8 Min Read

8 Min Read

Specialized Investment Funds (SIF): Understanding SEBI's New Investment Option for High-Net-Worth Investors

Specialized Investment Funds (SIF): Understanding SEBI's New Investment Option for High-Net-Worth Investors

Specialized Investment Funds (SIF): Understanding SEBI's New Investment Option for High-Net-Worth Investors

Learn how Specialized Investment Funds work, compare SIFs with mutual funds, PMS and AIFs, and assess whether they suit your portfolio.

Learn how Specialized Investment Funds work, compare SIFs with mutual funds, PMS and AIFs, and assess whether they suit your portfolio.

Learn how Specialized Investment Funds work, compare SIFs with mutual funds, PMS and AIFs, and assess whether they suit your portfolio.

Ckredence Wealth

Ckredence Wealth

|

Specialized Investment Funds entered India’s investment framework when SEBI’s SIF rules took effect in April 2025. The framework allows permitted unhedged derivative exposure up to 25% of a strategy’s net assets and sets a ₹10 lakh aggregate entry threshold at the PAN level within one AMC, except for accredited investors.

Does the SIF allocation come from true long-term surplus or money needed for another goal?

Does the strategy add something your mutual funds, PMS, debt holdings, or cash allocation do not already provide?

Can you stay invested when early NAV movement does not match expectations?

Specialized Investment Funds sit between traditional mutual funds and portfolio management services in terms of flexibility and entry requirement. That does not make them a core holding by default. It means the investor must read the strategy, liquidity terms, costs, and portfolio role before subscribing.

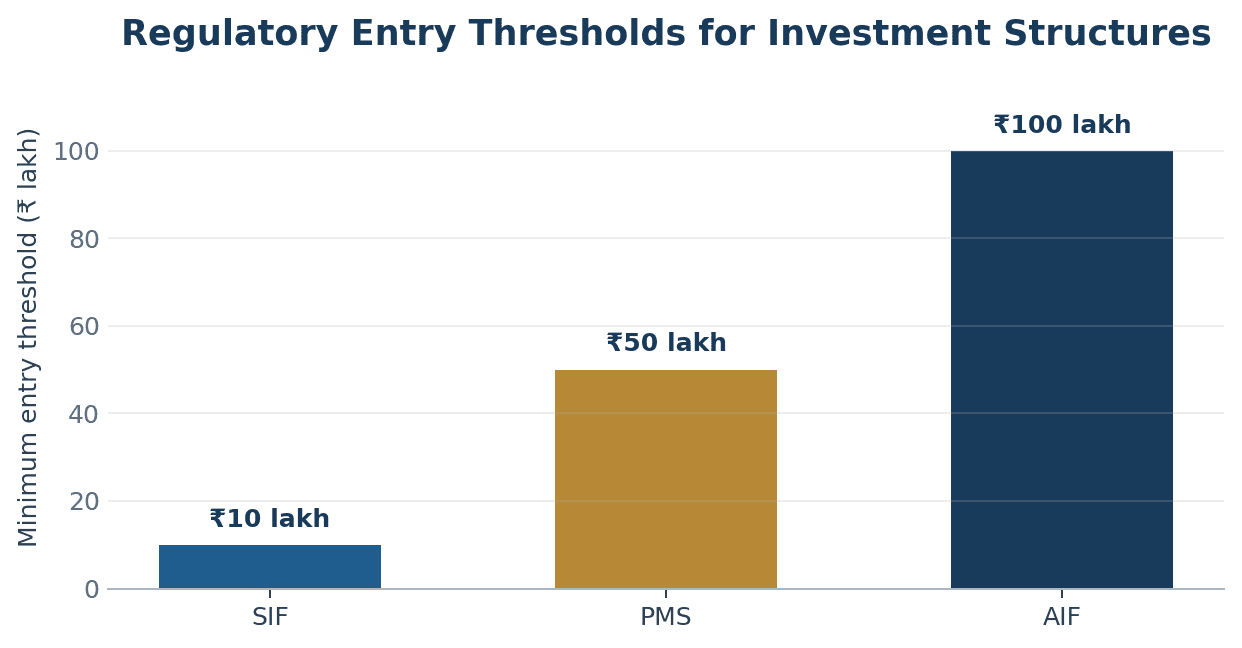

Regulatory Entry Thresholds for Investment Structures

Source: SEBI SIF Regulatory Framework | SEBI PMS Investor Guidance | SEBI AIF Regulations

TL;DR

Specialized Investment Funds are SEBI-regulated, strategy-led pooled investment products.

