5 min

5 min

Portfolio Management Services for Doctors in India: Best PMS Options, Costs and How to Choose in 2026

Portfolio Management Services for Doctors in India: Best PMS Options, Costs and How to Choose in 2026

Portfolio Management Services for Doctors in India: Best PMS Options, Costs and How to Choose in 2026

Explore portfolio management services for doctors in India. Learn PMS costs, benefits, risks, SEBI rules, and how to choose the right provider.

Explore portfolio management services for doctors in India. Learn PMS costs, benefits, risks, SEBI rules, and how to choose the right provider.

Explore portfolio management services for doctors in India. Learn PMS costs, benefits, risks, SEBI rules, and how to choose the right provider.

Ckredence Wealth

Ckredence Wealth

|

"A doctor who cannot manage time cannot manage wealth either."

Doctors in India often build strong incomes but weak investment systems.

Long working hours, unpredictable schedules, and delayed financial reviews leave many high-earning professionals stuck between scattered SIPs, idle cash, and underused advisors.

As per SEBI regulations, PMS is available for investors with a minimum of ₹50 lakh, and according to the SEBI Annual Report 2024-25, PMS assets under management in India crossed ₹32 lakh crore in 2024, reflecting how rapidly qualified investors are moving toward professionally managed portfolios.

Is your income rising, but your investments still running on autopilot?

Do you own multiple products but lack one clear portfolio strategy?

If markets change sharply, who is actively reviewing your wealth today?

This is where portfolio management services for doctors in India become relevant. PMS gives qualified investors access to professionally managed portfolios aligned to goals, risk profile, and time constraints.

For doctors who cannot monitor markets daily, this can bring structure, accountability, and clearer long-term wealth planning.

Key Takeaways

PMS requires a minimum of ₹50 lakh and suits doctors with investable surplus at that level

Discretionary PMS is often the better fit for doctors who cannot track markets regularly

Scattered investments across platforms can create review fatigue without real diversification

Fee structures matter, but post-fee performance against a benchmark matters more

Provider selection should start with SEBI registration, not brand name or returns data

What Are Portfolio Management Services for Doctors in India?

Portfolio management services for doctors in India are professionally managed investment solutions designed for eligible investors who want active portfolio oversight.

A PMS manager builds and manages a customised equity or debt portfolio in your name, usually through a Demat-linked structure.

For doctors with high earnings but limited time, PMS can offer structured decision-making, ongoing reviews, and accountability that self-directed investing often lacks.

Our guide to PMS investing walks through how the structure differs from mutual funds in terms of ownership, reporting, and portfolio flexibility.

How PMS Works for Doctors

The portfolio manager creates an investment strategy based on your goals, risk profile, and time horizon.

Investments are monitored regularly and changes are made when needed.

Doctors receive statements, reports, and updates without needing daily involvement.

Discretionary PMS: Full Manager Control

The portfolio manager takes investment decisions on your behalf within the agreed mandate. This is suitable for doctors who do not want day-to-day involvement in markets.

Stock selection, allocation changes, and reviews are handled professionally.

Non-Discretionary PMS: Doctor Decides, Manager Advises

The manager gives recommendations, but execution happens only after your approval.

This suits doctors who want more control over decisions while still benefiting from professional research.

Advisory PMS: Guidance Without Execution

The provider advises on portfolio strategy, but execution remains with the investor. This is less common for doctors looking for a hands-off investment route.

Minimum Investment Requirement

As per SEBI rules, PMS requires a minimum investment of ₹50 lakh.

This places PMS in the high-income investor category.

Many established doctors and clinic owners may qualify for this route.

"The stock market is a device for transferring money from the impatient to the patient." Warren Buffett, Chairman, Berkshire Hathaway

Doctors who invest without a structured review system are often the impatient ones, not by choice, but by schedule. PMS addresses that gap directly.

What Should Doctors Look for in a Portfolio Management Services Provider?

Many doctors compare brand names first. That is not enough. The better approach is to compare filters that actually affect outcomes.

1. SEBI Registration Must Come First

Start with regulatory credibility. A valid SEBI registration is the first non-negotiable checkpoint before discussing returns or products.

