PMS investors, and those seeking stable moderate returns with lower volatility are generally not suited for concentrated sector mandates. Sector PMS fits experienced HNIs who can hold through drawdown phases and understand sector cycle risks.

04.

How does Ckredence evaluate a sector PMS before recommending to HNI?

Ckredence reviews maximum historical drawdown, entry timing relative to sector cycle phase, rolling 3-year return consistency, exit discipline documentation, and investor suitability alignment. The evaluation starts with suitability and ends with allocation logic, not the other way around.

India's PMS industry crossed ₹35 lakh crore in assets under management in early 2025, up from ₹32.1 lakh crore in January 2024, with manufacturing, defence, BFSI, and green energy themes driving the fastest inflows.

Sector-based PMS strategies have moved from niche allocations to mainstream HNI conversations, driven by concentrated return cycles that look compelling in marketing presentations but carry risks that 1-year CAGR figures do not capture.

For investors deploying ₹50 lakh or more, PMS client numbers grew 27% in 2025, reflecting genuine appetite for personalised, strategy-led wealth management. Choosing the best sector-based PMS in India is no longer about identifying which theme is performing now.

It is about understanding concentration risk, sector rotation discipline, drawdown control, and manager decision-making quality across full market cycles, including the ones that turn against the strategy.

Key Takeaways

Sector PMS concentrates capital within specific industries, unlike diversified or thematic mandates

Return data from sector PMS is structurally cycle-dependent and often compared at peak timing

Maximum historical drawdown matters more than 1-year CAGR in concentrated strategies

Sector rotation discipline, not stock selection alone, determines multi-cycle performance consistency

Manufacturing, BFSI, and defence dominated sector PMS inflows across 2024 and 2025

Fee structures in concentrated PMS strategies become more visible during weaker market phases

Investor suitability, risk tolerance, and liquidity needs must precede any sector allocation decision

What Is a Sector-Based PMS in India?

A sector-based PMS in India is a SEBI-regulated discretionary portfolio management strategy that concentrates investments within selected sectors or themes instead of spreading exposure across the broader market.

Unlike diversified PMS portfolios, sector PMS mandates take intentional concentrated positions in sectors where the manager sees long-term structural opportunity. For HNI investors, this creates the possibility of stronger returns during strong sector cycles, and sharper drawdowns when the sector turns.

Understanding the differences across our guide to types of portfolio management services helps investors select the mandate structure that fits their actual risk profile.

Sector PMS vs Diversified PMS vs Thematic PMS

Type | Focus | Portfolio Structure | Risk Level | Best Fit |

Sector-Based PMS | One or few sectors | Concentrated | High | Experienced HNIs |

Diversified PMS | Multi-sector allocation | Broad exposure | Moderate | Long-term investors |

Thematic PMS | Macro theme-based | Cross-sector thematic | Moderate to High | Theme-specific investors |

Sector PMS vs Thematic PMS: Is There a Difference?

Sector PMS focuses on industries like BFSI, manufacturing, or technology. Thematic PMS combines multiple sectors under one broader narrative such as digitisation, defence, or green energy.

The structural distinction matters because thematic PMS typically carries lower concentration risk by spreading across related but distinct industries.

Which Sectors Do PMS Managers Concentrate In?

Most sector-focused PMS managers in India currently allocate within manufacturing, BFSI, technology, defence, consumption, green energy, and specialty chemicals. Each carries its own return cycle, volatility pattern, and macro dependency.

Manufacturing strategies benefit from India's capex cycle and PLI growth. BFSI strategies focus on credit expansion and financialisation trends. Defence strategies target government spending and domestic production mandates.

Green energy and specialty chemicals strategies track global supply chain shifts and energy transition capital flows.

SEBI-regulated PMS managers operate under disclosure and reporting requirements, but sector PMS portfolios still carry considerably higher concentration risk compared to diversified mandates, regardless of platform or track record.

"Risk comes from not knowing what you're doing." Warren Buffett, Chairman and CEO, Berkshire Hathaway

Source: Berkshire Hathaway Shareholder Letters

Most Sector PMS Return Data Is Built to Mislead Investors

Most investors evaluating the best sector-based PMS in India are comparing peak-cycle numbers without knowing it. A manufacturing-focused PMS delivering 38-42% returns after a sector rally looks compelling on a presentation slide.

What rarely gets discussed is what happened before the rally began or after the cycle reversed.

Sector PMS returns are highly cycle-dependent. A strategy can look exceptional during one phase and underperform sharply once momentum weakens. Several BFSI and manufacturing-heavy strategies generated 40%+ returns during FY24-FY25.

