10min Read

10min Read

PMS Returns India 2026: What HNI Investors Must Know

PMS Returns India 2026: What HNI Investors Must Know

PMS Returns India 2026: What HNI Investors Must Know

40% of HNI investors in India are dissatisfied with returns despite a bull run. Read how to evaluate PMS beyond headline performance.

40% of HNI investors in India are dissatisfied with returns despite a bull run. Read how to evaluate PMS beyond headline performance.

40% of HNI investors in India are dissatisfied with returns despite a bull run. Read how to evaluate PMS beyond headline performance.

Ckredence Wealth

Ckredence Wealth

|

PMS returns India searches typically begin with a single number. That number alone rarely tells whether a PMS strategy matches an investor's goals, risk comfort, or holding period. SEBI data shows over 2,06,000 discretionary PMS clients in India as of January 2026, managing listed equity AUM of over ₹3.65 lakh crore, a scale that reflects growing demand for professionally managed portfolios among India's HNI segment.

That context changes what investors should be asking. The Marcellus India Wealth Survey 2025 found that 40% of HNI investors in India expressed dissatisfaction with their investment returns despite a five-year equity bull run. PMS returns must be read alongside risk, drawdown, fees, and tax outcomes to reflect what an investor actually takes home.

TL;DR

PMS returns must be evaluated with risk, drawdown, fees, and tax together.

One-year PMS performance can mislead investors in strong equity market phases.

Strategy type matters because large-cap, multi-cap, and small-cap PMS behave differently.

Post-tax PMS returns differ from reported returns due to direct security ownership.

PMS suits investors who understand volatility and prefer customised portfolio management.

Wealth managers review consistency, portfolio quality, and investor fit before return claims.

What Are PMS Returns and How Are They Calculated?

PMS returns show how a professionally managed portfolio has performed over a chosen period. In India, PMS performance is usually discussed through CAGR, absolute returns, benchmark comparison, and risk-adjusted performance.

The key point is simple. PMS returns are not a fixed promise. They are the result of stock selection, allocation, market cycles, portfolio concentration, and the fund manager's decisions.

PMS meaning explained simply

Portfolio Management Services are investment services where a professional portfolio manager manages a portfolio for an investor. Our portfolio management services overview explains how discretionary PMS differs from pooled investment schemes and why direct ownership changes the tax structure for investors.

CAGR vs absolute returns

CAGR shows the annualised growth rate over a period. It is useful when comparing PMS performance across longer holding periods.

Absolute return shows total gain or loss for a specific period. It can look strong in a bullish year but does not show strategy consistency.

Why PMS returns differ from mutual fund returns

PMS portfolios often hold fewer stocks than mutual funds. This can increase return potential, but it also increases volatility.

Mutual funds are more standardised and diversified. PMS can be more focused, so performance dispersion can be wider.

What Returns Have PMS Strategies Historically Delivered in India?

PMS returns in India have varied across managers, market-cap exposure, and investment style. Some strategies do well in growth phases, while others hold better during weak markets.

This is why historical PMS returns should be studied across market cycles. A single strong year does not prove manager quality.

PMS across market cycles

A PMS strategy that performs well in a broad market rally may struggle when liquidity dries up. Small and mid-cap exposure can make this movement sharper.

A stronger review studies how the portfolio behaved in corrections. Investors should ask whether returns came from stock quality or only market momentum.

PMS vs Nifty 50 performance

The Nifty 50 is often used as a market benchmark. But every PMS should be compared with a benchmark that fits its portfolio style.

A small-cap PMS should not be judged only against a large-cap index. The benchmark must match the portfolio's investment universe.

Why historical returns should be viewed carefully

Historical returns are useful, but they are not a forecast. They show what happened under past market conditions.

Investors should check whether the same process can work in current valuations, interest-rate conditions, and sector cycles. That is where a wealth manager's review becomes useful.