2. Multiple Strategies Matter

Some providers run one style only. Better firms offer different approaches such as diversified, all-weather, growth-led, or cycle-based portfolios depending on investor needs.

Our PMS strategy comparison covers how different mandates suit different income profiles and risk appetites.

3. Reporting Should Be Clear

You should understand performance, allocation, benchmark comparison, and actions taken. If reports confuse you, the relationship will weaken over time.

4. AUM and Client Trust Matter

Assets under management and client continuity can signal trust. They should not be the only metric, but they do matter in evaluating provider stability.

5. Relationship Access Is Important for Doctors

Busy professionals need responsive service. If you can never reach your advisor when needed, size alone means little.

📊 If you are comparing PMS providers and the conversation has not moved past returns data, you have not seen the full picture. A risk-adjusted portfolio review looks very different from a raw returns comparison, especially over a 3 to 5 year cycle.

Why Doctors with Multiple Investments Often Build Less Wealth Than Those with One Portfolio Management Service

Many doctors own several mutual funds, insurance-linked plans, direct stocks, fixed deposits, and idle savings balances.

It feels diversified because money is spread across multiple products. In reality, these investments are often built at different times without one clear long-term strategy.

Multiple products across platforms create review fatigue. One account rises, another slips, and another gets ignored. Since there is no single portfolio view, decisions often get delayed because nothing feels urgent.

This is not always diversification. It can become structured neglect, where investments exist but are not actively managed with purpose.

When Diversification Turns Into Fragmentation

Different products may overlap in the same sectors or themes.

Risk can rise without the investor realising it.

Returns may look average because capital is spread without direction.

The Problem With Too Many Platforms

One account may sit with a broker. Another may be with a bank or distributor. A third may be in insurance or legacy holdings.

This creates a situation where tracking becomes irregular and performance comparison becomes difficult.

The Cost of Split Attention

A doctor tracking seven investments casually may monitor none properly. Reviews get pushed to weekends, then to month-end, and then skipped entirely.

Wealth often suffers more from neglect than from volatility.

How One PMS Creates Better Control

A professionally managed PMS can consolidate active capital into one strategy with one review framework, one monthly report, and one accountable manager.

Our portfolio consolidation guide explains how doctors with fragmented holdings can reorganise without triggering unnecessary exits. This creates clarity on allocation, performance, and next steps.

🔍 Managing above ₹50 lakh across multiple platforms with no unified review? A 20-minute portfolio review with a Ckredence advisor can show you exactly where your capital is overlapping and where it is not working.

