11min Read

11min Read

Best Investment Options for HNI in India: Where to Allocate Rs.5 Crore and Beyond

Best Investment Options for HNI in India: Where to Allocate Rs.5 Crore and Beyond

Best Investment Options for HNI in India: Where to Allocate Rs.5 Crore and Beyond

Explore the best investment options for HNI in India, from PMS and AIFs to real estate, global equities, and structured products.

Explore the best investment options for HNI in India, from PMS and AIFs to real estate, global equities, and structured products.

Explore the best investment options for HNI in India, from PMS and AIFs to real estate, global equities, and structured products.

Ckredence Wealth

Ckredence Wealth

|

India’s HNI population is expected to nearly double from about 850,000 today to 1.65 million by 2027, according to an Anarock report. Yet most first time HNIs still hold a portfolio that looks like an upgraded version of their old mutual fund SIPs, because nobody showed them what else exists once their investable assets crossed a serious threshold.

Before you assume your current portfolio is enough, ask yourself:

Do you know the difference between what a PMS, an AIF, and a structured product actually do for your money?

Is your portfolio still built the same way it was when you had a fraction of today’s investable assets?

Are you avoiding certain options simply because they sound like they are “only for the ultra-rich”?

We built this guide to walk through the best investment options for HNI in India in the order that matters, covering managed equity, private markets, real estate, and global diversification, so you can see what actually fits your stage of wealth.

TL;DR

Portfolio Management Services and Alternative Investment Funds are the two core routes once your portfolio outgrows mutual funds, each with a different SEBI-mandated minimum.

Commercial real estate and REITs offer steadier income than residential property, without requiring you to manage a physical asset.

International equities, accessed through the Liberalised Remittance Scheme, reduce your dependence on a single currency and economy.

Structured products and pre-IPO shares carry the most complexity and risk, and should stay a smaller slice of the portfolio.

Several of these routes are accessible well before the industry’s Rs.5 crore HNI threshold, not only after it.

The right mix depends on your investable corpus, risk appetite, and time horizon, not on copying someone else’s allocation.

Portfolio Management Services: The Starting Point Among Investment Options for HNI in India

For investors who want direct equity exposure managed by a professional rather than pooled fund units, Portfolio Management Services are usually the first step up from mutual funds. Each portfolio is held in the investor’s own demat account, not pooled with other clients, which gives more transparency and customization than a mutual fund.

SEBI-mandated minimum investment: Rs.50 lakh.

Portfolios can run concentrated, sector-specific, or diversified strategies depending on the manager.

Performance and holdings are visible at the individual account level, not just as a fund NAV.

MANAGED EQUITY, DONE FOR YOU |

Our PMS strategies start at the SEBI minimum and are built around your goals, not a one-size-fits-all model. |

Schedule a Consultation: ckredencewealth.com/contact-us |

Alternative Investment Funds: A Core Route Among Investment Options for HNI in India

Alternative Investment Funds pool capital into assets that sit outside listed stocks and bonds, including private equity, venture capital, and hedge strategies. They offer access to unlisted, high growth companies that public markets never see.

SEBI-mandated minimum investment: Rs.1 crore per scheme, or Rs.25 lakh for angel funds specifically.

Three categories exist. Category I funds venture capital and infrastructure, Category II covers private equity and debt, Category III runs hedge and derivative strategies.

Choosing between an AIF and a PMS depends on how much control you want, a difference we cover in PMS vs AIF.

PRIVATE MARKET ACCESS |

AIFs suit a slice of the portfolio, not the whole thing. We help size that slice against your liquidity needs and existing exposure. |

Schedule a Consultation: ckredencewealth.com/contact-us |

Commercial Real Estate and REITs: A Steady Income Option for HNI in India

Instead of a second residential flat, many HNIs now target Grade-A commercial space, warehouses, or fractional ownership platforms. These assets have historically offered higher and steadier yields, ranging from about 6 to 11 percent annually, than residential property.

Real Estate Investment Trusts (REITs) offer similar exposure with listed-market liquidity, unlike a physical property.

Whether direct or via REITs, real estate should sit inside a wider asset allocation plan, not stand alone.

Fractional ownership platforms lower the entry ticket but add platform and liquidity risk to evaluate.