🎯 Most PMS return comparisons miss a critical variable: whether the strategy still makes sense at current valuations. Our advisory team at Ckredence Wealth reviews strategy fit, market cycle positioning, and investor suitability in one structured session. Speak with our advisory team today to evaluate which PMS strategy aligns with your long-term plan.

Why Do PMS Returns Vary So Much Across Different Strategies?

PMS returns vary because each strategy can follow a different investment style. Some focus on concentrated growth stocks, while others prefer diversified portfolios or cycle-based allocation.

The return gap comes from how the portfolio is built. Two PMS products can both invest in equities, yet their risk and return behavior can be very different.

Key return drivers investors should check

The main drivers usually include:

Portfolio concentration: Fewer stocks can increase both upside and downside.

Market-cap exposure: Small and mid-cap strategies usually move more sharply.

Investment style: Growth, value, quality, and thematic styles perform in different phases.

Manager discipline: Buy, hold, exit, and cash decisions affect outcomes.

Risk controls: Drawdown management matters during market corrections.

This is why PMS comparison should never stop at the return column. The portfolio design explains the return pattern.

Risk and return trade-off

Higher return potential often comes with higher variation. Investors must be comfortable with that variation before choosing PMS.

A PMS that fits one investor may be unsuitable for another. Age, liquidity need, income stability, and investment horizon all matter.

Which PMS Categories Have Generated the Highest Returns in India?

PMS categories that take higher equity risk can show higher returns in favorable market phases. Small-cap, mid-cap, thematic, and focused growth strategies often look attractive in strong cycles.

But the highest-returning category is not automatically the best category. The right PMS category depends on risk capacity and time horizon.

Why category selection matters

A category can look poor in one phase and strong later. That is normal in equity investing.

Investors should not switch categories only because one recent return chart looks better. Frequent switching can reduce compounding and create unnecessary tax events.

Why Many Investors Focus Only on PMS Returns and Ignore Risk?

Many investors look at the highest PMS returns first. This is natural, but it can lead to poor selection.

Return numbers are easy to compare. Risk quality needs more reading.

"The investor's chief problem, and even his worst enemy, is likely to be himself." Benjamin Graham, Economist and Value Investor

Source: The Intelligent Investor, HarperCollins

Common return-chasing mistakes

Investors often make these mistakes:

They select PMS based on recent top performance.

They ignore how concentrated the portfolio is.

They do not ask how much the portfolio fell in weak markets.

They compare gross returns without checking fees and taxes.

They exit too early when volatility feels uncomfortable.

These mistakes usually come from incomplete comparison. A PMS review should study both return and behavior.

📊 40% of HNI investors in India expressed dissatisfaction with their investment returns despite a five-year equity bull run: This gap between market performance and investor experience shows how rarely headline returns reflect actual portfolio outcomes.

Source: Marcellus India Wealth Survey 2025

Why drawdown matters

Drawdown shows how much a portfolio falls from its peak. It matters because investors rarely experience returns in a straight line.

A portfolio that falls sharply can push the investor into panic selling. This is why risk-adjusted returns matter more than headline returns.

How Do PMS Returns Compare With Mutual Funds?

PMS and mutual funds both invest in securities, but they serve different investor needs. PMS offers direct ownership and more room for customisation, while mutual funds offer pooled diversification and easier access.

The comparison should begin with suitability. Our PMS vs mutual funds guide covers which structure fits different investor profiles, goals, and tax positions before any allocation decision is made.

PMS vs mutual funds comparison

Factor | PMS | Mutual Funds |

Ownership | Direct securities in investor account | Units of pooled scheme |

Access | For larger portfolios | Open to smaller investors |

Customisation | Higher | Limited |

Transparency | Portfolio-level visibility | Scheme-level reporting |

Costs | Fee model varies by agreement | Expense ratio based |

Tax treatment | Security-level gains in investor account | Fund-level structure differs |

Which investors prefer PMS?

PMS usually suits HNIs who want professional management with greater visibility. It also suits investors who understand market risk and can hold through cycles.

Mutual funds may suit investors who want simpler access and broader diversification. Many HNI portfolios use both structures together.