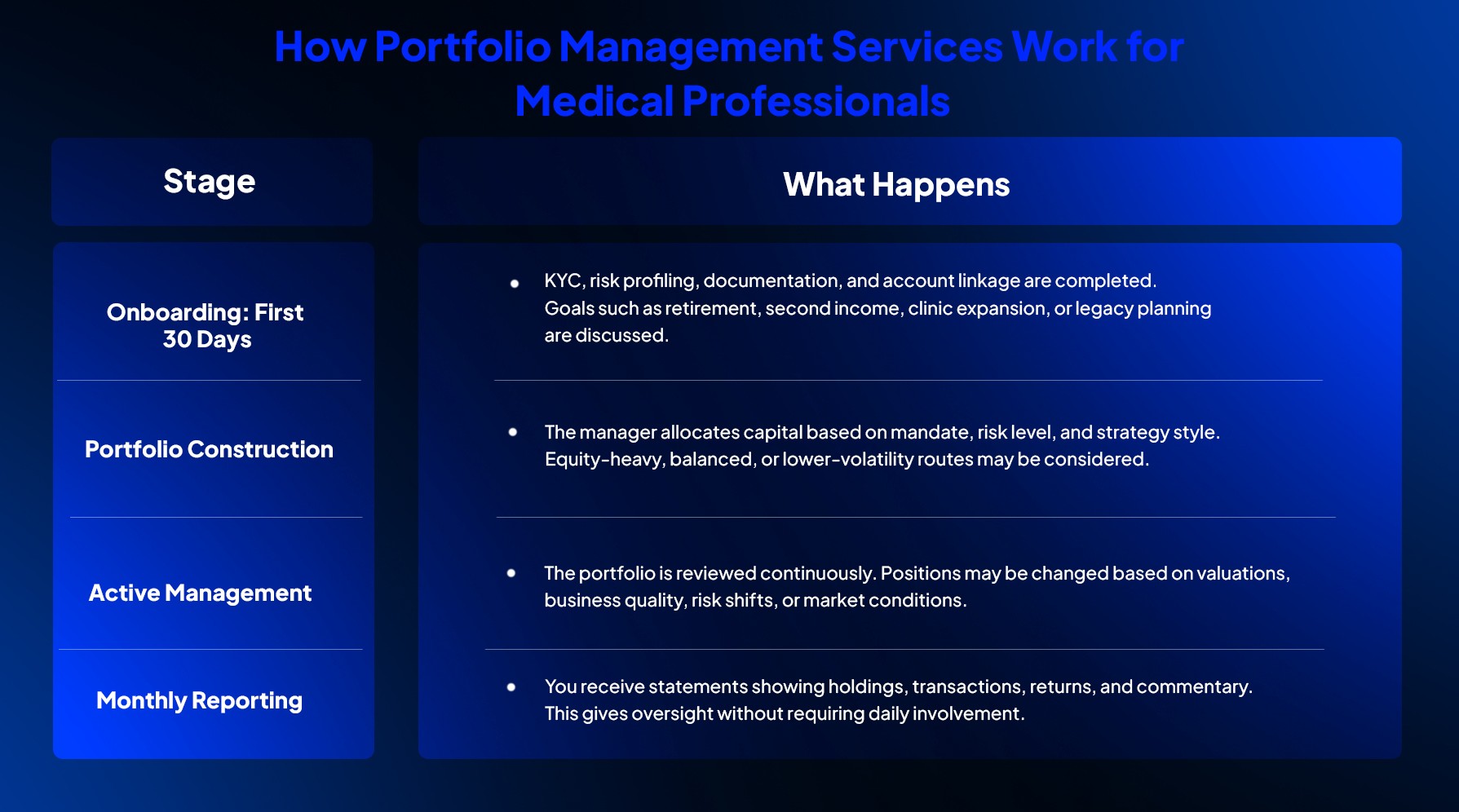

How Portfolio Management Services Work for Medical Professionals

Doctors often ask what happens after investing ₹50 lakh. The process is structured and straightforward.

The overall process is designed to reduce the need for constant personal monitoring. Doctors can stay focused on their profession while the portfolio is managed within an agreed strategy and risk framework.

How SEBI's 2026 Rules Changed Portfolio Management Services for Doctors

PMS in 2026 is easier to evaluate than it was years ago. Regulation and disclosures have improved transparency significantly.

Doctors value evidence. Updated PMS disclosures make provider comparisons more practical and less marketing-led.

SEBI's ₹50 lakh threshold also naturally filters PMS toward affluent investors such as senior doctors and clinic owners, which means the provider ecosystem has adjusted its service standards accordingly.

How Much Do Portfolio Management Services Cost for Doctors in India?

Many investors reject PMS on headline fees alone. That can be a mistake. Fees matter, but so does what the fee buys.

Fixed Management Fee

Some PMS providers charge a fixed annual fee based on assets under management. This pays for active management, research, reviews, and execution oversight.

Performance Fee

Some models charge when returns cross a hurdle level. This can align incentives if structured fairly. Our PMS fee structure guide breaks down how to read the total cost impact across different fee models before committing capital.

Exit Loads

Certain products may charge for early exit within a lock period or defined time window. Liquidity needs should be discussed in advance before signing.

PMS vs Mutual Fund Costs

Mutual funds may look cheaper. PMS may cost more but offers customisation, direct ownership, and active portfolio-level decision-making that pooled structures cannot replicate.

"Price is what you pay. Value is what you get." Warren Buffett, Chairman, Berkshire Hathaway

For doctors evaluating PMS, the right question is not what the fee is. It is what the fee delivers relative to your alternative.

What Are the Real Benefits and Risks of Portfolio Management Services for Doctors?

A balanced investment decision needs both sides. PMS can offer strong advantages for doctors, but it also comes with risks that should be understood clearly before committing capital.

Benefits

Active oversight instead of passive neglect: Portfolios are reviewed regularly rather than left unattended for years.

