8 Min Read

8 Min Read

How Can NRI Invest in Indian Stock Market: Complete Guide to PIS Account, Demat Setup and Trading Requirements

How Can NRI Invest in Indian Stock Market: Complete Guide to PIS Account, Demat Setup and Trading Requirements

How Can NRI Invest in Indian Stock Market: Complete Guide to PIS Account, Demat Setup and Trading Requirements

Learn how NRIs can invest in Indian stocks through NRE or NRO accounts, demat setup, PIS routes, tax checks, repatriation planning, and first-trade rules.

Learn how NRIs can invest in Indian stocks through NRE or NRO accounts, demat setup, PIS routes, tax checks, repatriation planning, and first-trade rules.

Learn how NRIs can invest in Indian stocks through NRE or NRO accounts, demat setup, PIS routes, tax checks, repatriation planning, and first-trade rules.

Ckredence Wealth

Ckredence Wealth

|

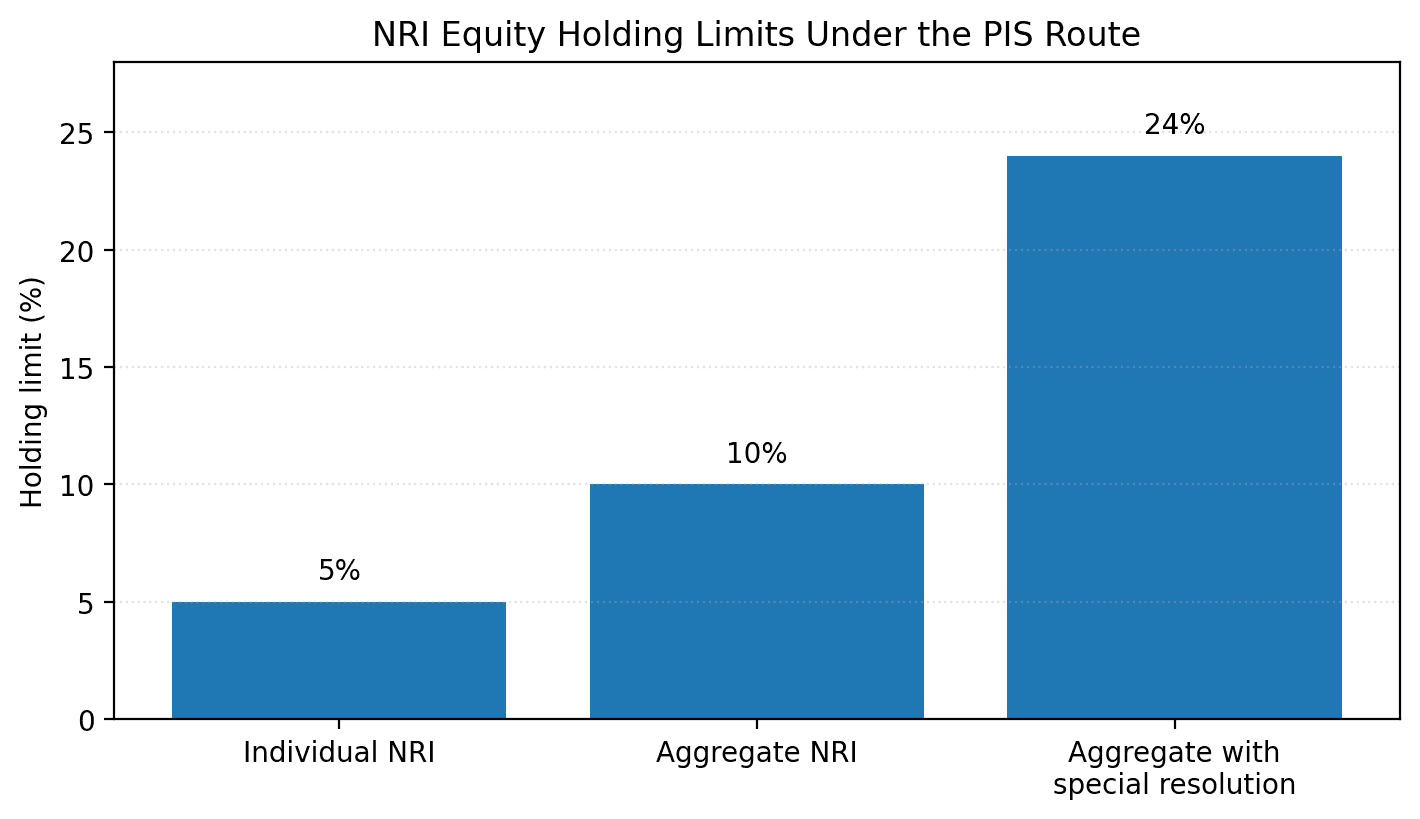

India’s demat-account base reached 19.24 crore accounts by the end of FY25, showing how widely securities investing has expanded. Yet NRIs follow a different account and compliance route from resident investors. RBI rules also place an individual NRI holding limit at 5% of a company’s paid-up capital and an aggregate NRI ownership limit at 10%, subject to a higher ceiling where permitted.

Are you investing in India for a future return home, family needs, diversification, or only because the rupee value looks attractive?

Does your India allocation fit with your existing foreign investments, taxes, and currency exposure?

Have you checked whether NRE, NRO, PIS, demat, and brokerage accounts match the investment you plan to make?

NRIs can invest in Indian listed shares, mutual funds, ETFs, IPOs, bonds, and selected derivatives through permitted routes. The right setup depends on where the money comes from, whether you may repatriate it later, your residence-country tax rules, and the role India should play in your overall portfolio.

Figure: NRI Equity Holding Limits Under the PIS Route. Source: RBI Foreign Investment Guidance.

TL;DR

NRIs can invest in Indian stocks, mutual funds, ETFs, IPOs, bonds, and selected market products.

NRE and NRO accounts serve different fund-source and repatriation needs.

A PIS route is mainly relevant for listed equity investments on a repatriable basis.

Mutual funds, IPOs, ETFs, bonds, and debt instruments may follow non-PIS routes.

Indian equity investing is generally delivery-based for NRIs.

TDS, India tax, residence-country tax, and treaty documents need review before investing.

India exposure should fit a wider global asset-allocation plan.

US, Canada, UK, and other overseas residents may face additional compliance or reporting needs.

Can an NRI Invest in the Indian Stock Market?