They offer more flexibility than standard mutual fund schemes.

Long-short exposure does not mean a SIF will profit during every market decline.

The entry threshold is a regulatory rule, not proof that the product suits you.

Liquidity, expense ratio, plan type, risk band, and benchmark need review before investing.

A short return record should not become the main reason to subscribe or exit.

SIFs may fit as a limited allocation after core goals, emergency needs, and basic asset allocation are addressed.

What Are Specialized Investment Funds?

Specialized Investment Funds are pooled investment strategies offered under the SEBI mutual fund framework. They allow eligible AMCs to run defined equity, debt, and hybrid long-short strategies with more flexibility than standard mutual fund categories.

The category was introduced to address the space between retail mutual funds and PMS structures. SIF investors own units of a pooled strategy, while PMS clients generally hold securities through a separate client-level portfolio.

What Specialized Investment Funds Can Include

SEBI permits specified strategy categories across equity, debt, and hybrid investments. These can include equity long-short, sector rotation long-short, debt long-short, sectoral debt long-short, hybrid long-short, and active asset allocation strategies.

Each strategy must follow its investment objective and applicable limits. Investors should read the Investment Strategy Information Document before treating a strategy name as a reason to invest.

What Specialized Investment Funds Are Not

Specialized Investment Funds are not fixed-return products. They are also not substitutes for emergency reserves, near-term property funds, education commitments, or money needed for business working capital.

A SIF should have a stated role in the portfolio. It should not be added merely because it is newer than a mutual fund or has a lower entry threshold than PMS.

Key Characteristics of Specialized Investment Funds

Specialized Investment Funds have rules that differ from standard mutual fund categories. The product structure can affect liquidity, volatility, reporting, and the way an investor reviews performance.

The key characteristics matter more than the fund name. Read them before comparing one SIF with another.

1. A PAN-Level Minimum Investment Requirement

SEBI applies the SIF entry threshold at the investor’s PAN level across all SIF strategies from the same AMC. Investments in that AMC’s regular mutual fund schemes do not count toward this SIF threshold.

The threshold is monitored at the strategy level under SEBI’s framework. A fall in value due to NAV movement is treated differently from a fall caused by an investor-led redemption.

2. Defined Strategy Categories

SIFs do not have unlimited freedom to invest anywhere. They must follow permitted categories and the investment approach stated in their offer documents.

Equity strategies may use long-short positions. Debt and hybrid strategies may use different asset combinations, subject to the limits and terms stated for the strategy.

3. Limited Unhedged Short Exposure

SIFs can take unhedged short exposure through permitted exchange-traded derivatives within SEBI’s stated limit. This gives fund managers a different set of tools than a standard long-only mutual fund.

That flexibility also creates a different risk profile. A short position can hurt when the manager’s call, timing, or security selection does not work.

4. Strategy-Specific Liquidity Terms

Redemption availability can differ across Specialized Investment Funds. Some strategies may permit more frequent redemptions, while others may use interval structures or notice periods.

Read the redemption schedule before investing. A fund can be suitable for long-term capital but unsuitable for money you may need quickly.

5. Risk Band and Disclosure Requirements

SIFs use a risk-band disclosure that shows the strategy’s risk level. The AMC must also publish offer documents, risk information, benchmark details, and portfolio disclosures under the applicable framework.

Do not rely on a short social-media summary. The Investment Strategy Information Document gives the fuller picture of assets, derivatives, liquidity, costs, and risk factors.

6. Plan Type and Expense Review

Before investing, confirm whether the SIF is available through a direct plan, regular plan, or another route stated by the AMC. The plan route can affect costs and service support.

Also review the total expense ratio, exit terms, and any transaction-related charges. Cost should be understood alongside the strategy’s actual purpose in your portfolio.

₹10 lakh gets an investor through a regulatory gate. It does not answer whether the money should move from mutual funds, debt holdings, PMS, or liquidity reserves. Review your asset allocation before adding a strategy-led product. |

Specialized Investment Funds vs Mutual Funds vs PMS vs AIFs

Specialized Investment Funds are often described as the middle layer between mutual funds and PMS. That description is useful, but it does not explain the different ownership, liquidity, reporting, and investment roles of each structure.