Investors who entered near cycle peaks experienced meaningful drawdowns once sector momentum slowed. The problem was not stock selection. It was timing, entry point, and concentration.

The Right Metrics to Evaluate Instead

Weak Metric | Better Metric |

1-Year CAGR | Rolling 3-Year Return |

Peak Return Snapshot | Drawdown Recovery Speed |

Marketing CAGR | Risk-Adjusted Return |

Sector Momentum | Exit Discipline |

What a Sector PMS Should Show You Before You Invest

A transparent PMS manager should explain maximum historical drawdown, recovery period after sector corrections, rolling performance across full market cycles, and exit discipline during sector reversals.

Our guide to portfolio management strategies covers the framework used to evaluate these dimensions before any allocation decision. Without that information, the investor is evaluating returns without understanding the risk structure behind the strategy.

📊 India's PMS AUM crossed ₹35 lakh crore in early 2025, up from ₹32.1 lakh crore in January 2024: Manufacturing, defence, and BFSI sector strategies attracted the highest concentrated inflows across this period. Source: Storifynews citing SEBI Data, October 2025

💼 If a sector PMS manager cannot show you maximum drawdown history and exit discipline from a previous correction cycle, the evaluation is incomplete. Talk to a Ckredence advisor for a risk-adjusted sector PMS review covering drawdown history, rolling returns, and investor suitability.

How Sector-Based PMS Works: Concentration, Rotation, and Exit Discipline

Sector PMS works differently from diversified mandates because allocation decisions concentrate capital around sector conviction rather than spreading risk across industries.

Understanding the process behind that concentration separates an informed allocation from a return-chasing decision. Our guide to the 5 phases of portfolio management explains how each phase applies to concentrated sector mandates specifically.

1. Entry Trigger

Managers identify sectors where valuations, earnings growth, policy support, or economic cycles create a clear opportunity.

Entry should come before momentum becomes crowded, not after trailing returns have already attracted flows.

2. Position Sizing

Capital is allocated aggressively toward high-conviction sectors rather than spreading exposure evenly.

This is where concentration risk becomes a structural feature of the strategy, not a temporary condition.

3. Sector Monitoring

Managers continuously review earnings, policy changes, valuations, and institutional flows.

The monitoring phase determines whether the sector thesis remains intact or whether rotation is warranted.

4. Exit Discipline

Positions are reduced or exited when valuations become excessive or sector momentum weakens.

Strong sector PMS managers define exit thresholds before volatility appears. Weak managers react after drawdowns have already compounded.

5. Reporting and Review

Investors receive portfolio statements, sector allocation visibility, and periodic commentary.

Reporting quality is a direct signal of manager transparency and is worth evaluating before any capital is deployed.

The Role of Drawdown Limits in Sector PMS Mandates

Strong sector PMS managers define exit discipline before volatility appears. If the advisor presenting a sector PMS cannot explain the drawdown trigger or exit logic from a previous cycle, the evaluation is looking at a return history, not a strategy.

"The intelligent investor is a realist who sells to optimists and buys from pessimists." Benjamin Graham, Author, The Intelligent Investor

Source: The Intelligent Investor, Revised Edition, HarperCollins

What Has Changed in Sector-Based PMS in India in 2026

Sector leadership shifted sharply between FY25 and FY26. Manufacturing and capital expenditure themes dominated PMS conversations in FY25, while IT-focused strategies struggled through parts of FY26 due to slower earnings momentum and delayed sector rotation.

Sector | FY25 Return Trend | FY26 Trend | Manager Positioning |

Manufacturing | Strong outperformance | Stable | Aggressive overweight |

BFSI | Consistent | Positive | Broad allocation |

Technology | Mixed | Underperformance | Rotation challenges |

Defence | Strong momentum | High volatility | Tactical exposure |

Green Energy | Momentum-driven | Selective | Theme-based allocation |

The IT Correction Revealed Manager Skill Differences

Some PMS managers remained overweight technology even after earnings momentum weakened. Others rotated earlier into manufacturing, BFSI, or defence-linked themes.

This difference in sector rotation discipline became visible quickly in portfolio performance across the year. The divergence confirmed that sector PMS outcomes depend heavily on rotation logic, not just initial theme selection.

New Themes Emerging in 2026

Thematic allocation conversations are now expanding toward defence manufacturing, green energy infrastructure, specialty chemicals, domestic manufacturing, and financialisation themes. The challenge is no longer identifying the theme.