Strategy matched to goals and risk profile: Investments can be aligned to retirement, wealth growth, second income, or capital preservation goals.

Cleaner reporting and accountability: Investors receive structured statements and clearer performance visibility.

Better use of limited time: Doctors can stay focused on practice while professionals monitor investments.

Risks

Concentration risk if strategy is narrow: Some PMS portfolios may hold fewer positions, which can increase volatility.

Fee drag if returns disappoint: Fees matter more when portfolio performance remains weak for a period.

Liquidity constraints in some cases: Certain structures may involve exit loads or less flexibility in early years.

Manager selection risk: Choosing the wrong provider can lead to poor communication or inconsistent execution.

How Doctors Can Reduce Risk

Choose the right allocation size instead of deploying too much capital at once. Use diversified strategies where suitable and review provider reporting discipline before investing.

It is also wise to align PMS with your broader financial plan rather than treating it as a standalone decision.

How a Cardiologist in Surat Used Portfolio Management Services to Grow ₹70 Lakh to ₹1.2 Crore in 4 Years

The Situation

A cardiologist in Surat had ₹70 lakh spread across SIPs, stocks, and idle balances. He had no review system and limited time for market monitoring.

The Problem

Six active products across platforms. No unified strategy. No regular performance review. Capital was working in different directions without a common mandate.

The Shift

Capital was reorganised into a focused managed approach aligned to growth and oversight needs. A single portfolio manager took over with a clear mandate and monthly reporting structure.

The Outcome

📊 Over four years, the portfolio grew from ₹70 lakh to approximately ₹1.2 crore through disciplined management and compounding. Active monitoring hours dropped close to zero. The doctor returned to reviewing one monthly statement instead of six unconnected accounts.

🧪 Managing above ₹50 lakh and your current portfolio has not had a review meeting in the last 6 months? You are investing without oversight. Here is what a 20-minute portfolio review with a Ckredence advisor looks like.

Why Should Doctors in India Choose Ckredence Wealth for Portfolio Management Services?

Doctors need more than a known brand. They need a provider that understands risk, time scarcity, and long-term planning. Most PMS providers offer the same product to every investor with a different label on it.

Ckredence Wealth builds around your actual income profile, cash-flow pattern, and risk tolerance before any portfolio decision is made.

What Ckredence Offers | Why It Matters for Doctors |

SEBI Registered: INP000007164, RIA: INA000020846 | Full regulatory credibility before any conversation about returns |

37-Year Legacy, established in 1987 | Institutional stability across multiple market cycles |

₹805+ Crore AUM across Gujarat and Maharashtra | Proven trust from active HNI clients in your region |

Four strategies: All Weather, Diversified, Business Cycle, ICE Growth | Multiple mandates for different risk profiles and goals |

Offices in Surat, Mumbai, Vadodara | Regional access with national-grade research |

Whether you run a clinic, own a practice, or earn a high specialist income, the portfolio should fit your real financial life. Not a template. Not a product that was built for someone else and repurposed for you.

🚀 You have compared the options. If you are a doctor managing ₹50 lakh or more and want a portfolio built around your actual risk profile, the next step is a 20-minute conversation.

Conclusion

Portfolio management services for doctors in India are most relevant when income is strong but investment attention is limited. Many doctors qualify financially, yet continue with scattered products and low review discipline. The right PMS can bring structure, professional oversight, and clearer capital direction without demanding more of your time.

Match strategy with goals, not trends. Compare providers beyond returns alone, understand fee models clearly, and choose a long-term relationship built on trust, discipline, and consistent communication. A well-managed portfolio should work as hard as you do.

FAQs

01.

What is the minimum investment required for PMS for doctors in India?

The minimum investment for PMS in India is ₹50 lakh as per SEBI rules. Many established doctors and clinic owners qualify based on surplus capital. This threshold places PMS in the high-income investor category.

02.

Is portfolio management services better than mutual funds for doctors?

PMS offers customisation, direct ownership, and active oversight that mutual funds cannot match. Doctors with higher investable surplus may prefer PMS for a more personalised approach. The right choice depends on your financial goals and time availability.

03.

How do portfolio management services work differently for doctors?

PMS suits doctors because medical professionals have limited time to monitor markets regularly. A professional manager handles portfolio reviews, strategy execution, and reporting. Doctors stay focused on practice while investments are managed systematically.