Use this table as a first filter. The right structure depends on your corpus, liquidity need, tax position, and preference for pooled or client-level holdings.

Decision Factor | Specialized Investment Funds | Traditional Mutual Funds | PMS | AIF |

|---|---|---|---|---|

Investment structure | Pooled strategy | Pooled scheme | Client-level managed portfolio | Pooled alternative investment vehicle |

Regulatory entry level | SIF threshold | Scheme-specific entry | PMS threshold | AIF threshold |

Portfolio style | Strategy-led and flexible | Category-led and often long-only | More client-level flexibility | Fund-specific and often private-market focused |

Derivative use | Permitted within SIF rules | Category and scheme specific | Mandate specific | Category and fund specific |

Liquidity | Strategy specific | Often more frequent | Agreement and holdings dependent | Fund tenure and terms dependent |

Investor role | Unit holder | Unit holder | Portfolio client | Fund investor |

Typical portfolio role | Satellite allocation | Core and goal-based allocation | Custom listed-market allocation | Alternative allocation |

Traditional mutual funds can work well for core goals, SIP planning, and broad asset allocation. PMS may suit investors seeking a separate managed portfolio, while AIFs can serve investors who understand longer holding periods and fund-specific structures.

Before comparing performance, compare the structure itself. Our guide on PMS vs mutual funds vs AIFs in India explains how ownership, liquidity, and investor control differ across these options.

A lower entry threshold than PMS does not make Specialized Investment Funds low-risk. The strategy, liquidity terms, derivative use, and portfolio concentration still need review. Read the difference between PMS and AIF structures before making a high-value allocation. |

How Long-Short Specialized Investment Funds Work

Long-short Specialized Investment Funds hold investments expected to rise while taking permitted short exposure through derivatives. The fund manager is trying to use both positive and negative market views within the stated strategy rules.

This can create a return pattern that differs from a long-only equity fund. It does not remove market risk or make the strategy suitable for every investor.

Myth: A Long-Short SIF Always Profits in Falling Markets

A short position may help when the market or security view is correct. It may not help when prices move in the opposite direction or when the hedge is incomplete.

The result depends on the manager’s research, portfolio construction, timing, and risk limits. There is no automatic downside protection.

Myth: Long-Short Means Low Risk

Long-short strategies may hold both long and short exposures, but both sides can create losses. Derivatives also need separate risk analysis because their behaviour can differ from cash equity and debt holdings.

The risk band and offer document should guide the investor. Do not judge risk from the word “hedged” alone.

Myth: Early NAV Performance Proves Strategy Quality

Specialized Investment Funds are still a new category in India. A few months of NAV movement cannot show how a strategy may behave through different market phases.

Compare the strategy with its benchmark and stated objective. Then review whether the exposure, liquidity terms, and risk level remain suitable for your allocation.

“Investments in Specialized Investment Fund involves relatively higher risk including potential loss of capital, liquidity risk and market volatility.” Source: SEBI SIF Regulatory Framework |

Who Should Consider Specialized Investment Funds?

Specialized Investment Funds may suit investors who already have their basic financial structure in place. They can be considered when the money is long-term in nature, the investor understands the strategy, and the allocation has a clear purpose.

The product is not only for a particular profession or salary level. It is more relevant to the investor’s total portfolio, liquidity needs, and ability to hold through uncertain periods.

Specialized Investment Funds May Be Worth Reviewing When

Investor Situation | Why a SIF May Be Relevant |

|---|---|

Core goals are already funded | The SIF can remain a limited, separate allocation |

Existing portfolio needs a defined strategy layer | The investor can assess whether it adds a distinct role |

Liquidity needs are already covered | Redemption timing is less likely to disrupt personal plans |

Investor understands long-short exposure | The risk and return pattern is less likely to create surprise |

Investor can review documents and benchmark | Decisions are based on facts rather than launch excitement |

Specialized Investment Funds May Not Fit Now When

Investor Situation | Why Waiting May Be Better |

|---|---|

The SIF amount represents most investible savings | Portfolio concentration can become too high |

Near-term expenses are uncertain | Liquidity terms may not suit the investor |

Core mutual fund and debt allocation is not in place | A strategy-led fund may not be the first requirement |

The investor expects assured protection in falling markets | Long-short exposure does not offer certainty |

The purchase is based mainly on recent NAV movement | Short records can create weak conclusions |

Can a Salaried Investor Invest in Specialized Investment Funds?