INCOME WITHOUT THE HASSLE |

Direct commercial property, REITs, or fractional platforms all play different roles. We help you pick the structure that matches how hands-on you want to be. |

Schedule a Consultation: ckredencewealth.com/contact-us |

International Equities: Global Diversification Among Investment Options for HNI in India

To reduce dependence on the rupee and Indian markets alone, many HNIs allocate a portion of their portfolio abroad using the Reserve Bank of India’s Liberalised Remittance Scheme (LRS). This also opens access to global sectors that are thin or absent on Indian exchanges.

A common allocation range is 10 to 20 percent of the total portfolio, though this varies by investor.

LRS currently permits remittances up to USD 250,000 per financial year for eligible investments.

This exposure works best as part of a defined mix across our investment approaches, not as a standalone bet on one region.

BEYOND ONE CURRENCY |

Global allocation only helps if it is sized correctly against your rupee liabilities and goals. We build that into the full plan, not as an afterthought. |

Schedule a Consultation: ckredencewealth.com/contact-us |

Structured Products and Pre-IPO Shares: Higher Complexity Investment Options for HNI in India

Structured Products and Market-Linked Debentures (MLDs) are customized, fixed income instruments that track a benchmark index or G-Sec yield, offering a defined payoff rather than an open-ended market return. Angel investing and pre-IPO shares sit at the opposite end, offering early access to unlisted companies before they list, at a much higher risk.

MLDs suit investors who want tax-efficient, benchmark-linked returns without full equity market volatility.

Pre-IPO and angel positions typically require spreading capital across 8 to 10 companies to manage the risk of any single failure.

Both options work best as a smaller, clearly bounded slice of an otherwise diversified portfolio.

