10min Read

10min Read

Financial Advisory Services in India: What You Get With a SEBI RIA vs a Broker

Financial Advisory Services in India: What You Get With a SEBI RIA vs a Broker

Financial Advisory Services in India: What You Get With a SEBI RIA vs a Broker

Meta Desc Understand how a SEBI registered investment advisor differs from a broker in India, from fiduciary duty and fees to which one fits your goals.

Meta Desc Understand how a SEBI registered investment advisor differs from a broker in India, from fiduciary duty and fees to which one fits your goals.

Meta Desc Understand how a SEBI registered investment advisor differs from a broker in India, from fiduciary duty and fees to which one fits your goals.

Ckredence Wealth

Ckredence Wealth

|

Choosing who guides your money is a serious decision. In India, most people open a broker account long before they ever speak to a fiduciary adviser.

As of August 2025, the country had only around 967 SEBI registered investment advisers serving more than 20 crore investors, against over 17 crore demat accounts. That is roughly one regulated adviser for every two million investors.

The numbers explain why the SEBI RIA vs broker question matters. Before you act on anyone’s guidance, ask:

Are you paying for advice, or paying commission on products someone else profits from?

Does the person guiding your portfolio have a legal duty to put you first?

When markets fall, who is accountable for the advice you followed?

We wrote this guide to make the choice clear. It compares a SEBI RIA vs broker across role, regulation, fees, and fit. By the end, you will know which one your goals need.

TL;DR

A SEBI RIA is a fiduciary bound by law to act in your interest, while a broker is an execution intermediary.

The heart of the SEBI RIA vs broker gap is payment: advisory fees versus brokerage and product commissions.

RIAs charge a flat fee or a share of assets, so their income does not depend on how often you trade.

A broker cannot charge brokerage on advice given in an RIA capacity, which keeps advice and execution apart.

Choose an RIA for planning and unbiased guidance, and a broker for low cost trade execution.

The same group can offer both, as long as the advisory and broking arms stay separate.

