13min Read

13min Read

Alternative to Fixed Deposit: Where to Invest When FD Rates Fall

Alternative to Fixed Deposit: Where to Invest When FD Rates Fall

Alternative to Fixed Deposit: Where to Invest When FD Rates Fall

Compare the best alternative to fixed deposit options in India, from government schemes to debt funds, liquid funds, and corporate bonds.

Compare the best alternative to fixed deposit options in India, from government schemes to debt funds, liquid funds, and corporate bonds.

Compare the best alternative to fixed deposit options in India, from government schemes to debt funds, liquid funds, and corporate bonds.

Ckredence Wealth

Ckredence Wealth

|

Many investors renew a fixed deposit out of habit, only to watch the rate on offer shrink a little more each time. Bank deposits still hold the largest share of household financial savings in India, yet a representative SBI fixed deposit now pays 6.25 percent to 6.40 percent for a one to three year tenure, a rate that keeps sliding as the RBI eases policy through 2026.

The real frustration is rarely the rate alone. It is not knowing where else that money can go without losing the safety it was set aside for, and not trusting a relationship manager whose incentive is the product that pays the highest commission. Before you renew another FD, ask:

Are you renewing an FD because it is genuinely right for you, or because you have never compared it against a real alternative?

Has a bank or agent ever pushed you toward a product that paid them more than it helped you?

Do you know how much of your surplus should stay liquid, and how much can chase a better post tax return?

We built this guide to help you move past that hesitation. It compares the four most reliable alternative to fixed deposit options by return, risk, and liquidity, so you can match the right one to your goal, not to what pays your bank the most.

TL;DR

Government schemes like the PPF and RBI bonds carry a sovereign backing, making them the safest alternative to fixed deposit.

Debt mutual funds can beat FD returns while staying far more liquid than a locked in deposit.

Liquid funds settle in a day or two, which suits money you might need on short notice.

Corporate bonds pay a higher coupon than FD, but the extra yield comes with credit risk.

The right alternative to fixed deposit depends on your time horizon, not just the rate on offer.

Spreading money across two or three of these options often works better than picking just one.

Government Schemes and Bonds: The Safest Alternative to Fixed Deposit

For investors who want to stay safe, government backed schemes are the first alternative to fixed deposit worth considering, especially if you are working toward an early retirement beyond fixed deposits. The Public Provident Fund and National Savings Certificate carry a sovereign guarantee and Section 80C benefit, unlike a bank FD.

RBI Floating Rate Savings Bonds and government securities bought through the RBI Retail Direct portal add another layer of choice. Placed correctly within your asset allocation, their returns reset with market rates, so they hold up even as FD rates keep falling.

Public Provident Fund: 15 year lock in, tax free interest, Section 80C eligible.

RBI Floating Rate Bonds: 7 year tenure, rate resets twice a year.

Government securities: buy directly through RBI Retail Direct, no broker required.

These instruments trade flexibility for safety. If you want steadier growth with easier access to your money, the next option fits better.

FOR SAFETY FIRST ALLOCATIONS |

Not sure how much of your surplus belongs in government schemes versus market linked options? Our SEBI registered RIA team builds a fee-only allocation plan around your goals, not a product target. |

Schedule a Consultation: ckredencewealth.com/contact-us |

Debt Mutual Funds: A Flexible Alternative to Fixed Deposit

Debt mutual funds are a flexible alternative to fixed deposit for investors who still want low volatility returns. Unlike equity focused mutual funds, the fund pools your money into government securities, corporate debt, and money market instruments.

Unlike an FD, you are not locked into one rate for the full tenure. The fund manager can shift between shorter and longer duration paper as interest rates move.

Short duration and corporate bond funds suit a one to three year horizon.

Returns move with the rate cycle and are not fixed in advance.

Exit is usually available within a day or two, unlike an early FD withdrawal.

Debt funds work well when you want your money to stay reasonably close while still chasing a better post tax return.

DEBT FUND SELECTION |

Choosing between short duration, corporate bond, and money market debt funds gets easier with a plan matched to your time horizon and tax bracket. |

Explore Mutual Fund Advisory: ckredencewealth.com/mutual-funds |

Liquid Funds: The Fastest Alternative to Fixed Deposit for Short Term Money

When you need money on short notice, liquid funds are a practical alternative to fixed deposit. They invest in instruments maturing within 91 days, which keeps volatility low.