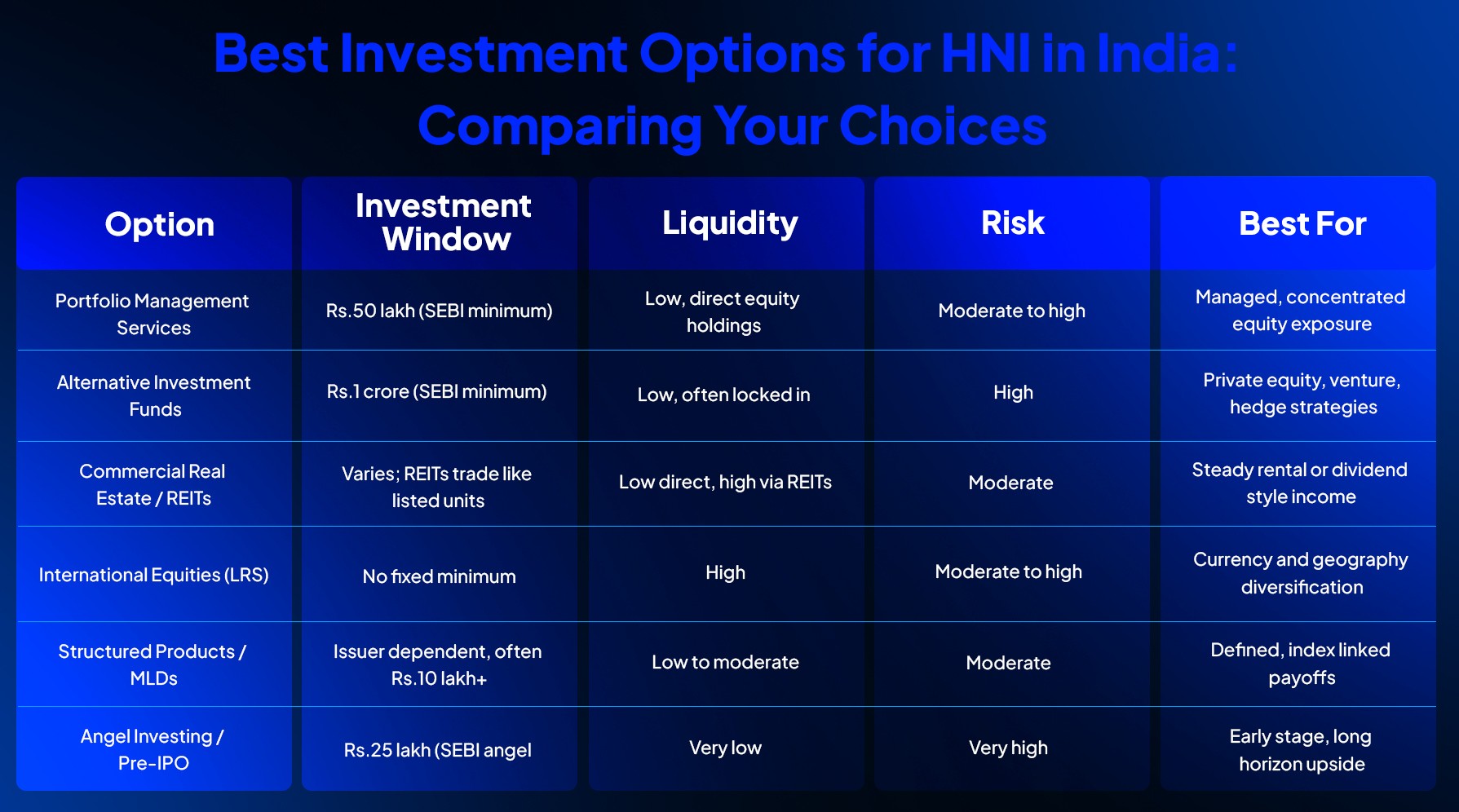

Best Investment Options for HNI in India: Comparing Your Choices

A side by side view makes the trade off clear.

Table: how each investment option for HNI in India compares on ticket size, liquidity, and risk.