Yes. NRIs can invest in Indian securities through permitted banking and brokerage arrangements. The route differs by product, fund source, repatriation preference, and the rules followed by the selected bank or broker.

A resident demat account should not continue unchanged after a person becomes non-resident. The investor must update bank, KYC, demat, and trading details to reflect non-resident status before placing fresh transactions.

What NRIs Can Invest In

NRIs can access several Indian investment products. Each one may require a different account route and has its own tax, liquidity, and reporting position.

Listed equity shares

Mutual funds

Exchange-traded funds

Initial public offerings

Bonds and debt securities

Portfolio Management Services

Selected equity and index derivatives

Direct equity can suit investors who have time to study listed companies. Investors seeking a broader managed route may also compare equity investment services, mutual fund services, and PMS for NRIs before deciding where each part of their money should go.

What NRIs Cannot Treat Like Resident Investors

NRIs cannot simply use a resident brokerage account after changing residential status. They must also follow rules around delivery-based equity trading, investment limits, permitted derivative activity, and movement of sale proceeds.

This does not make Indian investing impossible. It means the account setup needs to be completed correctly before an order is placed.

“A demat account is a precondition for trading in the securities market.” Source: SEBI Investor Education Material on NRI Investments |

Should an NRI Invest in India Before Opening an Account?

The first decision is not whether to open a demat account. It is whether Indian exposure serves a clear goal in your wider financial plan.

Some NRIs invest because they plan to return to India, support family needs, build a rupee-based retirement pool, or keep a part of their wealth linked to India. Others may already have India exposure through property, family business, inherited assets, or existing investments.

Check the Currency of Your Future Goal

A goal in India may need rupee-based investments. A goal abroad may need to be measured in the currency where you expect to spend.

This matters because a rise in rupee value does not automatically mean the same gain in your home currency. The investment should be reviewed in the currency of the future goal.

Avoid Home Bias Without a Portfolio View

Familiarity with Indian companies does not automatically make Indian shares the right choice. India can be a useful part of a portfolio, but it should not become the whole equity plan only because the investor has an Indian background.