04.

What PMS charges should doctors in India expect to pay?

Charges vary by provider and fee model across fixed fees, performance fees, and exit loads. It is important to review the total fee impact alongside service quality. Post-fee returns against a benchmark matter more than headline fee comparisons.

"A doctor who cannot manage time cannot manage wealth either."

Doctors in India often build strong incomes but weak investment systems.

Long working hours, unpredictable schedules, and delayed financial reviews leave many high-earning professionals stuck between scattered SIPs, idle cash, and underused advisors.

As per SEBI regulations, PMS is available for investors with a minimum of ₹50 lakh, and according to the SEBI Annual Report 2024-25, PMS assets under management in India crossed ₹32 lakh crore in 2024, reflecting how rapidly qualified investors are moving toward professionally managed portfolios.

Is your income rising, but your investments still running on autopilot?

Do you own multiple products but lack one clear portfolio strategy?

If markets change sharply, who is actively reviewing your wealth today?

This is where portfolio management services for doctors in India become relevant. PMS gives qualified investors access to professionally managed portfolios aligned to goals, risk profile, and time constraints.

For doctors who cannot monitor markets daily, this can bring structure, accountability, and clearer long-term wealth planning.

Key Takeaways

PMS requires a minimum of ₹50 lakh and suits doctors with investable surplus at that level

Discretionary PMS is often the better fit for doctors who cannot track markets regularly

Scattered investments across platforms can create review fatigue without real diversification

Fee structures matter, but post-fee performance against a benchmark matters more

Provider selection should start with SEBI registration, not brand name or returns data

What Are Portfolio Management Services for Doctors in India?

Portfolio management services for doctors in India are professionally managed investment solutions designed for eligible investors who want active portfolio oversight.

A PMS manager builds and manages a customised equity or debt portfolio in your name, usually through a Demat-linked structure.

For doctors with high earnings but limited time, PMS can offer structured decision-making, ongoing reviews, and accountability that self-directed investing often lacks.

Our guide to PMS investing walks through how the structure differs from mutual funds in terms of ownership, reporting, and portfolio flexibility.

How PMS Works for Doctors

The portfolio manager creates an investment strategy based on your goals, risk profile, and time horizon.

Investments are monitored regularly and changes are made when needed.

Doctors receive statements, reports, and updates without needing daily involvement.

Discretionary PMS: Full Manager Control

The portfolio manager takes investment decisions on your behalf within the agreed mandate. This is suitable for doctors who do not want day-to-day involvement in markets.

Stock selection, allocation changes, and reviews are handled professionally.

Non-Discretionary PMS: Doctor Decides, Manager Advises

The manager gives recommendations, but execution happens only after your approval.

This suits doctors who want more control over decisions while still benefiting from professional research.

Advisory PMS: Guidance Without Execution

The provider advises on portfolio strategy, but execution remains with the investor. This is less common for doctors looking for a hands-off investment route.

Minimum Investment Requirement

As per SEBI rules, PMS requires a minimum investment of ₹50 lakh.

This places PMS in the high-income investor category.

Many established doctors and clinic owners may qualify for this route.

"The stock market is a device for transferring money from the impatient to the patient." Warren Buffett, Chairman, Berkshire Hathaway

Doctors who invest without a structured review system are often the impatient ones, not by choice, but by schedule. PMS addresses that gap directly.

What Should Doctors Look for in a Portfolio Management Services Provider?

Many doctors compare brand names first. That is not enough. The better approach is to compare filters that actually affect outcomes.

1. SEBI Registration Must Come First

Start with regulatory credibility. A valid SEBI registration is the first non-negotiable checkpoint before discussing returns or products.

2. Multiple Strategies Matter

Some providers run one style only. Better firms offer different approaches such as diversified, all-weather, growth-led, or cycle-based portfolios depending on investor needs.

Our PMS strategy comparison covers how different mandates suit different income profiles and risk appetites.

3. Reporting Should Be Clear

You should understand performance, allocation, benchmark comparison, and actions taken. If reports confuse you, the relationship will weaken over time.

4. AUM and Client Trust Matter

Assets under management and client continuity can signal trust. They should not be the only metric, but they do matter in evaluating provider stability.