Most liquid funds settle in T+1, and many platforms allow instant redemption up to a set limit. That is often faster than the notice period a bank asks for on premature FD withdrawal.

Well suited to emergency funds and short term business surplus.

Credit risk stays low because holdings mature quickly.

Returns track short term rates, not a fixed FD coupon.

If your money needs to stay ready for use, a liquid fund protects that flexibility better than a locked in deposit.

LIQUIDITY PLANNING |

Emergency funds and short term business surplus need a structure, not a guess. We help you size the liquid bucket correctly against your full portfolio. |

Schedule a Consultation: ckredencewealth.com/contact-us |

Corporate Bonds: A Higher Yield Alternative to Fixed Deposit

For investors willing to accept some credit risk, corporate bonds are a higher yield alternative to fixed deposit. Companies issue these bonds to raise capital, and rating agencies grade them from AAA down to below investment grade.

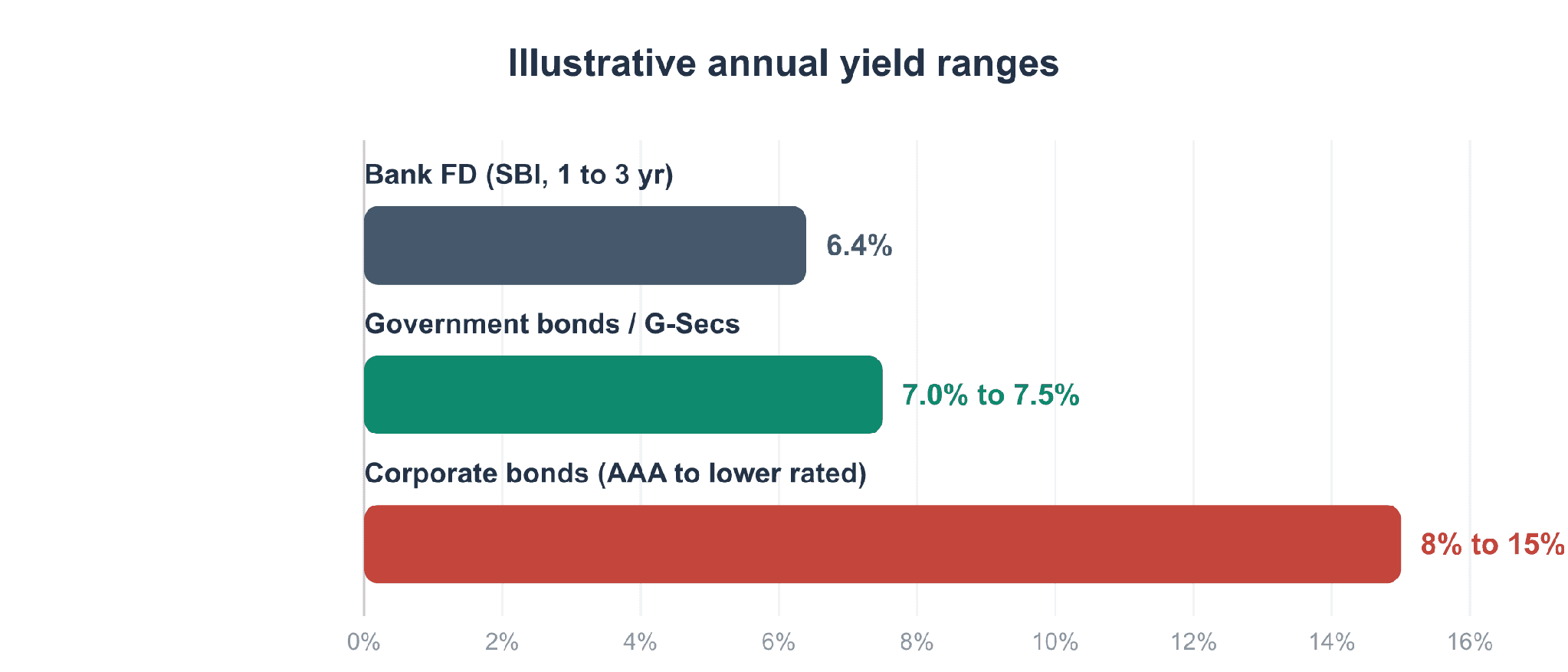

Corporate bond yields have ranged from about 8 percent to 15 percent (GoldenPi), depending on the issuer’s rating. A higher rated bond pays closer to FD levels with a wider safety margin, while a lower rated bond pays more but carries real default risk, which is why sound bond portfolio strategy starts with credit quality, not coupon.