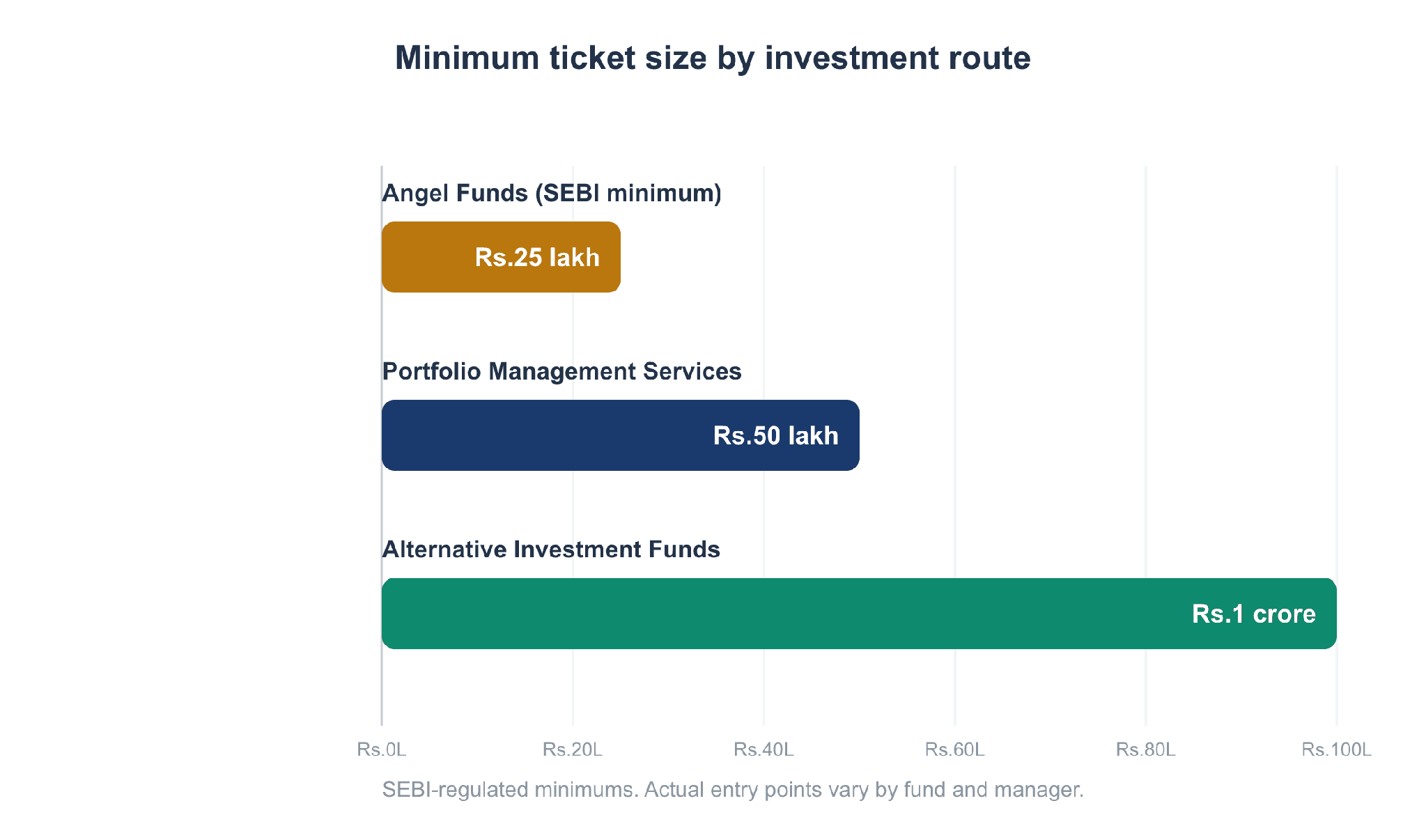

Minimum ticket size is often the first filter investors apply. The chart below places three SEBI-regulated minimums side by side.

SEBI-mandated minimum investment across three core routes.

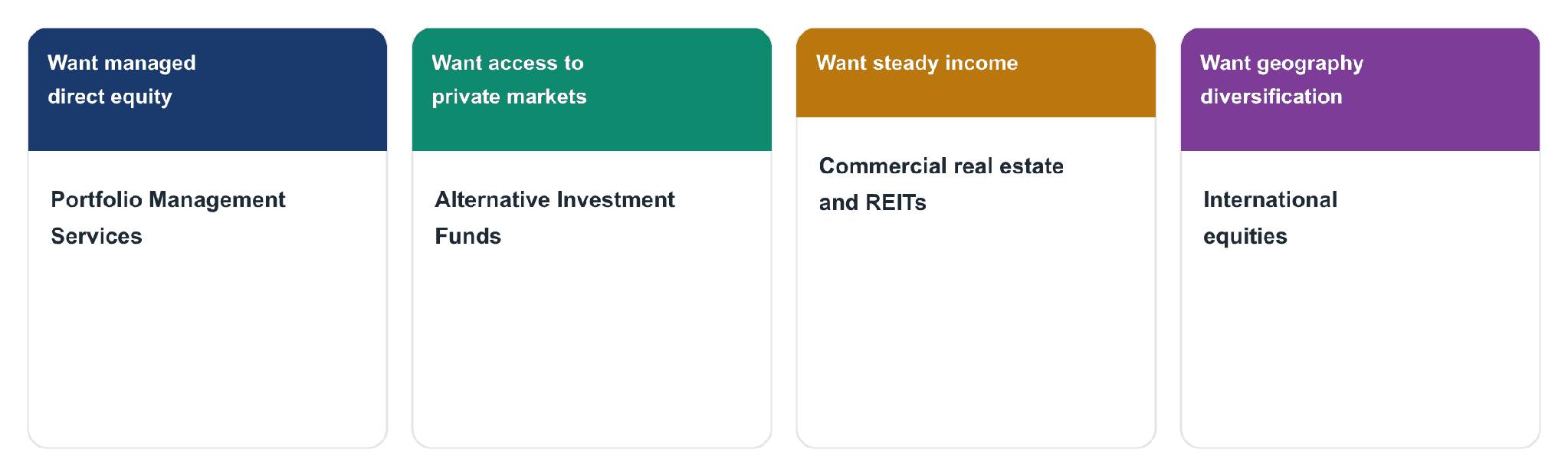

Ticket size is only one filter. Use the goal map below to match your priority to the right option.

Match your goal to the right investment option for HNI in India.

Why Should You Choose Ckredence Wealth?

You do not need to wait until you cross the industry’s Rs.5 crore HNI threshold to invest like one. Ckredence Wealth is a SEBI registered investment advisor (INA000020846) and portfolio manager (INP000007164), built on a 37 year legacy since 1987, working with investors from their first Rs.50 lakh onward.

Solutions That Matter:

PMS access at the SEBI entry point, through our 4 investment approaches.

Fee only advisory below the PMS threshold, through our RIA services.

Structured planning for larger payouts, through our HNI investment planning services.

Ready to transform your investment approach? Schedule a Consultation!

Conclusion

The best investment options for HNI in India are not one product but a set of tools, each built for a different job. PMS and AIFs extend your equity exposure beyond mutual funds, real estate and REITs add income that does not move in lockstep with the stock market, and international equities reduce dependence on a single currency and economy.