5. Relationship Access Is Important for Doctors

Busy professionals need responsive service. If you can never reach your advisor when needed, size alone means little.

📊 If you are comparing PMS providers and the conversation has not moved past returns data, you have not seen the full picture. A risk-adjusted portfolio review looks very different from a raw returns comparison, especially over a 3 to 5 year cycle.

Why Doctors with Multiple Investments Often Build Less Wealth Than Those with One Portfolio Management Service

Many doctors own several mutual funds, insurance-linked plans, direct stocks, fixed deposits, and idle savings balances.

It feels diversified because money is spread across multiple products. In reality, these investments are often built at different times without one clear long-term strategy.

Multiple products across platforms create review fatigue. One account rises, another slips, and another gets ignored. Since there is no single portfolio view, decisions often get delayed because nothing feels urgent.

This is not always diversification. It can become structured neglect, where investments exist but are not actively managed with purpose.

When Diversification Turns Into Fragmentation

Different products may overlap in the same sectors or themes.

Risk can rise without the investor realising it.

Returns may look average because capital is spread without direction.

The Problem With Too Many Platforms

One account may sit with a broker. Another may be with a bank or distributor. A third may be in insurance or legacy holdings.

This creates a situation where tracking becomes irregular and performance comparison becomes difficult.

The Cost of Split Attention

A doctor tracking seven investments casually may monitor none properly. Reviews get pushed to weekends, then to month-end, and then skipped entirely.

Wealth often suffers more from neglect than from volatility.

How One PMS Creates Better Control

A professionally managed PMS can consolidate active capital into one strategy with one review framework, one monthly report, and one accountable manager.

Our portfolio consolidation guide explains how doctors with fragmented holdings can reorganise without triggering unnecessary exits. This creates clarity on allocation, performance, and next steps.

🔍 Managing above ₹50 lakh across multiple platforms with no unified review? A 20-minute portfolio review with a Ckredence advisor can show you exactly where your capital is overlapping and where it is not working.

How Portfolio Management Services Work for Medical Professionals

Doctors often ask what happens after investing ₹50 lakh. The process is structured and straightforward.

The overall process is designed to reduce the need for constant personal monitoring. Doctors can stay focused on their profession while the portfolio is managed within an agreed strategy and risk framework.