AAA rated bonds suit conservative investors who still want a bit more than FD.

Interest is usually paid on a fixed schedule, similar to an FD payout.

Bonds can be sold on the exchange before maturity, subject to market price.

Corporate bonds work best when you study the issuer’s credit quality first, not just the coupon on offer.

CREDIT RISK, VETTED |

A higher coupon means nothing if the issuer cannot pay it back. Our team screens credit quality before any bond enters a client portfolio. |

Explore Portfolio Management: ckredencewealth.com/pms |

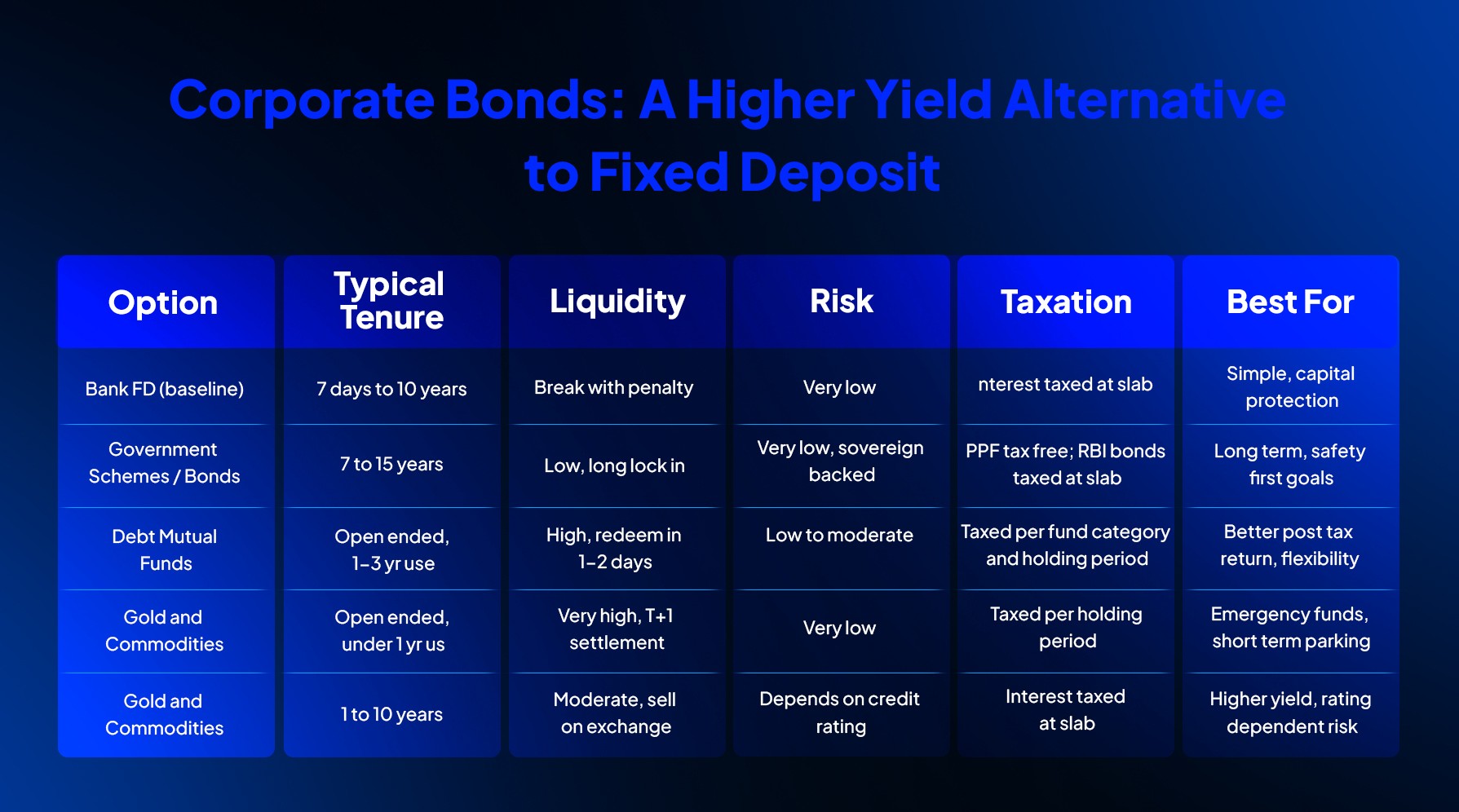

Alternative to Fixed Deposit: Comparing Your Options

A side by side view makes the trade off clear.