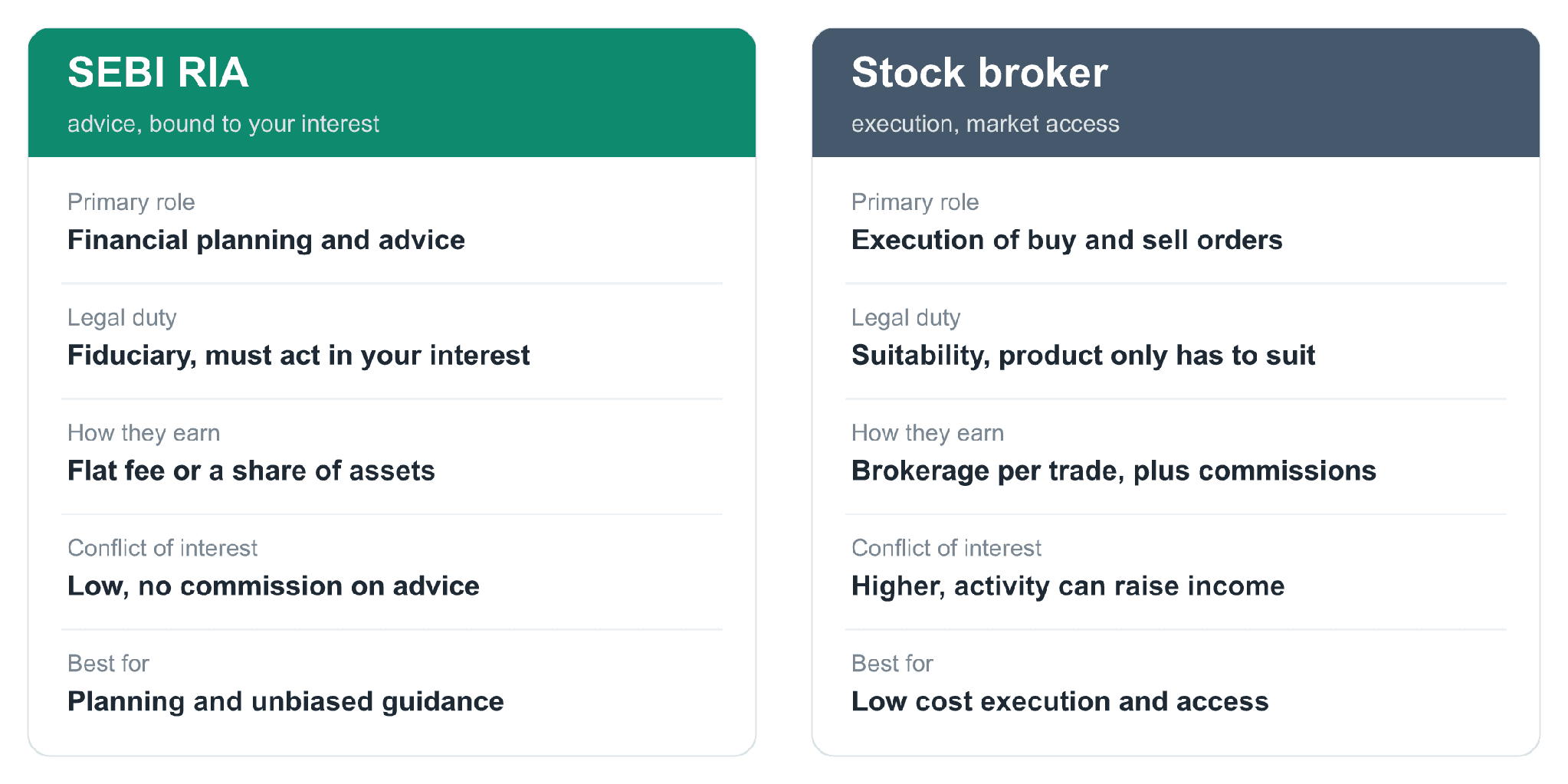

What Is a SEBI Registered Investment Advisor (RIA)?

A SEBI registered investment advisor is a professional licensed to give personalised financial advice for a fee. Registration is not a formality. Every RIA must clear the NISM investment adviser exams and hold a SEBI number before advising a single client.

In the SEBI RIA vs broker comparison, three features define an RIA:

Fiduciary duty: a legal obligation to place your interest ahead of their own.

Fee-only income: paid by you, not by the companies whose products they recommend.

No commission conflict: they cannot earn brokerage on the advice they give.

This structure is why an RIA sits on your side of the table. You can read the detail in our guide to the SEBI RIA in India.

What Is a Stock Broker in India?

A stock broker is a SEBI registered intermediary that executes your buy and sell orders. The broker gives you exchange access, a trading platform, and a demat account. Their core job is execution, not planning.

Brokers earn through brokerage on each trade, and sometimes through commissions on products they distribute. In the SEBI RIA vs broker setup, a broker follows a suitability standard. A product only has to be suitable for you, not the best option available. That difference in duty changes everything.

SEBI RIA vs Broker: Core Differences at a Glance

The clearest way to see the SEBI RIA vs broker difference is side by side. The visual below maps how each one earns, what each owes you by law, and what each is built to do.

SEBI RIA vs Broker: core differences at a glance.

The Important Regulatory Difference: Advice, Distribution and Implementation

Myth: An RIA Cannot Help You Implement Advice

Reality: An RIA may offer implementation services through direct schemes or products, provided there is no commission or referral income and the client is not required to use that service.

Myth: A Broker Cannot Give Any Advice

Reality: A SEBI-registered broker may offer basic advice that is incidental to its broking activity for existing broking clients.

Myth: Every Financial Professional Can Be Paid Both Ways

Reality: Individual IAs cannot provide distribution services. Non-individual IAs must maintain clear segregation between advisory and distribution clients.

Myth: RIA Registration Guarantees Returns

Reality: RIA registration does not assure investment outcomes. It means the adviser is subject to SEBI rules on fiduciary conduct, risk profiling, disclosures, and suitability.

Fee-Only vs Commission: What Each Model Costs You

Fees decide how much of your return you keep. In the SEBI RIA vs broker choice, a fee-only adviser charges a transparent, agreed amount. A broker earns from activity, so cost rises with every trade and every commission bearing product.

On a large portfolio, that gap adds up. The chart shows an illustrative yearly cost on a Rs.50 lakh portfolio, comparing a fee-only advisory model with a commission led broking model.