It is identifying which managers rotate out before the cycle weakens.

📊 Defence-focused PMS strategies saw 30-35% inflows growth in the first half of 2025 alone: Government defence spending and the Make in India push drove concentrated sector allocation into listed defence companies.

Source: Storifynews citing SEBI and APMI Data, October 2025

📋 High inflows into a sector PMS after a strong return cycle often signals late entry risk, not opportunity. Request a structured sector allocation review from Ckredence Wealth before adding concentration to any sector theme.

How to Choose the Best Sector-Based PMS in India: 5 Criteria Most Investors Never Check

Most investors compare sector PMS strategies using CAGR alone. Choosing the right sector PMS requires evaluating drawdown discipline, rolling returns, rotation logic, manager transparency, and full fee structures across market cycles, not just the headline return from the strongest phase.

Criterion | What Good Looks Like | Red Flag | Question to Ask |

Drawdown Control | Controlled corrections | Deep unrecovered losses | What was the maximum drawdown? |

Rolling Returns | Consistent multi-cycle performance | One-cycle dependence | How did returns behave across 3Y rolling periods? |

Sector Rotation Discipline | Early exits during reversals | Late-cycle holding | How do you decide exits? |

Manager Transparency | Clear reporting across cycles | Performance-only communication | How often are portfolio reviews shared? |

Fee Structure | Transparent total cost model | Hidden cost layering | What is the total cost structure? |

What a Good Sector PMS Track Record Looks Like

A strong sector PMS track record should show manageable drawdowns, reasonable recovery speed after market downturns, consistent performance across different market environments, and disciplined communication during both strong and weak market periods.

Our guide to how to invest in portfolio management services covers the 8-step evaluation process HNIs should follow before deploying capital into any PMS strategy, including sector-concentrated mandates.

Fee Structures Matter More Than Most Investors Realise

In concentrated PMS strategies, fees become more visible during weaker market cycles. A 2025 investor review found that fewer than 20% of HNI investors asked about maximum drawdown before deploying capital into IT-heavy sector strategies.

Those who ignored drawdown analysis experienced meaningful portfolio erosion during the correction phase.

🔍 Most sector PMS comparisons stop at the 3-year return table without asking what the drawdown looked like before the rally began. Book a structured sector PMS evaluation with Ckredence Wealth and compare your shortlist on risk-adjusted terms before deploying.

Best Sector-Based PMS in India 2026

The best sector-based PMS in India depends less on recent returns and more on investor suitability, concentration tolerance, and manager discipline across full market cycles.

PMS Strategy | Investment Philosophy | Return Profile | Drawdown Profile | Best-Fit Investor |

Aditya Birla Select Sector Portfolio | Sector rotation focus | Moderate | Moderate | Tactical allocation seekers |

Ckredence Wealth PMS Strategies | Risk-adjusted sector allocation with active monitoring | Balanced to Growth-Oriented | Controlled | HNIs seeking advisor-led sector allocation |

Green Portfolio Super 30 Dynamic | High-conviction thematic allocation | Strong | Moderate to High | Aggressive HNIs |

ICICI Prudential Growth Leaders | Sector-leading companies | Balanced | Moderate | Long-term HNIs |

Negen Capital Special Situations and Technology | Technology and special situations | Volatile | High | High-risk tolerance investors |

Aditya Birla Select Sector Portfolio focuses on tactical sector opportunities while maintaining broader institutional portfolio discipline.

Green Portfolio Super 30 Dynamic is known for concentrated thematic exposure and aggressive sector positioning during manufacturing and growth cycles.

ICICI Prudential Growth Leaders follows a relatively balanced quality-growth approach compared to more concentrated thematic strategies.

Negen Capital Special Situations and Technology attracts investors seeking higher-growth technology and thematic opportunities with higher volatility tolerance.

Ckredence Wealth PMS Strategies approach sector allocation as a risk-management decision first and a return opportunity second.

An investor who entered Green Portfolio Super 30 Dynamic in early 2023 with ₹75 lakh saw appreciation through the manufacturing cycle.

A comparable investor concentrated heavily in weaker IT-sector exposure experienced lower returns with deeper interim volatility. The difference was not stock selection alone. It was sector rotation discipline and entry timing relative to the cycle.

Who Should Not Invest in a Sector-Based PMS in India

Sector PMS is not suitable for every investor.