Table: how each alternative to fixed deposit compares on tenure, liquidity, risk, and taxation.

Taxation is often the deciding factor once returns look similar. Understanding how mutual fund and PMS taxation works before you invest avoids an unpleasant surprise at redemption. Here is how the sourced yield ranges for three of these options compare against a current bank FD.

Indicative ranges only, not a return promise. Rates move with markets and issuer credit quality.

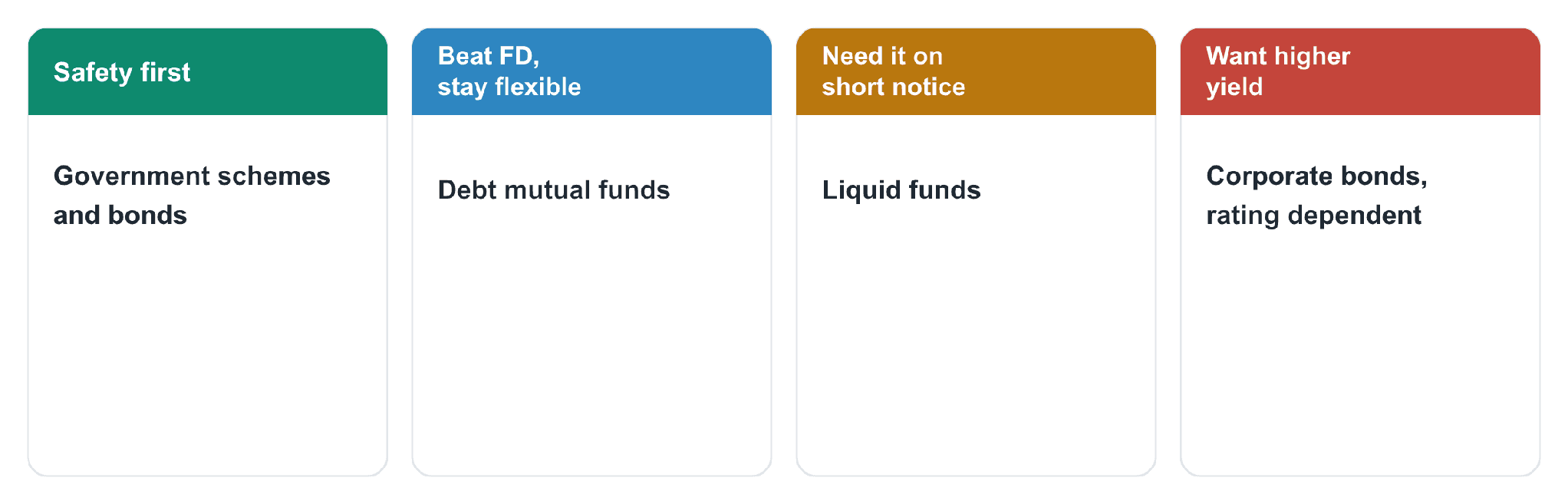

Debt mutual funds and liquid funds are not charted here because both are open ended, and their return depends on the prevailing rate cycle rather than a fixed coupon. Use the goal map below to place them correctly against your own need.

Match your goal to the right alternative to fixed deposit.

Why Should You Choose Ckredence Wealth?

Moving beyond an FD is easier with guidance that fits your goals, not a product pitch. Ckredence Wealth is a SEBI registered investment advisor (INA000020846) and portfolio manager (INP000007164), built on a 37 year legacy since 1987.

Solutions That Matter:

Fee only advice that matches each alternative to fixed deposit against your time horizon and risk appetite, through our RIA services.

Access to debt, bond, and equity strategies under one advisory relationship, across our investment approaches.

Ongoing review as interest rates and your goals change.

Ready to transform your investment approach? Schedule a Consultation!

Conclusion

An alternative to fixed deposit is not about giving up safety. It is about matching the right instrument to how soon you need the money and how much risk you can accept. Government schemes protect capital, debt funds add flexibility, liquid funds cover short notice needs, and corporate bonds raise the yield for investors who understand credit risk.

The investors who benefit most are the ones who stop renewing an FD out of habit and start reviewing it as one option among several. Keep emergency money liquid, use government schemes for long term safety, and add debt funds or bonds only once you understand what backs the return. A mix built around your goals will outperform a single instrument chosen out of comfort.