A salaried investor can invest in a SIF if the allocation comes after emergency reserves, insurance needs, debt obligations, and near-term goals are handled. Salary type does not decide suitability by itself.

The larger question is whether the SIF amount is separate from money required for a house purchase, family commitment, education goal, or job transition. A financial advisor in India can help assess this portfolio-level question before product selection.

How to Invest in Specialized Investment Funds in India

Specialized Investment Funds may be available through an AMC’s own website, authorised distributors, MFU, registrars, or other routes named in the offer document. Availability can vary by AMC, strategy, and platform.

Do not assume every SIF will appear on the same online investment app. Confirm the route before planning the allocation.

1. Read the Investment Strategy Information Document

The ISID explains the strategy objective, asset mix, benchmark, risk factors, liquidity terms, and permitted exposure. It is the main document for deciding whether the SIF fits your portfolio.

Read the strategy first. Do not start with a return chart or a launch advertisement.

2. Check the Investment and Redemption Structure

Check whether the strategy is open-ended, interval-based, or has a notice period. Subscription frequency and redemption frequency may also differ.

This matters when the capital may be needed for a business payment, property commitment, or family expense. Liquidity should match the purpose of the money.

3. Confirm the Investment Route

Ask whether the investment route is direct, regular, distributor-led, or available through a specific platform. Also confirm KYC requirements, account setup, and transaction timing.

SEBI permits AMCs to offer systematic investment, withdrawal, and transfer options for SIFs, subject to the applicable entry threshold. Actual availability must still be checked in the strategy documents.

4. Record the Role Before Investing

Write down why the SIF is being added. The reason might be a long-short allocation, sector view, debt positioning, or a diversified asset mix.

A written role makes later reviews easier. It also reduces the habit of changing allocations based on short-term headlines.

5. Keep the Core Portfolio Separate

A SIF should be reviewed alongside mutual funds, debt allocation, direct equity, PMS, AIFs, and cash reserves. It should not be treated as an isolated purchase.

Our guide on portfolio management strategies explains why every allocation needs a defined objective, risk level, and time horizon.

Read our portfolio management strategies guide.

How to Track Specialized Investment Funds Without Rushing to Judge Them

SIF tracking should focus on the strategy’s stated role, not only daily NAV movement. The right review asks whether the fund is behaving in a way that matches its investment objective and risk disclosures.

A short operating record needs patience. It also needs better questions.

Review the Benchmark and Investment Objective

Compare performance with the benchmark named in the offer document. The benchmark should relate to the strategy’s asset mix and investment approach.

Do not compare a long-short strategy only with a broad equity index. The strategy may hold different exposures and may behave differently in changing market conditions.

Review the Risk Band and Strategy Disclosures

Check the published risk band, investment objective, and portfolio disclosures. A change in risk level or positioning may matter more than a small movement in NAV.

SEBI requires SIF risk-band and portfolio disclosures under its framework. Investors should use these disclosures rather than relying only on third-party summaries.

Review Costs, Liquidity, and Plan Route

Expense ratio, exit terms, and redemption frequency affect the investor’s actual experience. They should be reviewed with the same care as returns.

A direct plan and regular plan may differ in cost and service support. Compare both only after understanding the route and role of the allocation.

Review the SIF Against Your Existing Holdings

A SIF may add hidden overlap with existing equity, debt, or sector exposure. It can also change the total risk of the portfolio more than expected.

Our guide on equity versus debt mutual funds can help you review the base allocation before adding a strategy-led investment layer.

“Past performance may or may not be sustained in future.” |

Why Choose Ckredence Wealth for Specialized Investment Funds Review?

A Specialized Investment Fund should fit into a full portfolio, not sit beside it without purpose. At Ckredence Wealth, we start with your goals, present holdings, liquidity needs, tax context, and risk capacity before discussing a new strategy-led allocation.