📋 Choosing between PMS and mutual funds without a suitability assessment often results in a portfolio that fits neither goal nor risk profile. Request a portfolio review with Ckredence Wealth to understand which investment structure fits your financial goals and tax position.

How Much Do Fees and Taxes Impact PMS Returns?

Fees and taxes can change the actual return an investor receives. That is why PMS returns should be evaluated on a post-fee and post-tax basis.

Reported returns may not match the investor's final experience. The difference depends on fee structure, churn, holding period, and tax rules.

Common PMS fee structures

PMS fee structures generally fall into these types:

Fixed management fee

Performance-linked fee

Hybrid fee with fixed and performance components

Exit load or other charges as per agreement

A lower fee is not always better. Our PMS charges breakdown explains how each fee model affects portfolio accountability and long-term net returns for HNI investors.

Tax impact in PMS

In PMS, the investor owns securities directly. Gains from the sale of listed equity are taxed based on holding period and applicable capital gains rules.

High portfolio churn can create more short-term gains. That can reduce the final return retained by the investor.

What Do Experienced Investors Look for Beyond PMS Returns?

Experienced investors do not stop at return charts. They ask how those returns were produced.

This changes the review from "what performed best?" to "what can remain suitable across different market phases?"

"Know what you own, and know why you own it." Peter Lynch, Former Portfolio Manager, Fidelity Investments

Source: One Up on Wall Street, Simon & Schuster

Practical PMS evaluation checklist

A serious PMS review should include:

Consistency: Did the strategy perform only in one cycle?

Benchmark fit: Is the benchmark suitable for the portfolio style?

Portfolio construction: Are positions sized with discipline?

Risk control: How does the manager handle corrections?

Churn: Is the portfolio traded too often?

Communication: Are reports clear and timely?

Investor fit: Does the strategy suit the investor's goals?

This checklist gives a better view than return ranking alone. It also reduces the chance of picking a PMS based only on recent noise.

What Are the Most Common Mistakes Investors Make When Evaluating PMS Returns?

The most common mistake is treating PMS like a leaderboard. The highest recent return often attracts attention, but it may not suit the investor.

PMS is a long-term portfolio decision. Investors who study our minimum investment for PMS guide understand that the entry threshold reflects a commitment to a longer-term allocation horizon, not a short-cycle product.

Mistake-to-correction view

Mistake | Better Way to Evaluate |

Choosing recent winners | Study rolling performance across cycles |

Ignoring drawdown | Ask how the portfolio behaved in corrections |

Overlooking fees | Compare post-fee return expectations |

Ignoring tax | Review churn and exit timing |

Comparing wrongly | Match PMS with the right benchmark |

Skipping suitability | Fit PMS to goal, horizon, and risk profile |

Why investor behavior matters

Even a good PMS can fail for an investor who exits at the wrong time. Behaviour affects final returns.

This is why review meetings matter. Investors need context when short-term performance looks weak.

How Professional Wealth Managers Evaluate PMS Opportunities?

Professional wealth managers evaluate PMS opportunities with a risk-first method. Returns matter, but they are not the starting point.

The starting point is investor suitability. A PMS should fit the investor's financial goals, liquidity needs, tax position, and risk appetite.

Evaluation method used by wealth managers

The key steps involved are:

Define the investor profile: Goal, age, liquidity need, and risk comfort.

Map the current portfolio: Existing equity, debt, mutual fund, and PMS exposure.

Study strategy fit: Match PMS style to portfolio gap.

Check risk behaviour: Review drawdowns, concentration, and churn.

Review fee and tax impact: Estimate real investor-level outcome.

Monitor periodically: Review changes in portfolio, manager, and market conditions.

This method reduces emotional selection. It also helps investors avoid overlap across multiple products.

Why Ckredence Wealth Focuses on Risk-Adjusted PMS Selection?

We approach PMS selection through investor goals, risk comfort, and long-term portfolio fit. The aim is not to chase the highest recent return.