FAQs

01.

What is the best alternative to fixed deposit for safety?

Government schemes such as the PPF and RBI Floating Rate Bonds carry a sovereign guarantee, making them the safest alternative to fixed deposit available today.

02.

Can debt mutual funds lose value the way FDs never do?

Yes. Debt fund returns move with interest rates and are not fixed, unlike the rate locked in at FD opening.

03.

Which alternative to fixed deposit suits emergency funds best?

Liquid funds suit emergency money best, since they settle in T+1 and invest in instruments maturing within 91 days.

04.

Are corporate bonds safer than fixed deposits?

Not always. Corporate bonds pay a higher coupon but carry credit risk tied to the issuing company, so the credit rating matters more than the headline rate.

Many investors renew a fixed deposit out of habit, only to watch the rate on offer shrink a little more each time. Bank deposits still hold the largest share of household financial savings in India, yet a representative SBI fixed deposit now pays 6.25 percent to 6.40 percent for a one to three year tenure, a rate that keeps sliding as the RBI eases policy through 2026.

The real frustration is rarely the rate alone. It is not knowing where else that money can go without losing the safety it was set aside for, and not trusting a relationship manager whose incentive is the product that pays the highest commission. Before you renew another FD, ask:

Are you renewing an FD because it is genuinely right for you, or because you have never compared it against a real alternative?

Has a bank or agent ever pushed you toward a product that paid them more than it helped you?

Do you know how much of your surplus should stay liquid, and how much can chase a better post tax return?

We built this guide to help you move past that hesitation. It compares the four most reliable alternative to fixed deposit options by return, risk, and liquidity, so you can match the right one to your goal, not to what pays your bank the most.

TL;DR

Government schemes like the PPF and RBI bonds carry a sovereign backing, making them the safest alternative to fixed deposit.

Debt mutual funds can beat FD returns while staying far more liquid than a locked in deposit.

Liquid funds settle in a day or two, which suits money you might need on short notice.

Corporate bonds pay a higher coupon than FD, but the extra yield comes with credit risk.

The right alternative to fixed deposit depends on your time horizon, not just the rate on offer.

Spreading money across two or three of these options often works better than picking just one.

Government Schemes and Bonds: The Safest Alternative to Fixed Deposit

For investors who want to stay safe, government backed schemes are the first alternative to fixed deposit worth considering, especially if you are working toward an early retirement beyond fixed deposits. The Public Provident Fund and National Savings Certificate carry a sovereign guarantee and Section 80C benefit, unlike a bank FD.

RBI Floating Rate Savings Bonds and government securities bought through the RBI Retail Direct portal add another layer of choice. Placed correctly within your asset allocation, their returns reset with market rates, so they hold up even as FD rates keep falling.

Public Provident Fund: 15 year lock in, tax free interest, Section 80C eligible.

RBI Floating Rate Bonds: 7 year tenure, rate resets twice a year.

Government securities: buy directly through RBI Retail Direct, no broker required.

These instruments trade flexibility for safety. If you want steadier growth with easier access to your money, the next option fits better.

FOR SAFETY FIRST ALLOCATIONS |

Not sure how much of your surplus belongs in government schemes versus market linked options? Our SEBI registered RIA team builds a fee-only allocation plan around your goals, not a product target. |

Schedule a Consultation: ckredencewealth.com/contact-us |

Debt Mutual Funds: A Flexible Alternative to Fixed Deposit

Debt mutual funds are a flexible alternative to fixed deposit for investors who still want low volatility returns. Unlike equity focused mutual funds, the fund pools your money into government securities, corporate debt, and money market instruments.

Unlike an FD, you are not locked into one rate for the full tenure. The fund manager can shift between shorter and longer duration paper as interest rates move.

Short duration and corporate bond funds suit a one to three year horizon.

Returns move with the rate cycle and are not fixed in advance.

Exit is usually available within a day or two, unlike an early FD withdrawal.

Debt funds work well when you want your money to stay reasonably close while still chasing a better post tax return.

DEBT FUND SELECTION |

Choosing between short duration, corporate bond, and money market debt funds gets easier with a plan matched to your time horizon and tax bracket. |

Explore Mutual Fund Advisory: ckredencewealth.com/mutual-funds |

Liquid Funds: The Fastest Alternative to Fixed Deposit for Short Term Money

When you need money on short notice, liquid funds are a practical alternative to fixed deposit. They invest in instruments maturing within 91 days, which keeps volatility low.