A financial advisor in India can help assess whether India belongs as a core allocation, a limited satellite allocation, or a future-goal allocation.

Keep Near-Term Money Separate

Money needed for property payments, relocation, education, emergency use, or business commitments should not be placed in market-linked investments without considering timing. Stock investing needs a longer holding horizon and the ability to accept market movement.

Your account route should follow the role of the money. Your investment product should follow the goal.

NRE, NRO, PIS and Non-PIS: Which Route Does an NRI Need?

NRE and NRO accounts are not interchangeable. They are used for different sources of money and may have different repatriation treatment.

A PIS route is mainly connected with certain listed-equity transactions. Other investments may use non-PIS arrangements through NRE or NRO accounts, depending on the product and the investor’s banking setup.

Account or Route | Main Use | Funding Context | Repatriation Consideration |

|---|---|---|---|

NRE Account | Overseas income held in India | Foreign earnings | Usually used for repatriable investments |

NRO Account | India-sourced income | Rent, pension, dividends, or Indian income | Subject to applicable tax and banking rules |

NRE PIS Route | Listed equity on repatriable basis | NRE or permitted foreign funds | Sale proceeds may be repatriable under applicable rules |

Non-PIS Route | Mutual funds, IPOs, ETFs, bonds, and debt | NRE or NRO route | Depends on product and source account |

The bank and broker should confirm the route before account opening. Do not rely only on an app screen or a generic NRI investment checklist.

Regulatory Note SEBI’s NRI investor material states that PIS permission is not required for IPOs, ESOPs, rights issues, mutual funds, ETFs, bonds, and debt securities. Choose the route after identifying the product, source account, and repatriation requirement. |

Step-by-Step Process for NRI Stock Market Investment

The setup is best handled in order. Starting with a broker before settling the banking route can create avoidable delays.

Step 1: Open or Update Your NRI Bank Account

Start with an NRE or NRO account based on the source of funds and future repatriation requirement. Existing resident savings accounts generally need to be redesignated after residential status changes.

Keep your bank records current. Your passport, overseas address, PAN, tax declarations, and contact details should match across financial accounts.

Step 2: Complete PAN and KYC Requirements

PAN and KYC are required for securities-market investing. Your broker or fund house may also ask for passport copies, overseas-address proof, banking documents, and FATCA or CRS declarations.

The required document list can differ by provider. Ask for the latest checklist before notarising or attesting documents.

Step 3: Open an NRI Demat and Trading Account

A demat account holds securities electronically. A trading account helps you place buy and sell orders.

The account should be opened as a non-resident account and linked to the appropriate NRE, NRO, PIS, or non-PIS banking route. This is where many account-opening errors happen.

Step 4: Select the Product Before Funding the Account

Direct shares, mutual funds, ETFs, IPOs, bonds, and PMS structures do not work the same way. Review the product before moving money into an account only because the bank relationship manager suggested it.

For investors who prefer managed mutual fund exposure, read our guide on mutual funds for NRIs. Investors considering a higher-value listed-equity route can also review Portfolio Management Services.

Step 5: Keep Records From the First Transaction

Save contract notes, capital-gains reports, TDS certificates, bank statements, remittance evidence, and tax documents. These records matter for Indian tax filing, repatriation requests, and tax credit in your country of residence.

Good recordkeeping reduces pressure when you later sell, move countries, or return to India.

What Can an NRI Invest in Through Indian Markets?

NRIs have access to more than direct stocks. The right instrument depends on how closely you want to monitor the investment and whether the money must remain liquid.

Investment Type | What It Can Offer | What Needs Review |

|---|---|---|

Direct Equity | Ownership in selected Indian companies | Delivery rules, company risk, account route |

Mutual Funds | Pooled exposure across asset classes | Fund-house acceptance, FATCA, tax treatment |

ETFs | Listed market exposure through a demat account | Liquidity, tracking difference, product type |

IPOs | Primary-market participation | Eligibility, funding route, post-listing plan |

Bonds | Income-oriented securities exposure | Credit risk, maturity, tax treatment |

PMS | Managed listed-equity portfolios | Suitability, portfolio size, fees, tax reporting |

NRIs from the United States and Canada should check whether the AMC accepts investments from their country. Some fund houses require added declarations or may limit digital onboarding because of FATCA and CRS obligations.