Ckredence Wealth Management Pvt. Ltd. was established in 1987, is SEBI registered, and offers PMS, mutual funds, and equity investment services. The firm has branches in Surat, Mumbai, and Vadodara, offering PMS strategies that range from our All Weather investment approach to Diversified, Business Cycle, and ICE Growth.

We focus on:

Goal-based selection: We match each PMS strategy to the investor's specific financial goals, not to recent return charts.

Investment style diversification: Our advisory covers multiple strategies across market cycles, helping investors avoid undue concentration in any single style.

Concentration risk review: We evaluate how concentrated a PMS portfolio is and what that concentration means for downside exposure in weak market phases.

Long-term portfolio construction: We build PMS allocations around a holding period and goal horizon, not on short-term performance signals.

Fee transparency: We explain every fee component before the investor commits capital, including management fees, performance-linked structures, and exit clauses.

Regular performance discussion: We conduct periodic reviews to help investors stay anchored to their original investment rationale.

This matters because HNI investors in India often need structured, relationship-led support before making large allocation decisions.

🤝 If recent PMS return charts are your only reference point, the evaluation is missing its most important steps. Connect with our SEBI-registered advisory team at Ckredence Wealth to build a PMS evaluation framework around your goals, risk profile, and tax position.

01.

What does SEBI registration mean for a PMS investor?

A SEBI-registered portfolio manager follows SEBI's regulations on reporting, disclosure, and investor protection. Investors can verify registration status on SEBI's official intermediary portal before committing capital.

02.

How is PMS different from a mutual fund for HNI investors?

In PMS, the investor holds securities directly in their own demat account, unlike a mutual fund where they own units of a pooled scheme. This direct ownership structure affects tax treatment, portfolio visibility, and the level of customisation available. PMS also requires a higher minimum investment than mutual fund products.

03.

Who is PMS most suitable for in India?

PMS is most suitable for HNI investors with a minimum investable surplus of ₹50 lakh, as mandated by SEBI. Investors who can hold through volatility and need no immediate liquidity benefit most from a professionally managed portfolio.

04.

How does the PMS engagement and review process work at Ckredence Wealth?

We begin with an investor suitability assessment covering goals, risk appetite, and existing portfolio composition. After strategy selection, investors receive regular portfolio reports and periodic review discussions to keep the strategy aligned with their financial plan.

PMS returns India searches typically begin with a single number. That number alone rarely tells whether a PMS strategy matches an investor's goals, risk comfort, or holding period. SEBI data shows over 2,06,000 discretionary PMS clients in India as of January 2026, managing listed equity AUM of over ₹3.65 lakh crore, a scale that reflects growing demand for professionally managed portfolios among India's HNI segment.

That context changes what investors should be asking. The Marcellus India Wealth Survey 2025 found that 40% of HNI investors in India expressed dissatisfaction with their investment returns despite a five-year equity bull run. PMS returns must be read alongside risk, drawdown, fees, and tax outcomes to reflect what an investor actually takes home.

TL;DR

PMS returns must be evaluated with risk, drawdown, fees, and tax together.

One-year PMS performance can mislead investors in strong equity market phases.

Strategy type matters because large-cap, multi-cap, and small-cap PMS behave differently.

Post-tax PMS returns differ from reported returns due to direct security ownership.

PMS suits investors who understand volatility and prefer customised portfolio management.

Wealth managers review consistency, portfolio quality, and investor fit before return claims.

What Are PMS Returns and How Are They Calculated?

PMS returns show how a professionally managed portfolio has performed over a chosen period. In India, PMS performance is usually discussed through CAGR, absolute returns, benchmark comparison, and risk-adjusted performance.

The key point is simple. PMS returns are not a fixed promise. They are the result of stock selection, allocation, market cycles, portfolio concentration, and the fund manager's decisions.

PMS meaning explained simply

Portfolio Management Services are investment services where a professional portfolio manager manages a portfolio for an investor. Our portfolio management services overview explains how discretionary PMS differs from pooled investment schemes and why direct ownership changes the tax structure for investors.