Investor Profile | Sector PMS Suitability | Reason |

First-time PMS investor | Not recommended | Concentration risk may feel excessive before building experience |

Investor below ₹50 lakh deployable surplus | Not recommended | Allocation risk becomes disproportionately high at smaller corpus |

Long-term HNI with diversified wealth base | Suitable | Better ability to absorb sector volatility across a full portfolio |

Investor seeking stable moderate returns | Not recommended | Diversified PMS structures may be more appropriate |

When Diversified PMS Makes More Sense

Investors who prefer smoother volatility, lack sector-specific understanding, cannot absorb sharp drawdowns, or prefer broader market participation may find that diversified PMS structures suit their profile better than concentrated sector mandates.

Our overview of types of portfolio management services covers how discretionary, non-discretionary, and diversified structures differ in practice.

Why Ckredence Wealth for Sector-Based PMS Allocation in India

Choosing a sector PMS manager is not just about selecting the highest-return strategy.

The real challenge is understanding how the manager behaves when the sector cycle weakens, how risk is controlled during volatility, and whether the allocation matches the investor's financial profile.

At Ckredence Wealth, our PMS advisory approach treats sector allocation as a risk-management decision first and a return opportunity second.

The focus is on building sustainable long-term allocation structures for HNI investors, not chasing whichever sector performed best last year.

Drawdown Discipline Evaluation: Many PMS presentations highlight only peak returns. We evaluate how the manager handled difficult phases, corrections, and sector reversals before considering allocation suitability.

Entry Timing and Allocation Logic: Sector allocation timing matters as much as sector selection itself. We review whether the manager identified the opportunity early or entered after momentum had already become crowded.

Ongoing Portfolio Monitoring: Sector cycles can shift because of policy changes, valuation expansion, global events, or earnings slowdowns. Allocation review at Ckredence does not stop after deployment.

Investor Suitability Alignment: Allocation sizing, liquidity needs, risk tolerance, and investment horizon matter before any sector PMS selection. A ₹50 lakh aggressive allocation may suit one investor and create excessive concentration for another.

What Ckredence Evaluates | Why It Matters for Sector PMS |

Maximum historical drawdown | Reveals strategy behaviour during sector corrections, not just rallies |

Rolling 3-year returns | Removes single-cycle dependency from the comparison |

Exit discipline documentation | Confirms the manager has a trigger, not just a trailing return story |

Entry timing analysis | Identifies whether past returns came from skill or late-cycle momentum |

Investor suitability mapping | Aligns concentration level with the investor's actual risk capacity |

Ckredence Wealth is SEBI Registered (INP000007164) with ₹805 crore-plus in Assets Under Management, 376 active HNI clients, and a 37-year advisory legacy since 1987, with offices in Surat, Mumbai, and Vadodara.

If you are managing ₹50 lakh or above and want a sector allocation built around your risk profile and tax situation, schedule a structured advisory conversation with Ckredence Wealth.

Conclusion

Sector-based PMS strategies can deliver strong returns during the right market cycle. The problem is that most investors evaluate them at the wrong point in that cycle, using return data that reflects peak performance rather than full-cycle risk.

The best sector-based PMS in India for any HNI is the one that fits their risk tolerance, entry timing, concentration comfort, and long-term financial structure, not the one with the highest recent trailing return. If the manager cannot explain drawdown history, exit discipline, and investor suitability in clear terms, the strategy is not ready for evaluation.

01.

What does SEBI registration mean for investors choosing a sector PMS in India?

SEBI registration confirms that the PMS manager operates under regulated disclosure, reporting, and compliance requirements. It does not protect investors from concentration risk or poor sector timing. Investors should verify registration status and then evaluate drawdown history and rotation discipline separately.

02.

How is sector PMS different from thematic PMS and diversified PMS?

Sector PMS concentrates capital within one or two specific industries such as BFSI or manufacturing. Thematic PMS combines multiple sectors under a broader macro narrative. Diversified PMS allocates across a wider range of industries with lower concentration risk per sector.

03.

Who should not invest in a sector-based PMS in India?

Investors below ₹50 lakh deployable surplus, first-time PMS investors, and those seeking stable moderate returns with lower volatility are generally not suited for concentrated sector mandates. Sector PMS fits experienced HNIs who can hold through drawdown phases and understand sector cycle risks.

04.

How does Ckredence evaluate a sector PMS before recommending to HNI?

Ckredence reviews maximum historical drawdown, entry timing relative to sector cycle phase, rolling 3-year return consistency, exit discipline documentation, and investor suitability alignment. The evaluation starts with suitability and ends with allocation logic, not the other way around.