Our review focuses on:

Whether the SIF adds a real role beyond existing mutual funds, PMS holdings, debt allocation, and cash reserves.

Whether liquidity terms fit your expected business, family, or personal commitments.

Whether the strategy creates overlap with your current equity, sector, or derivative exposure.

Whether the allocation size reflects your broader wealth plan.

For investors who need a wider investment view, our financial advisory services guide explains how product decisions should connect with long-term goals.

Bring your current holdings, upcoming cash needs, and the SIF offer document. Leave with a clear view of what the strategy adds, what it duplicates, and what it may displace. Request a Portfolio Fit Review |

Conclusion

Specialized Investment Funds offer a regulated path for strategy-led investing between traditional mutual funds and PMS. Their flexibility can suit investors who understand long-short exposure, strategy-specific liquidity, derivative risk, and the importance of a limited allocation.

The first question should not be which SIF has shown the best early return. It should be whether the strategy fits your existing portfolio, financial goals, liquidity needs, and comfort with risk. A clear role makes it easier to hold or exit a SIF for the right reason.

FAQs

01.

What are Specialized Investment Funds?

Specialized Investment Funds are SEBI-regulated, strategy-led pooled investment products. They offer more flexibility than standard mutual fund categories.

02.

What is the minimum investment required for Specialized Investment Funds?

The SIF threshold is ₹10 lakh at PAN level within one AMC. Accredited investors may receive an exemption under SEBI rules.

03.

Can Specialized Investment Funds protect investors during market falls?

No, SIFs cannot guarantee protection during market falls. Long-short positions work only when the manager’s market view proves correct.

04.

How can investors buy and track Specialized Investment Funds in India?

Investors can use routes stated by the AMC or authorised distributor. Track NAV, benchmark, risk band, costs, liquidity terms, and portfolio disclosures.

Specialized Investment Funds entered India’s investment framework when SEBI’s SIF rules took effect in April 2025. The framework allows permitted unhedged derivative exposure up to 25% of a strategy’s net assets and sets a ₹10 lakh aggregate entry threshold at the PAN level within one AMC, except for accredited investors.

Does the SIF allocation come from true long-term surplus or money needed for another goal?

Does the strategy add something your mutual funds, PMS, debt holdings, or cash allocation do not already provide?

Can you stay invested when early NAV movement does not match expectations?

Specialized Investment Funds sit between traditional mutual funds and portfolio management services in terms of flexibility and entry requirement. That does not make them a core holding by default. It means the investor must read the strategy, liquidity terms, costs, and portfolio role before subscribing.

Regulatory Entry Thresholds for Investment Structures

Source: SEBI SIF Regulatory Framework | SEBI PMS Investor Guidance | SEBI AIF Regulations

TL;DR

Specialized Investment Funds are SEBI-regulated, strategy-led pooled investment products.

They offer more flexibility than standard mutual fund schemes.

Long-short exposure does not mean a SIF will profit during every market decline.

The entry threshold is a regulatory rule, not proof that the product suits you.

Liquidity, expense ratio, plan type, risk band, and benchmark need review before investing.

A short return record should not become the main reason to subscribe or exit.

SIFs may fit as a limited allocation after core goals, emergency needs, and basic asset allocation are addressed.

What Are Specialized Investment Funds?

Specialized Investment Funds are pooled investment strategies offered under the SEBI mutual fund framework. They allow eligible AMCs to run defined equity, debt, and hybrid long-short strategies with more flexibility than standard mutual fund categories.

The category was introduced to address the space between retail mutual funds and PMS structures. SIF investors own units of a pooled strategy, while PMS clients generally hold securities through a separate client-level portfolio.

What Specialized Investment Funds Can Include

SEBI permits specified strategy categories across equity, debt, and hybrid investments. These can include equity long-short, sector rotation long-short, debt long-short, sectoral debt long-short, hybrid long-short, and active asset allocation strategies.

Each strategy must follow its investment objective and applicable limits. Investors should read the Investment Strategy Information Document before treating a strategy name as a reason to invest.

What Specialized Investment Funds Are Not

Specialized Investment Funds are not fixed-return products. They are also not substitutes for emergency reserves, near-term property funds, education commitments, or money needed for business working capital.

A SIF should have a stated role in the portfolio. It should not be added merely because it is newer than a mutual fund or has a lower entry threshold than PMS.