CAGR vs absolute returns

CAGR shows the annualised growth rate over a period. It is useful when comparing PMS performance across longer holding periods.

Absolute return shows total gain or loss for a specific period. It can look strong in a bullish year but does not show strategy consistency.

Why PMS returns differ from mutual fund returns

PMS portfolios often hold fewer stocks than mutual funds. This can increase return potential, but it also increases volatility.

Mutual funds are more standardised and diversified. PMS can be more focused, so performance dispersion can be wider.

What Returns Have PMS Strategies Historically Delivered in India?

PMS returns in India have varied across managers, market-cap exposure, and investment style. Some strategies do well in growth phases, while others hold better during weak markets.

This is why historical PMS returns should be studied across market cycles. A single strong year does not prove manager quality.

PMS across market cycles

A PMS strategy that performs well in a broad market rally may struggle when liquidity dries up. Small and mid-cap exposure can make this movement sharper.

A stronger review studies how the portfolio behaved in corrections. Investors should ask whether returns came from stock quality or only market momentum.

PMS vs Nifty 50 performance

The Nifty 50 is often used as a market benchmark. But every PMS should be compared with a benchmark that fits its portfolio style.

A small-cap PMS should not be judged only against a large-cap index. The benchmark must match the portfolio's investment universe.

Why historical returns should be viewed carefully

Historical returns are useful, but they are not a forecast. They show what happened under past market conditions.

Investors should check whether the same process can work in current valuations, interest-rate conditions, and sector cycles. That is where a wealth manager's review becomes useful.

🎯 Most PMS return comparisons miss a critical variable: whether the strategy still makes sense at current valuations. Our advisory team at Ckredence Wealth reviews strategy fit, market cycle positioning, and investor suitability in one structured session. Speak with our advisory team today to evaluate which PMS strategy aligns with your long-term plan.

Why Do PMS Returns Vary So Much Across Different Strategies?

PMS returns vary because each strategy can follow a different investment style. Some focus on concentrated growth stocks, while others prefer diversified portfolios or cycle-based allocation.

The return gap comes from how the portfolio is built. Two PMS products can both invest in equities, yet their risk and return behavior can be very different.

Key return drivers investors should check

The main drivers usually include:

Portfolio concentration: Fewer stocks can increase both upside and downside.

Market-cap exposure: Small and mid-cap strategies usually move more sharply.

Investment style: Growth, value, quality, and thematic styles perform in different phases.

Manager discipline: Buy, hold, exit, and cash decisions affect outcomes.

Risk controls: Drawdown management matters during market corrections.

This is why PMS comparison should never stop at the return column. The portfolio design explains the return pattern.

Risk and return trade-off

Higher return potential often comes with higher variation. Investors must be comfortable with that variation before choosing PMS.

A PMS that fits one investor may be unsuitable for another. Age, liquidity need, income stability, and investment horizon all matter.