A mutual fund advisor can help compare direct shares, mutual funds, and managed routes without treating every product as a replacement for another.

Trading Rules, Tax and Repatriation Checks for NRIs

NRI investing has product restrictions that residents may not face. Understanding these before a first trade prevents later account blocks or repatriation issues.

The rules are not only about buying shares. They also affect how you sell, receive proceeds, pay tax, and report income abroad.

1. Equity Trading Is Usually Delivery-Based

NRIs generally need to take delivery of Indian equity shares. Intraday equity trading, BTST, and STBT transactions are not permitted under the normal NRI equity route.

This means an NRI should not treat an Indian demat account as a short-term trading account. The account is better used for planned investment decisions.

2. Derivatives Need Separate Verification

Equity and index derivatives may be available to NRIs under specific banking, broker, custody, and non-repatriation conditions. Currency and commodity derivative access is restricted.

Do not assume that a derivative segment visible on a trading platform is automatically available to your NRI account. Confirm it in writing with the bank and broker.

3. Tax Requires an India and Overseas Review

Indian capital gains and dividend income can attract tax and TDS. The final position can depend on the investment product, holding period, treaty benefit, Tax Residency Certificate, and the tax law of your residence country.

For NRIs in countries that tax global income, Indian investment returns may also need reporting abroad. Tax should be checked before investing, not only when it is time to sell.

4. Repatriation Depends on the Account Route

NRE-based investment routes generally offer a different repatriation treatment from NRO-based routes. NRO remittances may need tax documents and bank review before funds can move abroad.

Keep a clear trail from remittance to investment and redemption. This is especially useful when an investor has changed countries or holds several Indian accounts.

A demat account alone does not show whether your India allocation works with your foreign portfolio, tax residence, currency needs, and future plans. Start an NRI portfolio review with Ckredence Wealth before moving money across borders. |

Why Choose Ckredence Wealth for NRI Investment Planning?

NRI investing becomes harder when the investor holds Indian shares, mutual funds, foreign securities, property income, family assets, and more than one bank account. Each item may appear manageable alone, but the combined picture can create gaps in liquidity, tax records, asset allocation, and future repatriation planning.

At Ckredence Wealth, we begin with the role India should play in your total financial picture. We review your goals, existing holdings, investment route, cash needs, and the difference between wealth held in rupees and wealth required in another currency.

Our work can include:

Reviewing whether Indian equity, mutual funds, PMS, or cash holdings serve distinct roles.

Comparing your NRI banking route with your planned investment product.

Reviewing India allocation alongside overseas holdings and future spending needs.

Helping you prepare questions for your bank, broker, and tax professional.

Building a documented investment view rather than reacting to product calls or market headlines.

For investors who want a regulated advisory relationship, read our SEBI Registered Investment Advisor guide. You can also review our financial advisory services in India before deciding the level of support you need.

Before your next remittance becomes an unplanned India allocation, map its role. Bring your Indian holdings, overseas investments, future rupee needs, and available bank routes. We will help you see what should remain separate, what overlaps, and what needs a clearer plan. |

Conclusion

NRIs can invest in Indian markets through permitted bank, demat, trading, and investment routes. But the right way to begin is not by opening every account available. It is by deciding what India needs to do in your wider financial plan, whether that means future rupee spending, family commitments, diversification, or a long-term return plan.

Account setup, tax, TDS, residence-country reporting, and repatriation should be reviewed before the first transaction. A clear structure helps you choose between direct shares, mutual funds, ETFs, PMS, or cash without treating every Indian product as the same type of investment.

FAQs

01.

Can an NRI invest in the Indian stock market without a PIS account?

PIS is commonly used for listed equity investments on a repatriable basis. Mutual funds, ETFs, bonds, debt securities, IPOs, and rights issues may use non-PIS routes.

02.

Can an NRI do intraday trading in Indian shares?

NRIs generally cannot undertake intraday trading in Indian equity shares. Delivery-based investing is normally required through the permitted NRI account route.

03.

Can NRIs from the United States or Canada invest in Indian mutual funds?