Key Characteristics of Specialized Investment Funds

Specialized Investment Funds have rules that differ from standard mutual fund categories. The product structure can affect liquidity, volatility, reporting, and the way an investor reviews performance.

The key characteristics matter more than the fund name. Read them before comparing one SIF with another.

1. A PAN-Level Minimum Investment Requirement

SEBI applies the SIF entry threshold at the investor’s PAN level across all SIF strategies from the same AMC. Investments in that AMC’s regular mutual fund schemes do not count toward this SIF threshold.

The threshold is monitored at the strategy level under SEBI’s framework. A fall in value due to NAV movement is treated differently from a fall caused by an investor-led redemption.

2. Defined Strategy Categories

SIFs do not have unlimited freedom to invest anywhere. They must follow permitted categories and the investment approach stated in their offer documents.

Equity strategies may use long-short positions. Debt and hybrid strategies may use different asset combinations, subject to the limits and terms stated for the strategy.

3. Limited Unhedged Short Exposure

SIFs can take unhedged short exposure through permitted exchange-traded derivatives within SEBI’s stated limit. This gives fund managers a different set of tools than a standard long-only mutual fund.

That flexibility also creates a different risk profile. A short position can hurt when the manager’s call, timing, or security selection does not work.

4. Strategy-Specific Liquidity Terms

Redemption availability can differ across Specialized Investment Funds. Some strategies may permit more frequent redemptions, while others may use interval structures or notice periods.

Read the redemption schedule before investing. A fund can be suitable for long-term capital but unsuitable for money you may need quickly.

5. Risk Band and Disclosure Requirements

SIFs use a risk-band disclosure that shows the strategy’s risk level. The AMC must also publish offer documents, risk information, benchmark details, and portfolio disclosures under the applicable framework.

Do not rely on a short social-media summary. The Investment Strategy Information Document gives the fuller picture of assets, derivatives, liquidity, costs, and risk factors.

6. Plan Type and Expense Review

Before investing, confirm whether the SIF is available through a direct plan, regular plan, or another route stated by the AMC. The plan route can affect costs and service support.

Also review the total expense ratio, exit terms, and any transaction-related charges. Cost should be understood alongside the strategy’s actual purpose in your portfolio.

₹10 lakh gets an investor through a regulatory gate. It does not answer whether the money should move from mutual funds, debt holdings, PMS, or liquidity reserves. Review your asset allocation before adding a strategy-led product. |

Specialized Investment Funds vs Mutual Funds vs PMS vs AIFs

Specialized Investment Funds are often described as the middle layer between mutual funds and PMS. That description is useful, but it does not explain the different ownership, liquidity, reporting, and investment roles of each structure.

Use this table as a first filter. The right structure depends on your corpus, liquidity need, tax position, and preference for pooled or client-level holdings.

Decision Factor | Specialized Investment Funds | Traditional Mutual Funds | PMS | AIF |

|---|---|---|---|---|

Investment structure | Pooled strategy | Pooled scheme | Client-level managed portfolio | Pooled alternative investment vehicle |

Regulatory entry level | SIF threshold | Scheme-specific entry | PMS threshold | AIF threshold |

Portfolio style | Strategy-led and flexible | Category-led and often long-only | More client-level flexibility | Fund-specific and often private-market focused |

Derivative use | Permitted within SIF rules | Category and scheme specific | Mandate specific | Category and fund specific |

Liquidity | Strategy specific | Often more frequent | Agreement and holdings dependent | Fund tenure and terms dependent |

Investor role | Unit holder | Unit holder | Portfolio client | Fund investor |

Typical portfolio role | Satellite allocation | Core and goal-based allocation | Custom listed-market allocation | Alternative allocation |

Traditional mutual funds can work well for core goals, SIP planning, and broad asset allocation. PMS may suit investors seeking a separate managed portfolio, while AIFs can serve investors who understand longer holding periods and fund-specific structures.

Before comparing performance, compare the structure itself. Our guide on PMS vs mutual funds vs AIFs in India explains how ownership, liquidity, and investor control differ across these options.