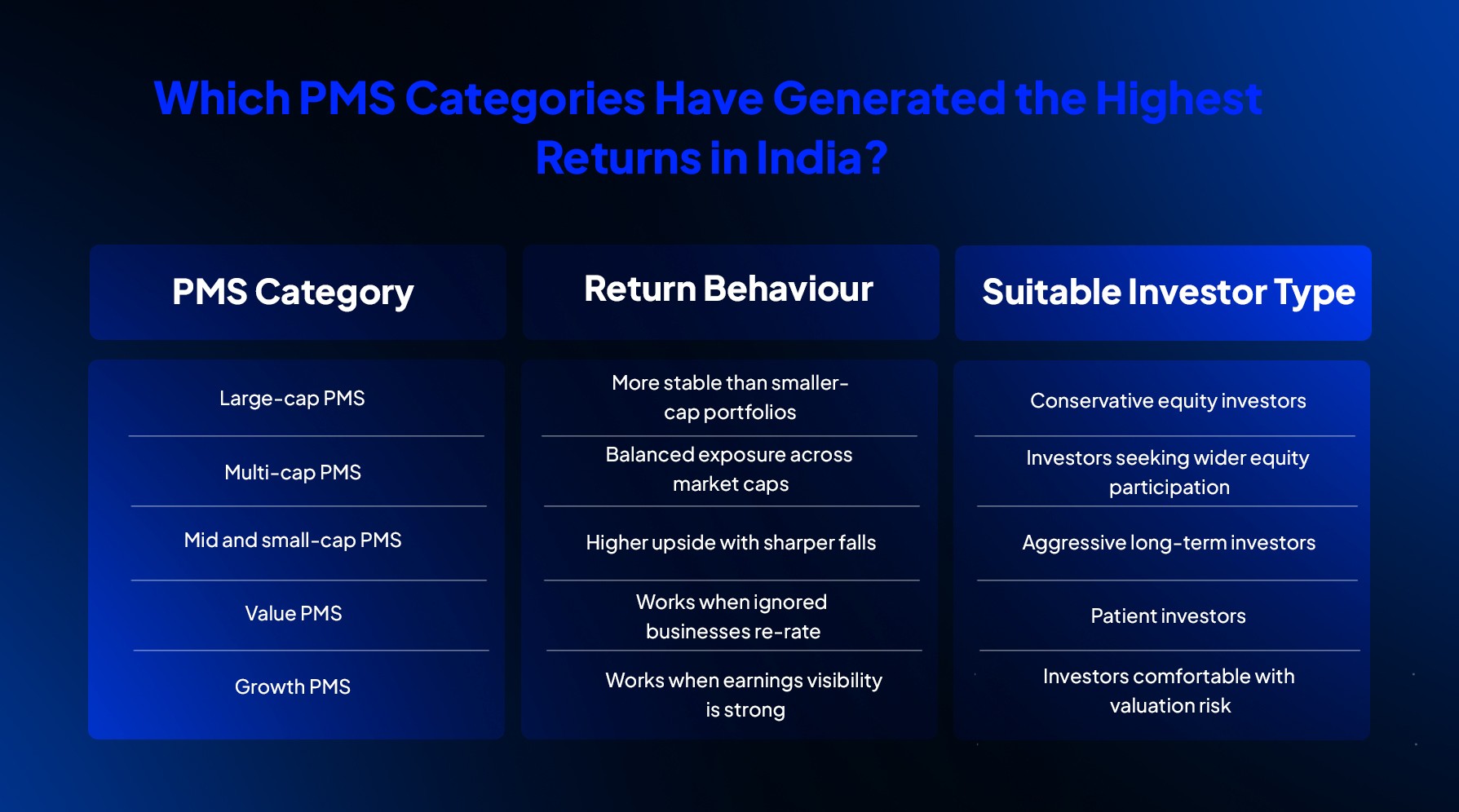

Which PMS Categories Have Generated the Highest Returns in India?

PMS categories that take higher equity risk can show higher returns in favorable market phases. Small-cap, mid-cap, thematic, and focused growth strategies often look attractive in strong cycles.

But the highest-returning category is not automatically the best category. The right PMS category depends on risk capacity and time horizon.

Why category selection matters

A category can look poor in one phase and strong later. That is normal in equity investing.

Investors should not switch categories only because one recent return chart looks better. Frequent switching can reduce compounding and create unnecessary tax events.

Why Many Investors Focus Only on PMS Returns and Ignore Risk?

Many investors look at the highest PMS returns first. This is natural, but it can lead to poor selection.

Return numbers are easy to compare. Risk quality needs more reading.

"The investor's chief problem, and even his worst enemy, is likely to be himself." Benjamin Graham, Economist and Value Investor

Source: The Intelligent Investor, HarperCollins

Common return-chasing mistakes

Investors often make these mistakes:

They select PMS based on recent top performance.

They ignore how concentrated the portfolio is.

They do not ask how much the portfolio fell in weak markets.

They compare gross returns without checking fees and taxes.