Some Indian fund houses accept investments from US and Canada-based NRIs. Others may require added FATCA documentation or restrict digital onboarding.

04.

What should an NRI check before investing in Indian stocks?

Check your bank-account route, demat status, repatriation needs, tax residency, and investment goal. Also review whether India fits your total portfolio rather than only your Indian holdings.

India’s demat-account base reached 19.24 crore accounts by the end of FY25, showing how widely securities investing has expanded. Yet NRIs follow a different account and compliance route from resident investors. RBI rules also place an individual NRI holding limit at 5% of a company’s paid-up capital and an aggregate NRI ownership limit at 10%, subject to a higher ceiling where permitted.

Are you investing in India for a future return home, family needs, diversification, or only because the rupee value looks attractive?

Does your India allocation fit with your existing foreign investments, taxes, and currency exposure?

Have you checked whether NRE, NRO, PIS, demat, and brokerage accounts match the investment you plan to make?

NRIs can invest in Indian listed shares, mutual funds, ETFs, IPOs, bonds, and selected derivatives through permitted routes. The right setup depends on where the money comes from, whether you may repatriate it later, your residence-country tax rules, and the role India should play in your overall portfolio.

Figure: NRI Equity Holding Limits Under the PIS Route. Source: RBI Foreign Investment Guidance.

TL;DR

NRIs can invest in Indian stocks, mutual funds, ETFs, IPOs, bonds, and selected market products.

NRE and NRO accounts serve different fund-source and repatriation needs.

A PIS route is mainly relevant for listed equity investments on a repatriable basis.

Mutual funds, IPOs, ETFs, bonds, and debt instruments may follow non-PIS routes.

Indian equity investing is generally delivery-based for NRIs.

TDS, India tax, residence-country tax, and treaty documents need review before investing.

India exposure should fit a wider global asset-allocation plan.

US, Canada, UK, and other overseas residents may face additional compliance or reporting needs.

Can an NRI Invest in the Indian Stock Market?

Yes. NRIs can invest in Indian securities through permitted banking and brokerage arrangements. The route differs by product, fund source, repatriation preference, and the rules followed by the selected bank or broker.

A resident demat account should not continue unchanged after a person becomes non-resident. The investor must update bank, KYC, demat, and trading details to reflect non-resident status before placing fresh transactions.

What NRIs Can Invest In

NRIs can access several Indian investment products. Each one may require a different account route and has its own tax, liquidity, and reporting position.

Listed equity shares

Mutual funds

Exchange-traded funds

Initial public offerings

Bonds and debt securities

Portfolio Management Services

Selected equity and index derivatives

Direct equity can suit investors who have time to study listed companies. Investors seeking a broader managed route may also compare equity investment services, mutual fund services, and PMS for NRIs before deciding where each part of their money should go.

What NRIs Cannot Treat Like Resident Investors

NRIs cannot simply use a resident brokerage account after changing residential status. They must also follow rules around delivery-based equity trading, investment limits, permitted derivative activity, and movement of sale proceeds.

This does not make Indian investing impossible. It means the account setup needs to be completed correctly before an order is placed.

“A demat account is a precondition for trading in the securities market.” Source: SEBI Investor Education Material on NRI Investments |

Should an NRI Invest in India Before Opening an Account?

The first decision is not whether to open a demat account. It is whether Indian exposure serves a clear goal in your wider financial plan.

Some NRIs invest because they plan to return to India, support family needs, build a rupee-based retirement pool, or keep a part of their wealth linked to India. Others may already have India exposure through property, family business, inherited assets, or existing investments.

Check the Currency of Your Future Goal

A goal in India may need rupee-based investments. A goal abroad may need to be measured in the currency where you expect to spend.

This matters because a rise in rupee value does not automatically mean the same gain in your home currency. The investment should be reviewed in the currency of the future goal.

Avoid Home Bias Without a Portfolio View

Familiarity with Indian companies does not automatically make Indian shares the right choice. India can be a useful part of a portfolio, but it should not become the whole equity plan only because the investor has an Indian background.

A financial advisor in India can help assess whether India belongs as a core allocation, a limited satellite allocation, or a future-goal allocation.

Keep Near-Term Money Separate

Money needed for property payments, relocation, education, emergency use, or business commitments should not be placed in market-linked investments without considering timing. Stock investing needs a longer holding horizon and the ability to accept market movement.