Most liquid funds settle in T+1, and many platforms allow instant redemption up to a set limit. That is often faster than the notice period a bank asks for on premature FD withdrawal.

Well suited to emergency funds and short term business surplus.

Credit risk stays low because holdings mature quickly.

Returns track short term rates, not a fixed FD coupon.

If your money needs to stay ready for use, a liquid fund protects that flexibility better than a locked in deposit.

LIQUIDITY PLANNING |

Emergency funds and short term business surplus need a structure, not a guess. We help you size the liquid bucket correctly against your full portfolio. |

Schedule a Consultation: ckredencewealth.com/contact-us |

Corporate Bonds: A Higher Yield Alternative to Fixed Deposit

For investors willing to accept some credit risk, corporate bonds are a higher yield alternative to fixed deposit. Companies issue these bonds to raise capital, and rating agencies grade them from AAA down to below investment grade.

Corporate bond yields have ranged from about 8 percent to 15 percent (GoldenPi), depending on the issuer’s rating. A higher rated bond pays closer to FD levels with a wider safety margin, while a lower rated bond pays more but carries real default risk, which is why sound bond portfolio strategy starts with credit quality, not coupon.

AAA rated bonds suit conservative investors who still want a bit more than FD.

Interest is usually paid on a fixed schedule, similar to an FD payout.

Bonds can be sold on the exchange before maturity, subject to market price.

Corporate bonds work best when you study the issuer’s credit quality first, not just the coupon on offer.

CREDIT RISK, VETTED |

A higher coupon means nothing if the issuer cannot pay it back. Our team screens credit quality before any bond enters a client portfolio. |

Explore Portfolio Management: ckredencewealth.com/pms |

Alternative to Fixed Deposit: Comparing Your Options

A side by side view makes the trade off clear.

Table: how each alternative to fixed deposit compares on tenure, liquidity, risk, and taxation.

Taxation is often the deciding factor once returns look similar. Understanding how mutual fund and PMS taxation works before you invest avoids an unpleasant surprise at redemption. Here is how the sourced yield ranges for three of these options compare against a current bank FD.

Indicative ranges only, not a return promise. Rates move with markets and issuer credit quality.

Debt mutual funds and liquid funds are not charted here because both are open ended, and their return depends on the prevailing rate cycle rather than a fixed coupon. Use the goal map below to place them correctly against your own need.

Match your goal to the right alternative to fixed deposit.

Why Should You Choose Ckredence Wealth?

Moving beyond an FD is easier with guidance that fits your goals, not a product pitch. Ckredence Wealth is a SEBI registered investment advisor (INA000020846) and portfolio manager (INP000007164), built on a 37 year legacy since 1987.

Solutions That Matter:

Fee only advice that matches each alternative to fixed deposit against your time horizon and risk appetite, through our RIA services.

Access to debt, bond, and equity strategies under one advisory relationship, across our investment approaches.

Ongoing review as interest rates and your goals change.

Ready to transform your investment approach? Schedule a Consultation!

Conclusion

An alternative to fixed deposit is not about giving up safety. It is about matching the right instrument to how soon you need the money and how much risk you can accept. Government schemes protect capital, debt funds add flexibility, liquid funds cover short notice needs, and corporate bonds raise the yield for investors who understand credit risk.

The investors who benefit most are the ones who stop renewing an FD out of habit and start reviewing it as one option among several. Keep emergency money liquid, use government schemes for long term safety, and add debt funds or bonds only once you understand what backs the return. A mix built around your goals will outperform a single instrument chosen out of comfort.

FAQs

01.

What is the best alternative to fixed deposit for safety?

Government schemes such as the PPF and RBI Floating Rate Bonds carry a sovereign guarantee, making them the safest alternative to fixed deposit available today.

02.

Can debt mutual funds lose value the way FDs never do?

Yes. Debt fund returns move with interest rates and are not fixed, unlike the rate locked in at FD opening.

03.

Which alternative to fixed deposit suits emergency funds best?

Liquid funds suit emergency money best, since they settle in T+1 and invest in instruments maturing within 91 days.

04.

Are corporate bonds safer than fixed deposits?

Not always. Corporate bonds pay a higher coupon but carry credit risk tied to the issuing company, so the credit rating matters more than the headline rate.