A lower entry threshold than PMS does not make Specialized Investment Funds low-risk. The strategy, liquidity terms, derivative use, and portfolio concentration still need review. Read the difference between PMS and AIF structures before making a high-value allocation. |

How Long-Short Specialized Investment Funds Work

Long-short Specialized Investment Funds hold investments expected to rise while taking permitted short exposure through derivatives. The fund manager is trying to use both positive and negative market views within the stated strategy rules.

This can create a return pattern that differs from a long-only equity fund. It does not remove market risk or make the strategy suitable for every investor.

Myth: A Long-Short SIF Always Profits in Falling Markets

A short position may help when the market or security view is correct. It may not help when prices move in the opposite direction or when the hedge is incomplete.

The result depends on the manager’s research, portfolio construction, timing, and risk limits. There is no automatic downside protection.

Myth: Long-Short Means Low Risk

Long-short strategies may hold both long and short exposures, but both sides can create losses. Derivatives also need separate risk analysis because their behaviour can differ from cash equity and debt holdings.

The risk band and offer document should guide the investor. Do not judge risk from the word “hedged” alone.

Myth: Early NAV Performance Proves Strategy Quality

Specialized Investment Funds are still a new category in India. A few months of NAV movement cannot show how a strategy may behave through different market phases.

Compare the strategy with its benchmark and stated objective. Then review whether the exposure, liquidity terms, and risk level remain suitable for your allocation.

“Investments in Specialized Investment Fund involves relatively higher risk including potential loss of capital, liquidity risk and market volatility.” Source: SEBI SIF Regulatory Framework |

Who Should Consider Specialized Investment Funds?

Specialized Investment Funds may suit investors who already have their basic financial structure in place. They can be considered when the money is long-term in nature, the investor understands the strategy, and the allocation has a clear purpose.

The product is not only for a particular profession or salary level. It is more relevant to the investor’s total portfolio, liquidity needs, and ability to hold through uncertain periods.

Specialized Investment Funds May Be Worth Reviewing When

Investor Situation | Why a SIF May Be Relevant |

|---|---|

Core goals are already funded | The SIF can remain a limited, separate allocation |

Existing portfolio needs a defined strategy layer | The investor can assess whether it adds a distinct role |

Liquidity needs are already covered | Redemption timing is less likely to disrupt personal plans |

Investor understands long-short exposure | The risk and return pattern is less likely to create surprise |

Investor can review documents and benchmark | Decisions are based on facts rather than launch excitement |

Specialized Investment Funds May Not Fit Now When

Investor Situation | Why Waiting May Be Better |

|---|---|

The SIF amount represents most investible savings | Portfolio concentration can become too high |

Near-term expenses are uncertain | Liquidity terms may not suit the investor |

Core mutual fund and debt allocation is not in place | A strategy-led fund may not be the first requirement |

The investor expects assured protection in falling markets | Long-short exposure does not offer certainty |

The purchase is based mainly on recent NAV movement | Short records can create weak conclusions |

Can a Salaried Investor Invest in Specialized Investment Funds?

A salaried investor can invest in a SIF if the allocation comes after emergency reserves, insurance needs, debt obligations, and near-term goals are handled. Salary type does not decide suitability by itself.

The larger question is whether the SIF amount is separate from money required for a house purchase, family commitment, education goal, or job transition. A financial advisor in India can help assess this portfolio-level question before product selection.

How to Invest in Specialized Investment Funds in India

Specialized Investment Funds may be available through an AMC’s own website, authorised distributors, MFU, registrars, or other routes named in the offer document. Availability can vary by AMC, strategy, and platform.

Do not assume every SIF will appear on the same online investment app. Confirm the route before planning the allocation.

1. Read the Investment Strategy Information Document

The ISID explains the strategy objective, asset mix, benchmark, risk factors, liquidity terms, and permitted exposure. It is the main document for deciding whether the SIF fits your portfolio.

Read the strategy first. Do not start with a return chart or a launch advertisement.

2. Check the Investment and Redemption Structure

Check whether the strategy is open-ended, interval-based, or has a notice period. Subscription frequency and redemption frequency may also differ.

This matters when the capital may be needed for a business payment, property commitment, or family expense. Liquidity should match the purpose of the money.

3. Confirm the Investment Route

Ask whether the investment route is direct, regular, distributor-led, or available through a specific platform. Also confirm KYC requirements, account setup, and transaction timing.