Your account route should follow the role of the money. Your investment product should follow the goal.

NRE, NRO, PIS and Non-PIS: Which Route Does an NRI Need?

NRE and NRO accounts are not interchangeable. They are used for different sources of money and may have different repatriation treatment.

A PIS route is mainly connected with certain listed-equity transactions. Other investments may use non-PIS arrangements through NRE or NRO accounts, depending on the product and the investor’s banking setup.

Account or Route | Main Use | Funding Context | Repatriation Consideration |

|---|---|---|---|

NRE Account | Overseas income held in India | Foreign earnings | Usually used for repatriable investments |

NRO Account | India-sourced income | Rent, pension, dividends, or Indian income | Subject to applicable tax and banking rules |

NRE PIS Route | Listed equity on repatriable basis | NRE or permitted foreign funds | Sale proceeds may be repatriable under applicable rules |

Non-PIS Route | Mutual funds, IPOs, ETFs, bonds, and debt | NRE or NRO route | Depends on product and source account |

The bank and broker should confirm the route before account opening. Do not rely only on an app screen or a generic NRI investment checklist.

Regulatory Note SEBI’s NRI investor material states that PIS permission is not required for IPOs, ESOPs, rights issues, mutual funds, ETFs, bonds, and debt securities. Choose the route after identifying the product, source account, and repatriation requirement. |

Step-by-Step Process for NRI Stock Market Investment

The setup is best handled in order. Starting with a broker before settling the banking route can create avoidable delays.

Step 1: Open or Update Your NRI Bank Account

Start with an NRE or NRO account based on the source of funds and future repatriation requirement. Existing resident savings accounts generally need to be redesignated after residential status changes.

Keep your bank records current. Your passport, overseas address, PAN, tax declarations, and contact details should match across financial accounts.

Step 2: Complete PAN and KYC Requirements

PAN and KYC are required for securities-market investing. Your broker or fund house may also ask for passport copies, overseas-address proof, banking documents, and FATCA or CRS declarations.

The required document list can differ by provider. Ask for the latest checklist before notarising or attesting documents.

Step 3: Open an NRI Demat and Trading Account

A demat account holds securities electronically. A trading account helps you place buy and sell orders.

The account should be opened as a non-resident account and linked to the appropriate NRE, NRO, PIS, or non-PIS banking route. This is where many account-opening errors happen.

Step 4: Select the Product Before Funding the Account

Direct shares, mutual funds, ETFs, IPOs, bonds, and PMS structures do not work the same way. Review the product before moving money into an account only because the bank relationship manager suggested it.

For investors who prefer managed mutual fund exposure, read our guide on mutual funds for NRIs. Investors considering a higher-value listed-equity route can also review Portfolio Management Services.

Step 5: Keep Records From the First Transaction

Save contract notes, capital-gains reports, TDS certificates, bank statements, remittance evidence, and tax documents. These records matter for Indian tax filing, repatriation requests, and tax credit in your country of residence.

Good recordkeeping reduces pressure when you later sell, move countries, or return to India.

What Can an NRI Invest in Through Indian Markets?

NRIs have access to more than direct stocks. The right instrument depends on how closely you want to monitor the investment and whether the money must remain liquid.

Investment Type | What It Can Offer | What Needs Review |

|---|---|---|

Direct Equity | Ownership in selected Indian companies | Delivery rules, company risk, account route |

Mutual Funds | Pooled exposure across asset classes | Fund-house acceptance, FATCA, tax treatment |

ETFs | Listed market exposure through a demat account | Liquidity, tracking difference, product type |

IPOs | Primary-market participation | Eligibility, funding route, post-listing plan |

Bonds | Income-oriented securities exposure | Credit risk, maturity, tax treatment |

PMS | Managed listed-equity portfolios | Suitability, portfolio size, fees, tax reporting |

NRIs from the United States and Canada should check whether the AMC accepts investments from their country. Some fund houses require added declarations or may limit digital onboarding because of FATCA and CRS obligations.

A mutual fund advisor can help compare direct shares, mutual funds, and managed routes without treating every product as a replacement for another.