None of these choices should be copied wholesale from someone else’s portfolio. The right mix depends on your investable corpus, risk appetite, and time horizon, and several of these routes are accessible well before you formally cross into HNI territory. Building that allocation early matters more than waiting for a round number.

FAQs

01.

What is the minimum investment to be considered an HNI in India?

The industry standard is Rs.5 crore or more in investable assets, though some regulatory contexts use different thresholds for specific products.

02.

What is the difference between PMS and AIF for HNI investors?

PMS holds securities in your own demat account with a Rs.50 lakh minimum, while an AIF pools capital into private market strategies with a Rs.1 crore minimum.

03.

How much of an HNI portfolio should go into international equities?

A common range is 10 to 20 percent of the total portfolio, allocated through the Liberalised Remittance Scheme, though the right figure varies by investor.

04.

Is real estate still a good investment option for HNI in India?

Commercial real estate and REITs can offer steady yields between roughly 6 and 11 percent, but they work best balanced against more liquid options in the portfolio.

India’s HNI population is expected to nearly double from about 850,000 today to 1.65 million by 2027, according to an Anarock report. Yet most first time HNIs still hold a portfolio that looks like an upgraded version of their old mutual fund SIPs, because nobody showed them what else exists once their investable assets crossed a serious threshold.

Before you assume your current portfolio is enough, ask yourself:

Do you know the difference between what a PMS, an AIF, and a structured product actually do for your money?

Is your portfolio still built the same way it was when you had a fraction of today’s investable assets?

Are you avoiding certain options simply because they sound like they are “only for the ultra-rich”?

We built this guide to walk through the best investment options for HNI in India in the order that matters, covering managed equity, private markets, real estate, and global diversification, so you can see what actually fits your stage of wealth.

TL;DR

Portfolio Management Services and Alternative Investment Funds are the two core routes once your portfolio outgrows mutual funds, each with a different SEBI-mandated minimum.

Commercial real estate and REITs offer steadier income than residential property, without requiring you to manage a physical asset.

International equities, accessed through the Liberalised Remittance Scheme, reduce your dependence on a single currency and economy.

Structured products and pre-IPO shares carry the most complexity and risk, and should stay a smaller slice of the portfolio.

Several of these routes are accessible well before the industry’s Rs.5 crore HNI threshold, not only after it.

The right mix depends on your investable corpus, risk appetite, and time horizon, not on copying someone else’s allocation.

Portfolio Management Services: The Starting Point Among Investment Options for HNI in India

For investors who want direct equity exposure managed by a professional rather than pooled fund units, Portfolio Management Services are usually the first step up from mutual funds. Each portfolio is held in the investor’s own demat account, not pooled with other clients, which gives more transparency and customization than a mutual fund.

SEBI-mandated minimum investment: Rs.50 lakh.

Portfolios can run concentrated, sector-specific, or diversified strategies depending on the manager.

Performance and holdings are visible at the individual account level, not just as a fund NAV.

MANAGED EQUITY, DONE FOR YOU |

Our PMS strategies start at the SEBI minimum and are built around your goals, not a one-size-fits-all model. |

Schedule a Consultation: ckredencewealth.com/contact-us |

Alternative Investment Funds: A Core Route Among Investment Options for HNI in India

Alternative Investment Funds pool capital into assets that sit outside listed stocks and bonds, including private equity, venture capital, and hedge strategies. They offer access to unlisted, high growth companies that public markets never see.

SEBI-mandated minimum investment: Rs.1 crore per scheme, or Rs.25 lakh for angel funds specifically.

Three categories exist. Category I funds venture capital and infrastructure, Category II covers private equity and debt, Category III runs hedge and derivative strategies.

Choosing between an AIF and a PMS depends on how much control you want, a difference we cover in PMS vs AIF.

PRIVATE MARKET ACCESS |

AIFs suit a slice of the portfolio, not the whole thing. We help size that slice against your liquidity needs and existing exposure. |

Schedule a Consultation: ckredencewealth.com/contact-us |

Commercial Real Estate and REITs: A Steady Income Option for HNI in India

Instead of a second residential flat, many HNIs now target Grade-A commercial space, warehouses, or fractional ownership platforms. These assets have historically offered higher and steadier yields, ranging from about 6 to 11 percent annually, than residential property.