SEBI permits AMCs to offer systematic investment, withdrawal, and transfer options for SIFs, subject to the applicable entry threshold. Actual availability must still be checked in the strategy documents.

4. Record the Role Before Investing

Write down why the SIF is being added. The reason might be a long-short allocation, sector view, debt positioning, or a diversified asset mix.

A written role makes later reviews easier. It also reduces the habit of changing allocations based on short-term headlines.

5. Keep the Core Portfolio Separate

A SIF should be reviewed alongside mutual funds, debt allocation, direct equity, PMS, AIFs, and cash reserves. It should not be treated as an isolated purchase.

Our guide on portfolio management strategies explains why every allocation needs a defined objective, risk level, and time horizon.

Read our portfolio management strategies guide.

How to Track Specialized Investment Funds Without Rushing to Judge Them

SIF tracking should focus on the strategy’s stated role, not only daily NAV movement. The right review asks whether the fund is behaving in a way that matches its investment objective and risk disclosures.

A short operating record needs patience. It also needs better questions.

Review the Benchmark and Investment Objective

Compare performance with the benchmark named in the offer document. The benchmark should relate to the strategy’s asset mix and investment approach.

Do not compare a long-short strategy only with a broad equity index. The strategy may hold different exposures and may behave differently in changing market conditions.

Review the Risk Band and Strategy Disclosures

Check the published risk band, investment objective, and portfolio disclosures. A change in risk level or positioning may matter more than a small movement in NAV.

SEBI requires SIF risk-band and portfolio disclosures under its framework. Investors should use these disclosures rather than relying only on third-party summaries.

Review Costs, Liquidity, and Plan Route

Expense ratio, exit terms, and redemption frequency affect the investor’s actual experience. They should be reviewed with the same care as returns.

A direct plan and regular plan may differ in cost and service support. Compare both only after understanding the route and role of the allocation.

Review the SIF Against Your Existing Holdings

A SIF may add hidden overlap with existing equity, debt, or sector exposure. It can also change the total risk of the portfolio more than expected.

Our guide on equity versus debt mutual funds can help you review the base allocation before adding a strategy-led investment layer.

“Past performance may or may not be sustained in future.” |

Why Choose Ckredence Wealth for Specialized Investment Funds Review?

A Specialized Investment Fund should fit into a full portfolio, not sit beside it without purpose. At Ckredence Wealth, we start with your goals, present holdings, liquidity needs, tax context, and risk capacity before discussing a new strategy-led allocation.

Our review focuses on:

Whether the SIF adds a real role beyond existing mutual funds, PMS holdings, debt allocation, and cash reserves.

Whether liquidity terms fit your expected business, family, or personal commitments.

Whether the strategy creates overlap with your current equity, sector, or derivative exposure.

Whether the allocation size reflects your broader wealth plan.

For investors who need a wider investment view, our financial advisory services guide explains how product decisions should connect with long-term goals.

Bring your current holdings, upcoming cash needs, and the SIF offer document. Leave with a clear view of what the strategy adds, what it duplicates, and what it may displace. Request a Portfolio Fit Review |

Conclusion

Specialized Investment Funds offer a regulated path for strategy-led investing between traditional mutual funds and PMS. Their flexibility can suit investors who understand long-short exposure, strategy-specific liquidity, derivative risk, and the importance of a limited allocation.

The first question should not be which SIF has shown the best early return. It should be whether the strategy fits your existing portfolio, financial goals, liquidity needs, and comfort with risk. A clear role makes it easier to hold or exit a SIF for the right reason.

FAQs

01.

What are Specialized Investment Funds?

Specialized Investment Funds are SEBI-regulated, strategy-led pooled investment products. They offer more flexibility than standard mutual fund categories.

02.

What is the minimum investment required for Specialized Investment Funds?

The SIF threshold is ₹10 lakh at PAN level within one AMC. Accredited investors may receive an exemption under SEBI rules.

03.

Can Specialized Investment Funds protect investors during market falls?

No, SIFs cannot guarantee protection during market falls. Long-short positions work only when the manager’s market view proves correct.

04.

How can investors buy and track Specialized Investment Funds in India?

Investors can use routes stated by the AMC or authorised distributor. Track NAV, benchmark, risk band, costs, liquidity terms, and portfolio disclosures.