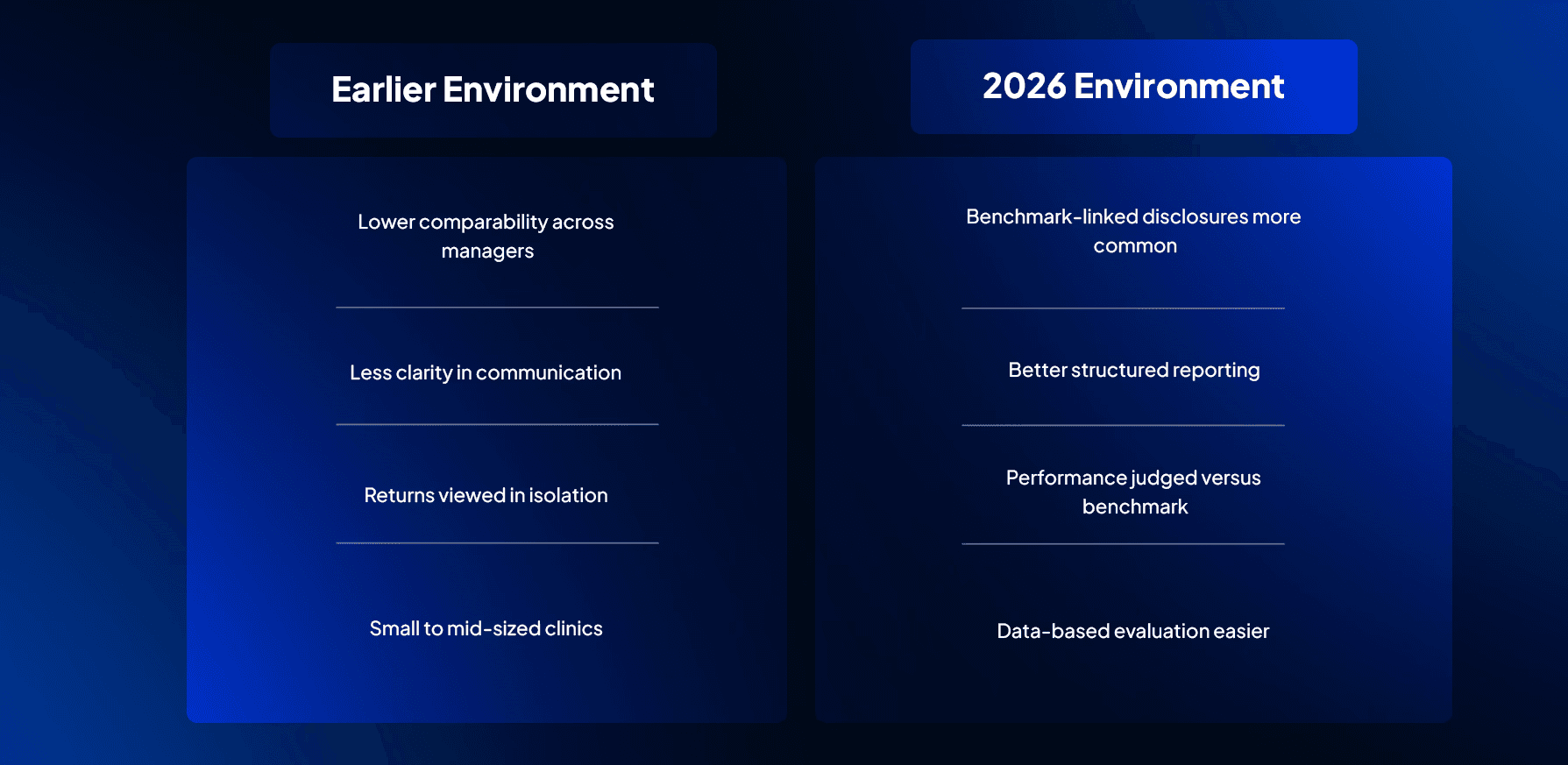

How SEBI's 2026 Rules Changed Portfolio Management Services for Doctors

PMS in 2026 is easier to evaluate than it was years ago. Regulation and disclosures have improved transparency significantly.

Doctors value evidence. Updated PMS disclosures make provider comparisons more practical and less marketing-led.

SEBI's ₹50 lakh threshold also naturally filters PMS toward affluent investors such as senior doctors and clinic owners, which means the provider ecosystem has adjusted its service standards accordingly.

How Much Do Portfolio Management Services Cost for Doctors in India?

Many investors reject PMS on headline fees alone. That can be a mistake. Fees matter, but so does what the fee buys.

Fixed Management Fee

Some PMS providers charge a fixed annual fee based on assets under management. This pays for active management, research, reviews, and execution oversight.

Performance Fee

Some models charge when returns cross a hurdle level. This can align incentives if structured fairly. Our PMS fee structure guide breaks down how to read the total cost impact across different fee models before committing capital.

Exit Loads

Certain products may charge for early exit within a lock period or defined time window. Liquidity needs should be discussed in advance before signing.

PMS vs Mutual Fund Costs

Mutual funds may look cheaper. PMS may cost more but offers customisation, direct ownership, and active portfolio-level decision-making that pooled structures cannot replicate.

"Price is what you pay. Value is what you get." Warren Buffett, Chairman, Berkshire Hathaway

For doctors evaluating PMS, the right question is not what the fee is. It is what the fee delivers relative to your alternative.

What Are the Real Benefits and Risks of Portfolio Management Services for Doctors?

A balanced investment decision needs both sides. PMS can offer strong advantages for doctors, but it also comes with risks that should be understood clearly before committing capital.

Benefits

Active oversight instead of passive neglect: Portfolios are reviewed regularly rather than left unattended for years.

Strategy matched to goals and risk profile: Investments can be aligned to retirement, wealth growth, second income, or capital preservation goals.

Cleaner reporting and accountability: Investors receive structured statements and clearer performance visibility.

Better use of limited time: Doctors can stay focused on practice while professionals monitor investments.

Risks

Concentration risk if strategy is narrow: Some PMS portfolios may hold fewer positions, which can increase volatility.