Illustrative annual cost on a Rs.50 lakh portfolio. Example only, not a quote.

Lower visible cost is not always lower real cost. Hidden commissions can quietly outweigh a clear advisory fee.

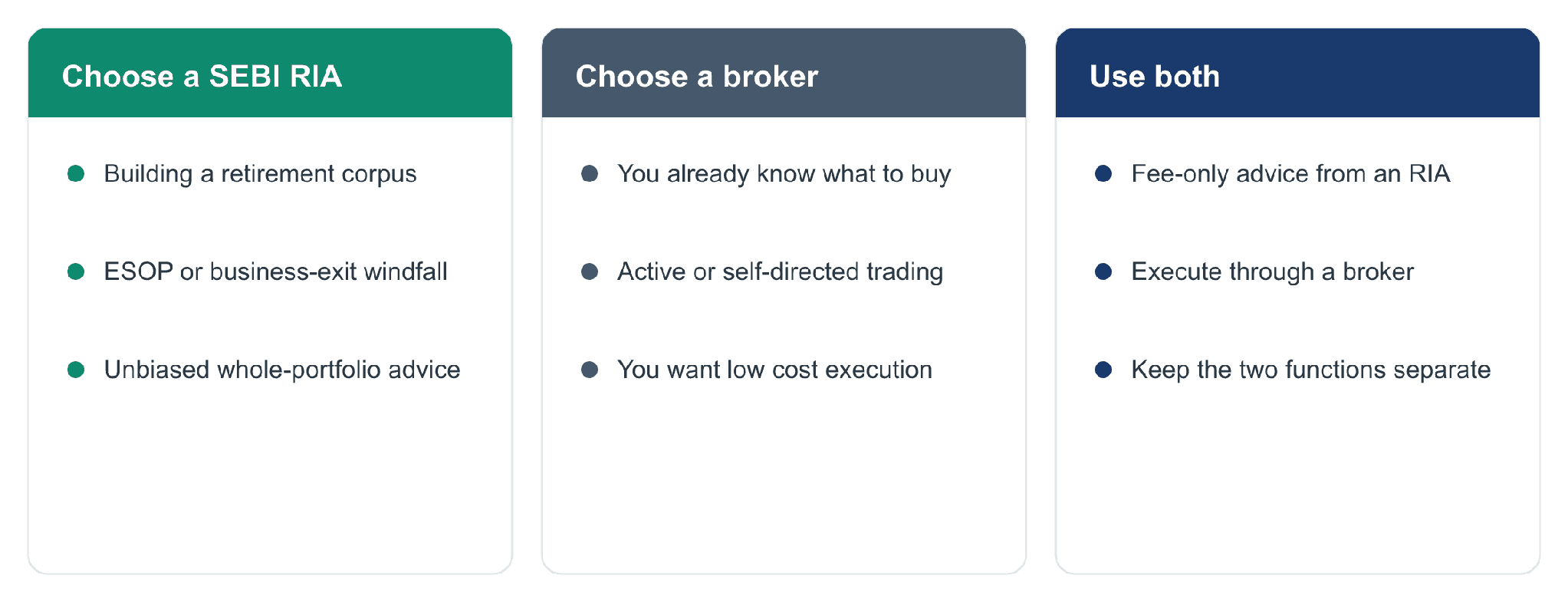

When Should You Choose a SEBI RIA vs a Broker?

The right answer depends on what you need. The SEBI RIA vs broker decision comes down to whether you want guidance or only access to the market.

When to choose a SEBI RIA, a broker, or both.

When to Choose a SEBI RIA

Choose an RIA when you want a plan, not just a trade. If you are building a retirement corpus, managing an ESOP windfall, or want unbiased advice across your whole portfolio, a fiduciary adviser fits. Our investment approaches are built around this kind of goal based planning.

When to Choose a Stock Broker

Choose a broker when you already know what you want to buy. Active traders and self-directed investors who value low cost execution are well served by a broker alone.

Can a SEBI RIA and Broker Overlap?

Yes, and many investors use both. You can take fee-only advice from an RIA and execute through a broker. The rule is that the two functions stay separate, so your advice stays unbiased.