They exit too early when volatility feels uncomfortable.

These mistakes usually come from incomplete comparison. A PMS review should study both return and behavior.

📊 40% of HNI investors in India expressed dissatisfaction with their investment returns despite a five-year equity bull run: This gap between market performance and investor experience shows how rarely headline returns reflect actual portfolio outcomes.

Source: Marcellus India Wealth Survey 2025

Why drawdown matters

Drawdown shows how much a portfolio falls from its peak. It matters because investors rarely experience returns in a straight line.

A portfolio that falls sharply can push the investor into panic selling. This is why risk-adjusted returns matter more than headline returns.

How Do PMS Returns Compare With Mutual Funds?

PMS and mutual funds both invest in securities, but they serve different investor needs. PMS offers direct ownership and more room for customisation, while mutual funds offer pooled diversification and easier access.

The comparison should begin with suitability. Our PMS vs mutual funds guide covers which structure fits different investor profiles, goals, and tax positions before any allocation decision is made.

PMS vs mutual funds comparison

Factor | PMS | Mutual Funds |

Ownership | Direct securities in investor account | Units of pooled scheme |

Access | For larger portfolios | Open to smaller investors |

Customisation | Higher | Limited |

Transparency | Portfolio-level visibility | Scheme-level reporting |

Costs | Fee model varies by agreement | Expense ratio based |

Tax treatment | Security-level gains in investor account | Fund-level structure differs |

Which investors prefer PMS?

PMS usually suits HNIs who want professional management with greater visibility. It also suits investors who understand market risk and can hold through cycles.

Mutual funds may suit investors who want simpler access and broader diversification. Many HNI portfolios use both structures together.

📋 Choosing between PMS and mutual funds without a suitability assessment often results in a portfolio that fits neither goal nor risk profile. Request a portfolio review with Ckredence Wealth to understand which investment structure fits your financial goals and tax position.

How Much Do Fees and Taxes Impact PMS Returns?

Fees and taxes can change the actual return an investor receives. That is why PMS returns should be evaluated on a post-fee and post-tax basis.

Reported returns may not match the investor's final experience. The difference depends on fee structure, churn, holding period, and tax rules.

Common PMS fee structures

PMS fee structures generally fall into these types:

Fixed management fee

Performance-linked fee

Hybrid fee with fixed and performance components

Exit load or other charges as per agreement

A lower fee is not always better. Our PMS charges breakdown explains how each fee model affects portfolio accountability and long-term net returns for HNI investors.

Tax impact in PMS

In PMS, the investor owns securities directly. Gains from the sale of listed equity are taxed based on holding period and applicable capital gains rules.

High portfolio churn can create more short-term gains. That can reduce the final return retained by the investor.

What Do Experienced Investors Look for Beyond PMS Returns?

Experienced investors do not stop at return charts. They ask how those returns were produced.

This changes the review from "what performed best?" to "what can remain suitable across different market phases?"

"Know what you own, and know why you own it." Peter Lynch, Former Portfolio Manager, Fidelity Investments

Source: One Up on Wall Street, Simon & Schuster

Practical PMS evaluation checklist

A serious PMS review should include:

Consistency: Did the strategy perform only in one cycle?

Benchmark fit: Is the benchmark suitable for the portfolio style?

Portfolio construction: Are positions sized with discipline?

Risk control: How does the manager handle corrections?

Churn: Is the portfolio traded too often?

Communication: Are reports clear and timely?

Investor fit: Does the strategy suit the investor's goals?

This checklist gives a better view than return ranking alone. It also reduces the chance of picking a PMS based only on recent noise.

What Are the Most Common Mistakes Investors Make When Evaluating PMS Returns?

The most common mistake is treating PMS like a leaderboard. The highest recent return often attracts attention, but it may not suit the investor.

PMS is a long-term portfolio decision. Investors who study our minimum investment for PMS guide understand that the entry threshold reflects a commitment to a longer-term allocation horizon, not a short-cycle product.