Fee drag if returns disappoint: Fees matter more when portfolio performance remains weak for a period.

Liquidity constraints in some cases: Certain structures may involve exit loads or less flexibility in early years.

Manager selection risk: Choosing the wrong provider can lead to poor communication or inconsistent execution.

How Doctors Can Reduce Risk

Choose the right allocation size instead of deploying too much capital at once. Use diversified strategies where suitable and review provider reporting discipline before investing.

It is also wise to align PMS with your broader financial plan rather than treating it as a standalone decision.

How a Cardiologist in Surat Used Portfolio Management Services to Grow ₹70 Lakh to ₹1.2 Crore in 4 Years

The Situation

A cardiologist in Surat had ₹70 lakh spread across SIPs, stocks, and idle balances. He had no review system and limited time for market monitoring.

The Problem

Six active products across platforms. No unified strategy. No regular performance review. Capital was working in different directions without a common mandate.

The Shift

Capital was reorganised into a focused managed approach aligned to growth and oversight needs. A single portfolio manager took over with a clear mandate and monthly reporting structure.

The Outcome

📊 Over four years, the portfolio grew from ₹70 lakh to approximately ₹1.2 crore through disciplined management and compounding. Active monitoring hours dropped close to zero. The doctor returned to reviewing one monthly statement instead of six unconnected accounts.

🧪 Managing above ₹50 lakh and your current portfolio has not had a review meeting in the last 6 months? You are investing without oversight. Here is what a 20-minute portfolio review with a Ckredence advisor looks like.

Why Should Doctors in India Choose Ckredence Wealth for Portfolio Management Services?

Doctors need more than a known brand. They need a provider that understands risk, time scarcity, and long-term planning. Most PMS providers offer the same product to every investor with a different label on it.

Ckredence Wealth builds around your actual income profile, cash-flow pattern, and risk tolerance before any portfolio decision is made.

What Ckredence Offers | Why It Matters for Doctors |

SEBI Registered: INP000007164, RIA: INA000020846 | Full regulatory credibility before any conversation about returns |

37-Year Legacy, established in 1987 | Institutional stability across multiple market cycles |

₹805+ Crore AUM across Gujarat and Maharashtra | Proven trust from active HNI clients in your region |

Four strategies: All Weather, Diversified, Business Cycle, ICE Growth | Multiple mandates for different risk profiles and goals |

Offices in Surat, Mumbai, Vadodara | Regional access with national-grade research |

Whether you run a clinic, own a practice, or earn a high specialist income, the portfolio should fit your real financial life. Not a template. Not a product that was built for someone else and repurposed for you.

🚀 You have compared the options. If you are a doctor managing ₹50 lakh or more and want a portfolio built around your actual risk profile, the next step is a 20-minute conversation.

Conclusion

Portfolio management services for doctors in India are most relevant when income is strong but investment attention is limited. Many doctors qualify financially, yet continue with scattered products and low review discipline. The right PMS can bring structure, professional oversight, and clearer capital direction without demanding more of your time.

Match strategy with goals, not trends. Compare providers beyond returns alone, understand fee models clearly, and choose a long-term relationship built on trust, discipline, and consistent communication. A well-managed portfolio should work as hard as you do.

FAQs

01.

What is the minimum investment required for PMS for doctors in India?

The minimum investment for PMS in India is ₹50 lakh as per SEBI rules. Many established doctors and clinic owners qualify based on surplus capital. This threshold places PMS in the high-income investor category.

02.

Is portfolio management services better than mutual funds for doctors?

PMS offers customisation, direct ownership, and active oversight that mutual funds cannot match. Doctors with higher investable surplus may prefer PMS for a more personalised approach. The right choice depends on your financial goals and time availability.

03.

How do portfolio management services work differently for doctors?

PMS suits doctors because medical professionals have limited time to monitor markets regularly. A professional manager handles portfolio reviews, strategy execution, and reporting. Doctors stay focused on practice while investments are managed systematically.

04.

What PMS charges should doctors in India expect to pay?

Charges vary by provider and fee model across fixed fees, performance fees, and exit loads. It is important to review the total fee impact alongside service quality. Post-fee returns against a benchmark matter more than headline fee comparisons.