Why Should You Choose Ckredence Wealth?

When the SEBI RIA vs broker choice comes down to trust, credentials matter. We are a SEBI registered investment advisor (INA000020846) and a SEBI registered portfolio manager (INP000007164), built on a 37 year legacy since 1987.

Solutions That Matter:

Fee-only, fiduciary advice with no commission conflict on the guidance we give.

A dedicated RIA principal officer and research led portfolio management.

Goal based planning across retirement, direct equity, and wealth structuring.

Whether you are moving beyond a broker relationship or building your first advised portfolio, we act on your side of the table. Ready to transform your investment approach? Schedule a Consultation!

Conclusion

The SEBI RIA vs broker choice comes down to whose interest comes first. A broker gives you access and execution, and earns from how much you trade. A SEBI RIA gives you advice that the law binds to your benefit. One helps you act, the other helps you decide.

Before you sign with either, read how they are paid, because payment shapes behaviour. Most serious investors eventually use both, each for what it does best. As your portfolio grows past mutual funds, advised management becomes the practical next step. Match the role to the job, and your outcome stays protected.

FAQs

01.

What is the main difference between a SEBI RIA and a broker?

A SEBI RIA gives fee-only, fiduciary advice. A broker executes trades and earns brokerage. One advises, the other executes.

02.

Can the same firm be both an RIA and a broker?

Yes, but the advisory and broking arms must stay separate. A broker cannot charge brokerage on advice given as an RIA.

03.

Do SEBI registered investment advisors charge commission?

No. RIAs are paid directly by clients through fees. They cannot earn commission on the advice they provide.

04.

Is a SEBI RIA worth it for a smaller portfolio?

It depends on your need for planning. Fee-only advice suits investors who want unbiased, goal based guidance over product selling.

Choosing who guides your money is a serious decision. In India, most people open a broker account long before they ever speak to a fiduciary adviser.

As of August 2025, the country had only around 967 SEBI registered investment advisers serving more than 20 crore investors, against over 17 crore demat accounts. That is roughly one regulated adviser for every two million investors.

The numbers explain why the SEBI RIA vs broker question matters. Before you act on anyone’s guidance, ask:

Are you paying for advice, or paying commission on products someone else profits from?

Does the person guiding your portfolio have a legal duty to put you first?

When markets fall, who is accountable for the advice you followed?

We wrote this guide to make the choice clear. It compares a SEBI RIA vs broker across role, regulation, fees, and fit. By the end, you will know which one your goals need.

TL;DR

A SEBI RIA is a fiduciary bound by law to act in your interest, while a broker is an execution intermediary.

The heart of the SEBI RIA vs broker gap is payment: advisory fees versus brokerage and product commissions.

RIAs charge a flat fee or a share of assets, so their income does not depend on how often you trade.

A broker cannot charge brokerage on advice given in an RIA capacity, which keeps advice and execution apart.

Choose an RIA for planning and unbiased guidance, and a broker for low cost trade execution.

The same group can offer both, as long as the advisory and broking arms stay separate.

What Is a SEBI Registered Investment Advisor (RIA)?

A SEBI registered investment advisor is a professional licensed to give personalised financial advice for a fee. Registration is not a formality. Every RIA must clear the NISM investment adviser exams and hold a SEBI number before advising a single client.

In the SEBI RIA vs broker comparison, three features define an RIA:

Fiduciary duty: a legal obligation to place your interest ahead of their own.

Fee-only income: paid by you, not by the companies whose products they recommend.

No commission conflict: they cannot earn brokerage on the advice they give.

This structure is why an RIA sits on your side of the table. You can read the detail in our guide to the SEBI RIA in India.

What Is a Stock Broker in India?

A stock broker is a SEBI registered intermediary that executes your buy and sell orders. The broker gives you exchange access, a trading platform, and a demat account. Their core job is execution, not planning.

Brokers earn through brokerage on each trade, and sometimes through commissions on products they distribute. In the SEBI RIA vs broker setup, a broker follows a suitability standard. A product only has to be suitable for you, not the best option available. That difference in duty changes everything.