Mistake-to-correction view

Mistake | Better Way to Evaluate |

Choosing recent winners | Study rolling performance across cycles |

Ignoring drawdown | Ask how the portfolio behaved in corrections |

Overlooking fees | Compare post-fee return expectations |

Ignoring tax | Review churn and exit timing |

Comparing wrongly | Match PMS with the right benchmark |

Skipping suitability | Fit PMS to goal, horizon, and risk profile |

Why investor behavior matters

Even a good PMS can fail for an investor who exits at the wrong time. Behaviour affects final returns.

This is why review meetings matter. Investors need context when short-term performance looks weak.

How Professional Wealth Managers Evaluate PMS Opportunities?

Professional wealth managers evaluate PMS opportunities with a risk-first method. Returns matter, but they are not the starting point.

The starting point is investor suitability. A PMS should fit the investor's financial goals, liquidity needs, tax position, and risk appetite.

Evaluation method used by wealth managers

The key steps involved are:

Define the investor profile: Goal, age, liquidity need, and risk comfort.

Map the current portfolio: Existing equity, debt, mutual fund, and PMS exposure.

Study strategy fit: Match PMS style to portfolio gap.

Check risk behaviour: Review drawdowns, concentration, and churn.

Review fee and tax impact: Estimate real investor-level outcome.

Monitor periodically: Review changes in portfolio, manager, and market conditions.

This method reduces emotional selection. It also helps investors avoid overlap across multiple products.

Why Ckredence Wealth Focuses on Risk-Adjusted PMS Selection?

We approach PMS selection through investor goals, risk comfort, and long-term portfolio fit. The aim is not to chase the highest recent return.

Ckredence Wealth Management Pvt. Ltd. was established in 1987, is SEBI registered, and offers PMS, mutual funds, and equity investment services. The firm has branches in Surat, Mumbai, and Vadodara, offering PMS strategies that range from our All Weather investment approach to Diversified, Business Cycle, and ICE Growth.

We focus on:

Goal-based selection: We match each PMS strategy to the investor's specific financial goals, not to recent return charts.

Investment style diversification: Our advisory covers multiple strategies across market cycles, helping investors avoid undue concentration in any single style.

Concentration risk review: We evaluate how concentrated a PMS portfolio is and what that concentration means for downside exposure in weak market phases.

Long-term portfolio construction: We build PMS allocations around a holding period and goal horizon, not on short-term performance signals.

Fee transparency: We explain every fee component before the investor commits capital, including management fees, performance-linked structures, and exit clauses.

Regular performance discussion: We conduct periodic reviews to help investors stay anchored to their original investment rationale.

This matters because HNI investors in India often need structured, relationship-led support before making large allocation decisions.

🤝 If recent PMS return charts are your only reference point, the evaluation is missing its most important steps. Connect with our SEBI-registered advisory team at Ckredence Wealth to build a PMS evaluation framework around your goals, risk profile, and tax position.

01.

What does SEBI registration mean for a PMS investor?

A SEBI-registered portfolio manager follows SEBI's regulations on reporting, disclosure, and investor protection. Investors can verify registration status on SEBI's official intermediary portal before committing capital.

02.

How is PMS different from a mutual fund for HNI investors?

In PMS, the investor holds securities directly in their own demat account, unlike a mutual fund where they own units of a pooled scheme. This direct ownership structure affects tax treatment, portfolio visibility, and the level of customisation available. PMS also requires a higher minimum investment than mutual fund products.

03.

Who is PMS most suitable for in India?

PMS is most suitable for HNI investors with a minimum investable surplus of ₹50 lakh, as mandated by SEBI. Investors who can hold through volatility and need no immediate liquidity benefit most from a professionally managed portfolio.

04.

How does the PMS engagement and review process work at Ckredence Wealth?

We begin with an investor suitability assessment covering goals, risk appetite, and existing portfolio composition. After strategy selection, investors receive regular portfolio reports and periodic review discussions to keep the strategy aligned with their financial plan.