Real Estate Investment Trusts (REITs) offer similar exposure with listed-market liquidity, unlike a physical property.

Whether direct or via REITs, real estate should sit inside a wider asset allocation plan, not stand alone.

Fractional ownership platforms lower the entry ticket but add platform and liquidity risk to evaluate.

INCOME WITHOUT THE HASSLE |

Direct commercial property, REITs, or fractional platforms all play different roles. We help you pick the structure that matches how hands-on you want to be. |

Schedule a Consultation: ckredencewealth.com/contact-us |

International Equities: Global Diversification Among Investment Options for HNI in India

To reduce dependence on the rupee and Indian markets alone, many HNIs allocate a portion of their portfolio abroad using the Reserve Bank of India’s Liberalised Remittance Scheme (LRS). This also opens access to global sectors that are thin or absent on Indian exchanges.

A common allocation range is 10 to 20 percent of the total portfolio, though this varies by investor.

LRS currently permits remittances up to USD 250,000 per financial year for eligible investments.

This exposure works best as part of a defined mix across our investment approaches, not as a standalone bet on one region.

BEYOND ONE CURRENCY |

Global allocation only helps if it is sized correctly against your rupee liabilities and goals. We build that into the full plan, not as an afterthought. |

Schedule a Consultation: ckredencewealth.com/contact-us |

Structured Products and Pre-IPO Shares: Higher Complexity Investment Options for HNI in India

Structured Products and Market-Linked Debentures (MLDs) are customized, fixed income instruments that track a benchmark index or G-Sec yield, offering a defined payoff rather than an open-ended market return. Angel investing and pre-IPO shares sit at the opposite end, offering early access to unlisted companies before they list, at a much higher risk.

MLDs suit investors who want tax-efficient, benchmark-linked returns without full equity market volatility.

Pre-IPO and angel positions typically require spreading capital across 8 to 10 companies to manage the risk of any single failure.

Both options work best as a smaller, clearly bounded slice of an otherwise diversified portfolio.

Best Investment Options for HNI in India: Comparing Your Choices

A side by side view makes the trade off clear.

Table: how each investment option for HNI in India compares on ticket size, liquidity, and risk.

Minimum ticket size is often the first filter investors apply. The chart below places three SEBI-regulated minimums side by side.

SEBI-mandated minimum investment across three core routes.

Ticket size is only one filter. Use the goal map below to match your priority to the right option.

Match your goal to the right investment option for HNI in India.

Why Should You Choose Ckredence Wealth?

You do not need to wait until you cross the industry’s Rs.5 crore HNI threshold to invest like one. Ckredence Wealth is a SEBI registered investment advisor (INA000020846) and portfolio manager (INP000007164), built on a 37 year legacy since 1987, working with investors from their first Rs.50 lakh onward.

Solutions That Matter:

PMS access at the SEBI entry point, through our 4 investment approaches.

Fee only advisory below the PMS threshold, through our RIA services.

Structured planning for larger payouts, through our HNI investment planning services.

Ready to transform your investment approach? Schedule a Consultation!

Conclusion

The best investment options for HNI in India are not one product but a set of tools, each built for a different job. PMS and AIFs extend your equity exposure beyond mutual funds, real estate and REITs add income that does not move in lockstep with the stock market, and international equities reduce dependence on a single currency and economy.

None of these choices should be copied wholesale from someone else’s portfolio. The right mix depends on your investable corpus, risk appetite, and time horizon, and several of these routes are accessible well before you formally cross into HNI territory. Building that allocation early matters more than waiting for a round number.

FAQs

01.

What is the minimum investment to be considered an HNI in India?

The industry standard is Rs.5 crore or more in investable assets, though some regulatory contexts use different thresholds for specific products.

02.

What is the difference between PMS and AIF for HNI investors?

PMS holds securities in your own demat account with a Rs.50 lakh minimum, while an AIF pools capital into private market strategies with a Rs.1 crore minimum.

03.

How much of an HNI portfolio should go into international equities?

A common range is 10 to 20 percent of the total portfolio, allocated through the Liberalised Remittance Scheme, though the right figure varies by investor.

04.

Is real estate still a good investment option for HNI in India?

Commercial real estate and REITs can offer steady yields between roughly 6 and 11 percent, but they work best balanced against more liquid options in the portfolio.