SEBI RIA vs Broker: Core Differences at a Glance

The clearest way to see the SEBI RIA vs broker difference is side by side. The visual below maps how each one earns, what each owes you by law, and what each is built to do.

SEBI RIA vs Broker: core differences at a glance.

The Important Regulatory Difference: Advice, Distribution and Implementation

Myth: An RIA Cannot Help You Implement Advice

Reality: An RIA may offer implementation services through direct schemes or products, provided there is no commission or referral income and the client is not required to use that service.

Myth: A Broker Cannot Give Any Advice

Reality: A SEBI-registered broker may offer basic advice that is incidental to its broking activity for existing broking clients.

Myth: Every Financial Professional Can Be Paid Both Ways

Reality: Individual IAs cannot provide distribution services. Non-individual IAs must maintain clear segregation between advisory and distribution clients.

Myth: RIA Registration Guarantees Returns

Reality: RIA registration does not assure investment outcomes. It means the adviser is subject to SEBI rules on fiduciary conduct, risk profiling, disclosures, and suitability.

Fee-Only vs Commission: What Each Model Costs You

Fees decide how much of your return you keep. In the SEBI RIA vs broker choice, a fee-only adviser charges a transparent, agreed amount. A broker earns from activity, so cost rises with every trade and every commission bearing product.

On a large portfolio, that gap adds up. The chart shows an illustrative yearly cost on a Rs.50 lakh portfolio, comparing a fee-only advisory model with a commission led broking model.

Illustrative annual cost on a Rs.50 lakh portfolio. Example only, not a quote.

Lower visible cost is not always lower real cost. Hidden commissions can quietly outweigh a clear advisory fee.

When Should You Choose a SEBI RIA vs a Broker?

The right answer depends on what you need. The SEBI RIA vs broker decision comes down to whether you want guidance or only access to the market.

When to choose a SEBI RIA, a broker, or both.

When to Choose a SEBI RIA

Choose an RIA when you want a plan, not just a trade. If you are building a retirement corpus, managing an ESOP windfall, or want unbiased advice across your whole portfolio, a fiduciary adviser fits. Our investment approaches are built around this kind of goal based planning.

When to Choose a Stock Broker

Choose a broker when you already know what you want to buy. Active traders and self-directed investors who value low cost execution are well served by a broker alone.

Can a SEBI RIA and Broker Overlap?

Yes, and many investors use both. You can take fee-only advice from an RIA and execute through a broker. The rule is that the two functions stay separate, so your advice stays unbiased.

Why Should You Choose Ckredence Wealth?

When the SEBI RIA vs broker choice comes down to trust, credentials matter. We are a SEBI registered investment advisor (INA000020846) and a SEBI registered portfolio manager (INP000007164), built on a 37 year legacy since 1987.

Solutions That Matter:

Fee-only, fiduciary advice with no commission conflict on the guidance we give.

A dedicated RIA principal officer and research led portfolio management.

Goal based planning across retirement, direct equity, and wealth structuring.

Whether you are moving beyond a broker relationship or building your first advised portfolio, we act on your side of the table. Ready to transform your investment approach? Schedule a Consultation!

Conclusion

The SEBI RIA vs broker choice comes down to whose interest comes first. A broker gives you access and execution, and earns from how much you trade. A SEBI RIA gives you advice that the law binds to your benefit. One helps you act, the other helps you decide.

Before you sign with either, read how they are paid, because payment shapes behaviour. Most serious investors eventually use both, each for what it does best. As your portfolio grows past mutual funds, advised management becomes the practical next step. Match the role to the job, and your outcome stays protected.

FAQs

01.

What is the main difference between a SEBI RIA and a broker?

A SEBI RIA gives fee-only, fiduciary advice. A broker executes trades and earns brokerage. One advises, the other executes.

02.

Can the same firm be both an RIA and a broker?

Yes, but the advisory and broking arms must stay separate. A broker cannot charge brokerage on advice given as an RIA.

03.

Do SEBI registered investment advisors charge commission?

No. RIAs are paid directly by clients through fees. They cannot earn commission on the advice they provide.

04.

Is a SEBI RIA worth it for a smaller portfolio?

It depends on your need for planning. Fee-only advice suits investors who want unbiased, goal based guidance over product selling.