Trading Rules, Tax and Repatriation Checks for NRIs

NRI investing has product restrictions that residents may not face. Understanding these before a first trade prevents later account blocks or repatriation issues.

The rules are not only about buying shares. They also affect how you sell, receive proceeds, pay tax, and report income abroad.

1. Equity Trading Is Usually Delivery-Based

NRIs generally need to take delivery of Indian equity shares. Intraday equity trading, BTST, and STBT transactions are not permitted under the normal NRI equity route.

This means an NRI should not treat an Indian demat account as a short-term trading account. The account is better used for planned investment decisions.

2. Derivatives Need Separate Verification

Equity and index derivatives may be available to NRIs under specific banking, broker, custody, and non-repatriation conditions. Currency and commodity derivative access is restricted.

Do not assume that a derivative segment visible on a trading platform is automatically available to your NRI account. Confirm it in writing with the bank and broker.

3. Tax Requires an India and Overseas Review

Indian capital gains and dividend income can attract tax and TDS. The final position can depend on the investment product, holding period, treaty benefit, Tax Residency Certificate, and the tax law of your residence country.

For NRIs in countries that tax global income, Indian investment returns may also need reporting abroad. Tax should be checked before investing, not only when it is time to sell.

4. Repatriation Depends on the Account Route

NRE-based investment routes generally offer a different repatriation treatment from NRO-based routes. NRO remittances may need tax documents and bank review before funds can move abroad.

Keep a clear trail from remittance to investment and redemption. This is especially useful when an investor has changed countries or holds several Indian accounts.

A demat account alone does not show whether your India allocation works with your foreign portfolio, tax residence, currency needs, and future plans. Start an NRI portfolio review with Ckredence Wealth before moving money across borders. |

Why Choose Ckredence Wealth for NRI Investment Planning?

NRI investing becomes harder when the investor holds Indian shares, mutual funds, foreign securities, property income, family assets, and more than one bank account. Each item may appear manageable alone, but the combined picture can create gaps in liquidity, tax records, asset allocation, and future repatriation planning.

At Ckredence Wealth, we begin with the role India should play in your total financial picture. We review your goals, existing holdings, investment route, cash needs, and the difference between wealth held in rupees and wealth required in another currency.

Our work can include:

Reviewing whether Indian equity, mutual funds, PMS, or cash holdings serve distinct roles.

Comparing your NRI banking route with your planned investment product.

Reviewing India allocation alongside overseas holdings and future spending needs.

Helping you prepare questions for your bank, broker, and tax professional.

Building a documented investment view rather than reacting to product calls or market headlines.

For investors who want a regulated advisory relationship, read our SEBI Registered Investment Advisor guide. You can also review our financial advisory services in India before deciding the level of support you need.

Before your next remittance becomes an unplanned India allocation, map its role. Bring your Indian holdings, overseas investments, future rupee needs, and available bank routes. We will help you see what should remain separate, what overlaps, and what needs a clearer plan. |

Conclusion

NRIs can invest in Indian markets through permitted bank, demat, trading, and investment routes. But the right way to begin is not by opening every account available. It is by deciding what India needs to do in your wider financial plan, whether that means future rupee spending, family commitments, diversification, or a long-term return plan.

Account setup, tax, TDS, residence-country reporting, and repatriation should be reviewed before the first transaction. A clear structure helps you choose between direct shares, mutual funds, ETFs, PMS, or cash without treating every Indian product as the same type of investment.

FAQs

01.

Can an NRI invest in the Indian stock market without a PIS account?

PIS is commonly used for listed equity investments on a repatriable basis. Mutual funds, ETFs, bonds, debt securities, IPOs, and rights issues may use non-PIS routes.

02.

Can an NRI do intraday trading in Indian shares?

NRIs generally cannot undertake intraday trading in Indian equity shares. Delivery-based investing is normally required through the permitted NRI account route.

03.

Can NRIs from the United States or Canada invest in Indian mutual funds?

Some Indian fund houses accept investments from US and Canada-based NRIs. Others may require added FATCA documentation or restrict digital onboarding.

04.

What should an NRI check before investing in Indian stocks?

Check your bank-account route, demat status, repatriation needs, tax residency, and investment goal. Also review whether India fits your total portfolio rather than only your Indian holdings.